Markets got off to a rough start in the pre-market trading hours on Tuesday and after a down day Monday. But then headlines surfaced that pointed to delaying the December 15th tariffs. U.S. and Chinese trade negotiators were said to be laying the groundwork for a delay of tariffs set to kick in on Dec. 15, according to officials on both sides, as they continue to haggle over how to get Beijing to commit to massive purchases of U.S. farm products President Trump is insisting on for a near-term deal.

Once the headlines surfaced, equity futures sharply reversed from down over 100 points on the Dow futures to up 20 points within minutes. If the anticipation amongst Wall Street traders isn’t enough, the mixed messages from White House officials serve to keep investors on edge. Shortly after the positive news on trade was disseminated by the Wall Street Journal, here’s what Larry Kudlow had to say at a Wall Street Journal conference.

“The reality is those tariffs are still on the table, the Dec. 15 tariffs, and the president has indicated if the short strokes remaining in negotiations do not pan out to his liking that those tariffs could go back into place.

So, they could not, but they also could. There is no definitive decision on that yet.”

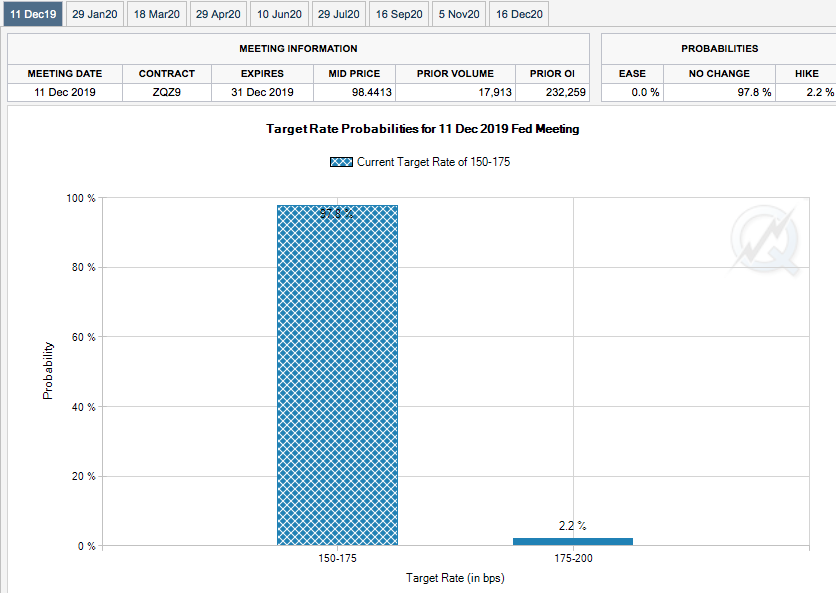

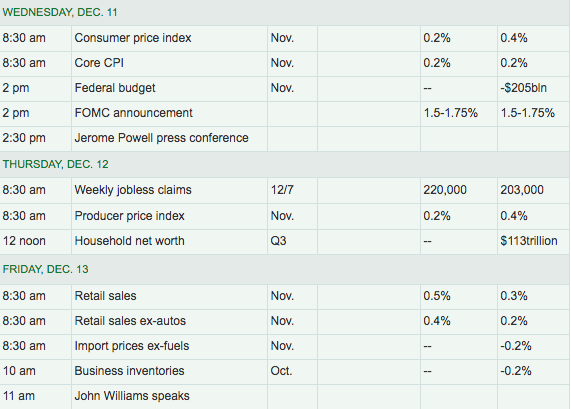

The reality of the situation is that come December 15th, investors will know for sure where the trade war stands and whether or not tariffs will be moved into position once again. And all of this ahead of the FOMC rate announcement and press conference with Jerome Powell. The Fed Chairman has show stark improvement when messaging to the public over the last 3 press conferences. Wall Street doesn’t expect any change in rates at this meeting according to the CME FedWatch Tool, which should also make Powell’s task that much easier during the press conference.

With the economy apparently on firmer footing, the Fed has taken a pause, following through with their October decision to hold rates steady absent a material change in the outlook. Investors shouldn’t be expecting any material deviation from this path or the outlook on the economy, which one could argue has strengthened. Recent improvements to Nonfarm payroll monthly reports, Consumer Sentiment, Markit PMIs and the housing sector data allow the Fed to pause and await the impact of the already enacted 3 rate cuts this year.

Policy makers aren’t inclined to cut rates again barring a fresh downturn in activity. Central bankers remain wary of potential downside risk given the ongoing trade war and potential for the U.S. to commence a more broad trade war with Europe near-term. Along these lines of consideration, coupled with the fact they also have yet to achieve sustained inflation at their 2% target rate, it’s unlikely that rate hikes will take place for the foreseeable future. Powell will likely emphasize this point in the post-meeting press conference. Markets will likely approve of such messaging.

With all that being said, there are strategists who believe the Fed could actually deliver a shock to markets on Wednesday by forecasting a rate hike out in 2020.

“They see an outside chance that the Federal Open Market Committee’s updated dot plot will signal a 2020 rate increase, an outcome that would flatten the U.S. yield curve and boost the dollar, according to a report from BofA’s Mark Cabana, Michelle Meyer, Ben Randol and Joe Song. To be sure, that’s not what they view as most probable; they think the dot plot will show the Fed on hold next year.“

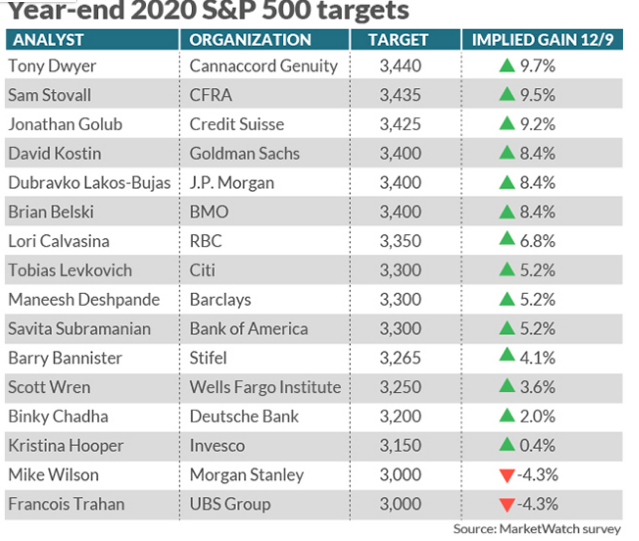

At this point in the calendar year, analysts are denoting their respective 2020 price targets and market outlooks.

We can add Jefferies to the list above with their recently announced price target on the S&P 500 for 2020.

“Just over twelve months ago, the equity markets were selling off as the U.S. fixed income markets choked on expectations of further rate hikes,” equity strategist Sean Darby said. But in the year since, the Fed cut rates three times and returned to making large-scale asset purchases, which in part helped to drive a more than 20% gain in the S&P 500 in 2019.

“If 2018 was a year of policy over-tightening then 2019 was a year of unwinding policy mistakes. Hence, 2020 looks to be the year of normalization as a number of macro factors recede.

2020 ought to see some normalization as earnings growth moves back in tandem with GDP. In summary, equity investors are likely to be focused on the traditional drivers for U.S. markets namely earnings growth.

“S&P 500 valuations don’t necessarily start off as inexpensive as other bourses but the cyclicals offer a lot of earnings upside if the global economy begins to resynchronize. Moreover, 2019 saw unprecedented risk aversion and there is plenty of room for assets to move away from fixed income into equities given the potential inflation risks.

In turn, this leads us to the biggest risk for 2020 which is a switch from low volatility, bond proxies into the real economy, cyclical growth stocks.

We expect earnings to accelerate back to trend of circa 10%, real interest rates to remain negative alongside a steep yield curve,” Darby said. “This ought to mean that the S&P 500 can advance to 3,300. We upgrade the S&P 500 to Modestly Bullish.”

While many analysts and strategists seem to be heralding a rebound in global growth, an easing of trade tensions and a continuation of central bank support, Morgan Stanley continues to encourage caution.

What we’ve seen from Morgan Stanley’s Lisa Shalett Chief Investment Officer, Wealth Management division throughout 2019 is a very cautious view, almost bearish some might say. In her latest cautionary tale on the market and economic outlook, here is what she had to say:

- U.S. economic growth may not rebound as expected. While global growth is improving, we’ve seen continued and unanticipated weakness in U.S. data, particularly in manufacturing. For example, the new orders index within the Manufacturing Institute for Supply Management Report on Business fell to 47.2, the lowest level since June 2012. Services data was also weak. Construction spending fell in October when a 0.4% gain was expected.

- Labor market data is showing cracks. Non-farm payrolls have remained strong, but softer, survey-based data, which tends to be more forward looking, has started to roll over. The “jobs plentiful” measure within the Consumer Confidence series is past peak, as is the Job Openings and Labor Turnover Survey (JOLTS) data. Most tellingly, the smallest businesses (those with fewer than 20 employees), are now shedding jobs. That suggests weakness in the “gig” economy that isn’t yet visible in the unemployment claims data.

- Improvement in trade policies may not lead to more corporate spending. Many investors expect a potential trade truce to lead to upside in capital spending. That may not be a good call either. Morgan Stanley’s indicator of capital spending intentions has remained stuck, despite some signs that trade tensions are improving. The Atlanta and Philadelphia regional Federal Reserve Bank surveys show spending stuck at levels last seen in 2011 and 2015. Most troubling: research and development budgets aren’t growing. That’s a bad sign for tech spending, especially for the maturing cloud-related “software and services” sector, which represents more than a third of all private non-residential spending.

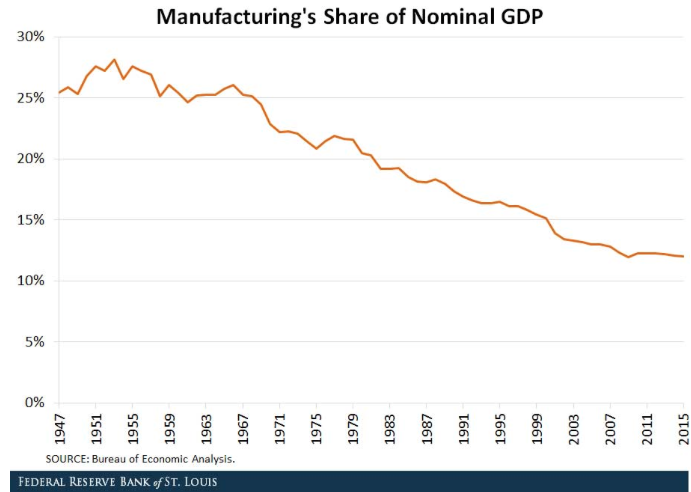

To Lisa Shalett’s first point on economic weakness, we can certainly agree that manufacturing has been weak. It’s no secret that manufacturing has been under great pressure from the protracted trade war, but it’s also no secret that manufacturing makes up barely 12% of GDP.

And to belabor the point on manufacturing as a percentage of GDP, as the chart shows, it is less and less relevant with each passing year. Trade war or not, the U.S. is not increasing manufacturing output for any elongated period of time. We’re an importer of goods! As it pertains to the October construction spending data, again, Shalett is correct. But in this regard, she’s actually outlining the MoM data and not the YoY data.

Construction spending during October 2019 was estimated at a seasonally adjusted annual rate of $1,291.1billion, 0.8% below the revised September estimate of $1,301.8 billion. The October figure is 1.1%, above the October 2018 estimate of $1,277.4 billion. Not as bad as she’s figuring into her outlook in this regard. But in earnest, construction spending has been down on a YoY basis through the first 10 months of the year. As such, she deserves this point in her favor. But, there’s always a but now isn’t there.

Homebuilders are building fewer single family homes in favor of less costly multi-family homes, which has served to distort some of the data and tracking efforts. After all, New home sales are at a cyclical high, Pending home sales and Existing home sales have surged since the Spring.

The housing market has been a stark out-performer in 2019, when it comes to industry data. And as it pertains to Shalett’s concerns over weakening employment data, should it not prove to weaken this late in the economic cycle? Additionally, are wages still rising in a tighter labor market? We don’t see these questions being considered in her noted concerns.

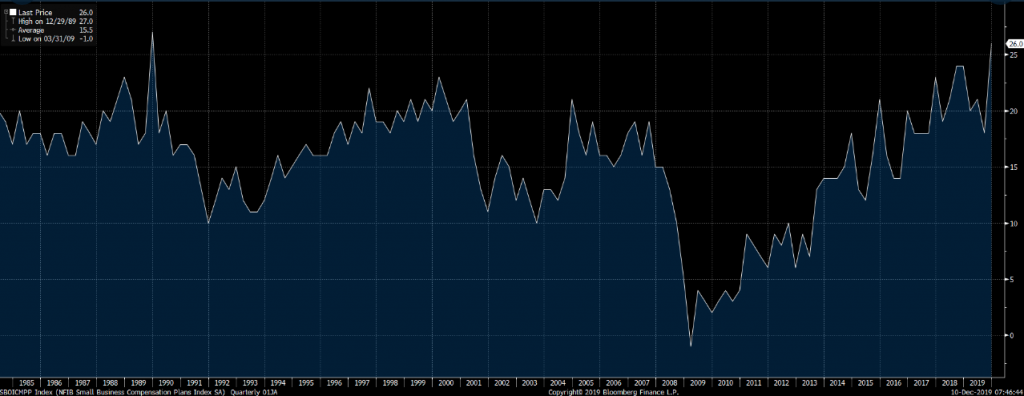

Moreover, in speaking about small business operators, the latest NFIB survey’s aim to shed some light on the subject matter of employment and wages. As reported last week in NFIB’s monthly jobs report, a net 30% of small business owners, seasonally adjusted, reported raising compensation (unchanged) and 26% plan to do so in the coming months, up 4 points and the highest level since December 1989. Job creation jumped in November, with an average addition of 0.29 workers per firm, the highest level since May. Finding qualified workers though remains the top issue for 26% reporting this as their number one problem, 1 point below August’s record high.

“Despite a tight labor market, small business owners are doing exactly what they said they would do thanks to tax relief. They’re creating new jobs and raising compensation at record levels,” said NFIB President & CEO Juanita D. Duggan. “The only thing holding them back continues to be finding qualified workers, but in spite of that challenge the small business economy is roaring.”

NFIB net compensation plans index is quite literally at cycle highs! (See chart below)

Do we really need to dissect Shalett’s comments on trade? I think our point has been made. But for fear of a bullish bias injection, let’s hear it from an outside party. Here is what the President of Goldman Sachs said about the outlook for the economy:

“We’re pretty constructive on the overall economy. Certainly, in the United States in particular, the economy feels if anything like it might be accelerating again from what had been a little bit more of a patchy 2019,” said Goldman Chief Operating Officer John Waldron.

“I do think the Fed’s easing bias has made a big impact. So we’re seeing that implication of easier policy coming through in the economy and it’s become much more of a stimulant for particularly consumers, but corporations as well.”

The Goldman exec noted that much of the resilience in the U.S. markets and economy could be attributed to American consumption, which accounts for about 70% of GDP growth and has for the last several quarters offset weaker business spending.

With back-to-back down days in the market, investors are still troubled by mixed messaging regarding the December 15 tariffs. On again-off again tariffs took U.S. indices for a ride on Tuesday, even as the VIX came under pressure. Nonetheless, all eyes and ears will be on the Fed today.

The economic calendar identifies the main piece of economic data for the week won’t be delivered until Friday. Investors will want to see a validation of the strong Black Friday weekend retail sales when the November monthly retail sales are released on Friday. The forecast has been lowered during the course of the week already, from .5% MoM growth to .4% MoM growth as shown in the MarketWatch table above.

At Finom Group and with regards to the monthly retail sales, we’ll be paying close attention to the category sales, mainly the growth between Nonstore and Department store retail sales. The Department store retail sales have been declining for the better part of the last 6-7 years, as Nonstore (online) sales have seen accelerated growth rates. The likes of Macy’s (M), Kohl’s (KSS) J.C. Penney (JCP) and Nordstrom’s (JWM) have all found sales faltering over the last several years as consumption trends have shifted more in favor of online sales. CNBC’s Jim Cramer takes up this very subject and with comments taking aim on these retailers specifically:

Consumers are finding it easier to shop for better prices from their cellphones, and retailers such as Macy’s and Kohl’s are finding it harder to staff their stores, especially during this holiday shopping season, the “Mad Money” host said.

“Now these troubled retailers can’t afford to offer the same level of customer service they used to. Sometimes they have long lines, sloppy aisles, empty registers. These are all common complaints about most of the mall-based department stores that I read online. They can’t afford to be run efficiently.

The department chains failed to bolster their digital platforms enough or install the right strategies to lure customers inside their stores and improved delivery services are making it easier for consumers to try on clothes in the privacy of their own homes — rather than using in-store dressing rooms — and return items that they don’t want.

The problem for Macy’s and Kohl’s and Nordstrom is that all of these trends are accelerating, meaning their position gets worse and worse with every passing year.”