U.S. equity markets are in distribution and/or de-risk mode ahead of the December 15th tariff deadline. While the financial news media outlets march out various opinions and forward-looking analysis for the markets and economy given this critical trade issue, investors have taken to de-risking their respective portfolios… just in case.

On Monday, investors began adding protection and selling equities ahead of the tariff deadline decision and with varied commentary on the issue from the White House Administration. The VIX rose more than 2 points (16%+) on Monday, as investors found cheaper protection in S&P 500 put options and perceived risk to the market at higher levels. The major averages found a more even distribution of selling with all 3 major averages down roughly 3%+ on the trading session with the tech-heavy Nasdaq (NDX) leading the way lower, losing .4% on the trading session. The setup for Tuesday’s trading session hasn’t improved either, as U.S. equity futures are showing additional selling pressure looms ahead of the opening bell on Wall Street.

On Monday, when asked, Agriculture Secretary Sonny Perdue offered the following at a conference and with regards tot he Dec. 15 tariffs:

“We have a deadline coming up on the Dec. 15 for another tranche of tariffs, I do not believe those will be implemented and I think we may see some backing away,” Purdue said at a conference in Indianapolis, Indiana Monday.“

In a procedural step that may also signal a broader trade agreement with the U.S. is drawing closer, China’s Finance Ministry said Friday it’s in the process of waiving retaliatory tariffs on imports of U.S. pork and soy by domestic companies. Also, Chinese private crushers are back in the market for U.S. soybeans, with the nation granting waivers on at least 1 million tons of the oilseeds to private buyers, according to people who asked not to be identified because the information is private. State-owned companies are excluded from the process, they said. The waivers allow purchasers to bring in the beans without incurring the retaliatory duties.

“I don’t think the president wants to implement these new tariffs but there’s got to be some movement on their part to encourage him not to do that and hopefully the signal that they sent over soy and pork reduction might be that signal in that way.”

Of course, while Perdue is offering his opinion we’ve heard others like CNBC’s Jim Cramer suggest the President will and should impose the last tranche of tariffs. Cramer went so far as to double-down on this opinion on Monday during the Mad Money show which he hosts.

“There is “no reason” for Trump to step away from his threat to put more pressure on the Chinese government in the ongoing trade war.

I say fine, the trade war’s hurting China a lot more than it’s hurting us. Don’t believe the conventional media, they’re wrong — they haven’t done the work. Negative trade war news will cause stocks to sell off.”

Cramer’s main reason for suggesting the President should move forward with the December tariffs centers on the surprising strength of the U.S. economy after a protracted 18-month trade feud that hasn’t proven to downshift consumer spending or the labor market all that much. The problem with this thinking or analysis is that most of the implemented tariffs to-date have been absorbed by businesses or have yet to hit consumer goods in any material way. The December 15th tariffs are just those tariffs that would hit consumer goods, during the most critical spending period of the year.

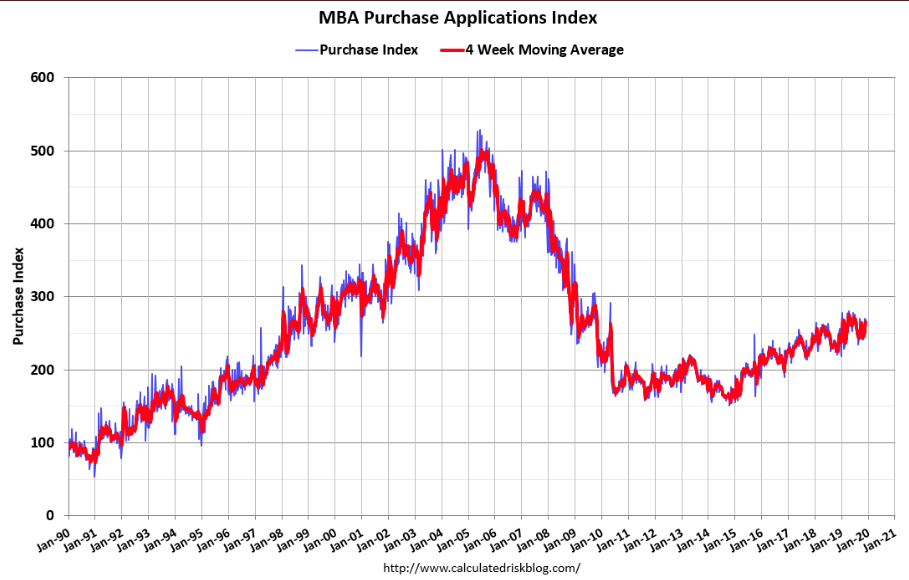

If we are to assume the tariffs will be implemented come Sunday, reluctantly or freely matters not at this point, there may be an offset in the way lower rates. At this point in the trade war and on a YoY basis, rates are lower than where they were this time a year ago and even since the first round of tariffs had been imposed in July 2018. Lower rates have contributed to a refinance boom, that has shown up in the mortgage and housing markets as both have been trending higher all year long.

Through refinancing, households have been able to reduce their monthly mortgage payments and/or cash out equity in their homes. This has aided in supporting all aspects of the household balance sheet and consumer spending over the last 18-month period and through the duration of the trade feud. It’s with this in mind that Canaccord Genuity’s Tony Dwyer takes exception to the doomsayer sentiment over the ongoing trade war and even the potential December 15th tariffs. In his latest market commentary and outlook for 2020, Dwyer offers his analysis on tariffs as it pertains to the economic and market implications.

“Company’s have extended maturities through debt refinancing, which has continued to support economic growth and a strong labor market, as the Fed is on hold.

The trend of the market multiple is higher. When you’re in a sub 3% core inflation environment, the average market multiple is 19X. If you go back to 2016, we had the same global inflection point in manufacturing with a 22X multiple.

The Powell put makes the Greenspan put look like nothing. Powell basically said he’s not raising rates for the foreseeable future.”

Tony Dwyer goes on to say that in this environment investors want to continue to be in offense-mode. They should be buying Information Technology, Financials and Industrials. He goes on to suggest investors should be chasing the next “tick” in the market, but on pull backs investors should be looking to buy these sectors according to like cycles in history.

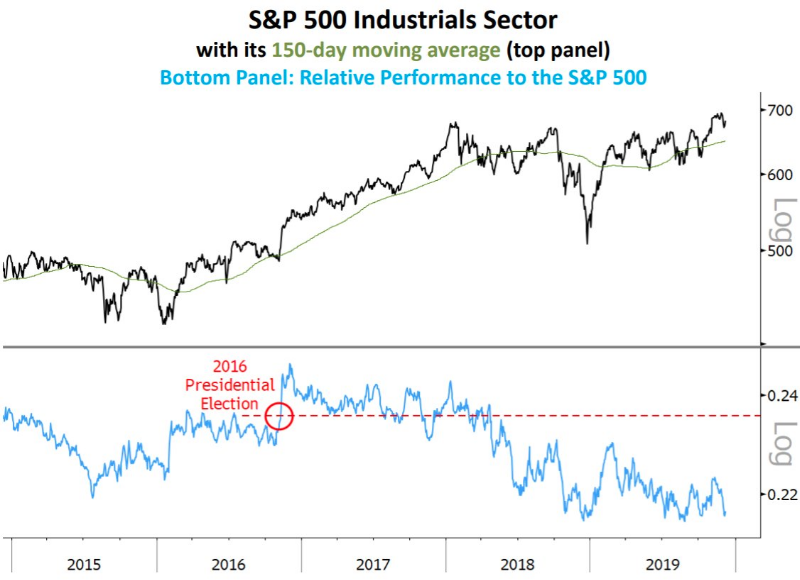

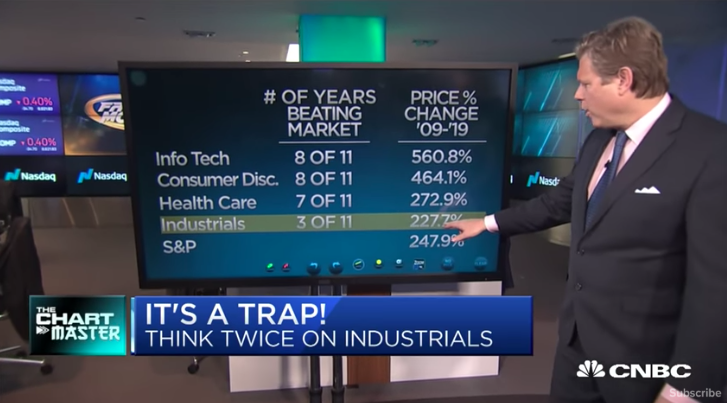

Now, while Tony Dwyer is touting an posture of offensive should the market weaken further near-term and even post a December 15th tariff imposition, Carter Worth suggests to “stay away” from Industrials. Carter Worth reiterates this view to stay underweight Industrials as the sectors relative performance flirts with new 52-week lows.

Carter Worth goes on to offer the relative performance with the S&P 500 during the last 11 years. He points out that the Industrials index (DJI) has only outperformed the S&P 500 3 of the last 11 years. After the 2016 election, Industrials received a reasonable bump higher with the broader market. Unfortunately, under the premise and duration of the trade war, the rise in the Industrials have given way to lower highs and relative underperformance with respect to the S&P 500.

So while Tony Dwyer touts the Industrial’s historic performance from past mini-recessions in manufacturing, as there was in 2016, it didn’t exist within the confines of a trade war. The trade war has taken aim at certain of the Industrial stocks. The Industrials have taken a big hit from the already implemented tariffs and/or trade war, which doesn’t seem to be unwinding any time soon.

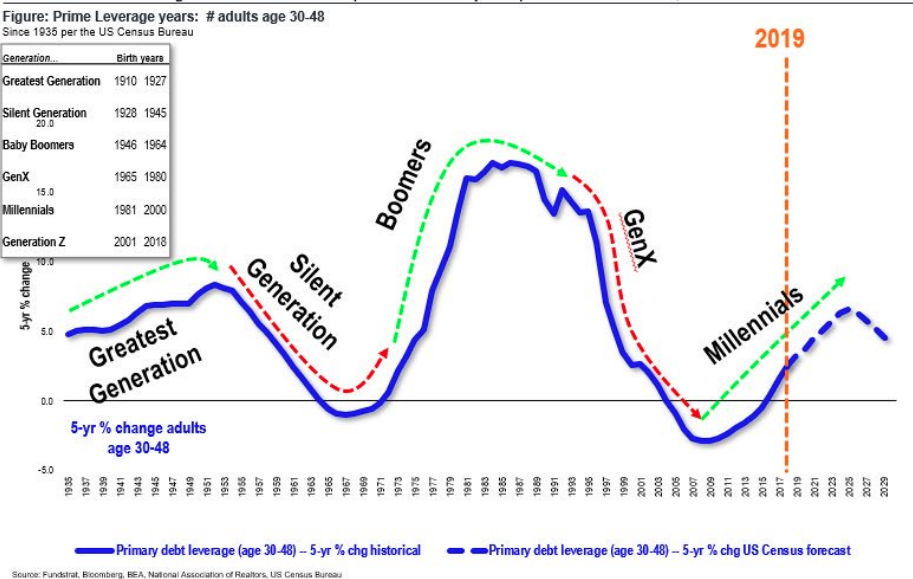

It remains to be seen what happens on December 15th, but either way the market’s reaction will be outsized in my opinion. As it pertains to the U.S.’ resilience from economic growth during the trade war compared to China, FundStrat’s Tom Lee says we should thank the Millenials.

FUNDSTRAT: “The U.S. is “avoiding the sluggishness seen in Asia and Europe, stupefying many economists … [W]e can thank Millennials, who are now entering their prime income years. .. This tailwind should continue for a few years.”

Speaking of those Millennials, at lest, we’ll see just how their spending habits have contributed to retail sales during the early days of the holiday period come Friday. November’s retail sales is the key economic data release of the week. Preliminary sales results from the Black Friday weekend have been strong, while headlines on certain credit card data have suggested weakness.

- J.P. Morgan Merchant Services’ combined in-store and e-commerce payment authorization volume for Black Friday increased 22.3% over 2018 Black Friday volume. On Cyber Monday, J.P. Morgan processed 26.5% more e-commerce payment authorizations than on Cyber Monday in 2018.

- According to Adobe, shoppers in the U.S. spent a total of $7.4 billion online on Black Friday, a 19.6% increase over 2018. On Cyber Monday, Adobe estimated online sales reached $9.4 billion, up 18.9% from the prior year.

- The strength in retail sales carried over into December as Cyber Monday commenced and found record breaking results. Cyber Monday saw a record $9.4 billion spent by online shoppers.

- Amazon (AMZN) said Cyber Monday was its ”’single biggest shopping day in company history”.

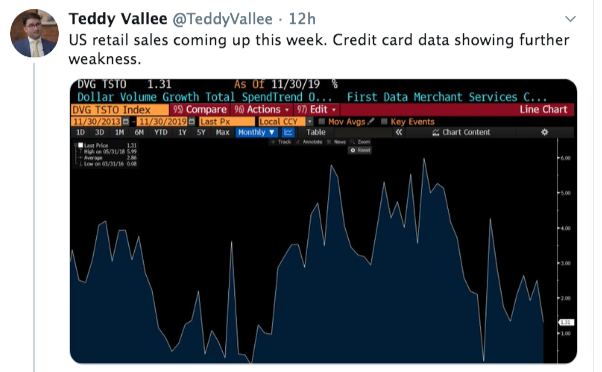

While the headline notes from Black Friday weekend sales were strong YoY, First Data Merchant Services Credit Card data shows weakness, according to Teddy Vallee. The Founder & CIO of Pervalle Global often tweets this data publicly, for which the data is often found dramatically at odds with the actual results on monthly retail sales disseminated by the Census Bureau.

And it’s not just First Data Merchant Services credit card sales tracking that proves at odds with monthly retail sales, but keep in mind that the headline data is offered on a MoM basis. One has to dig into the Census Bureaus data release to extrapolate the YoY results. That’s what we look at mainly and in order to capture the long-term trajectory of retail sales. Any given month can prove a hiccup from the previous month. The best analysis is to review the YoY data, especially as seasonality proves relevant and impactful MoM.

Whether or not Teddy Valle’s primary retail sales tracking will fall inline with Friday’s, November retail sales report remains to be seen. We’ve seen it prove faulty many a time before. And this credit card sales tracking is not the only tracking data that has proven faulty. Bank of America Merrill Lynch’s data has also failed to deliver on ominous headlines in the past. Recall that back in September, BofAML was calling for a significant MoM drop in the August retail sales report. Finom Group took the liberty of reporting on the bank’s warning that proliferated in the financial media just ahead of the Census Bureau’s release of the data and in an article titled Trade Concessions, Central Banks & Retail Sales Ahead. See the reported notes below:

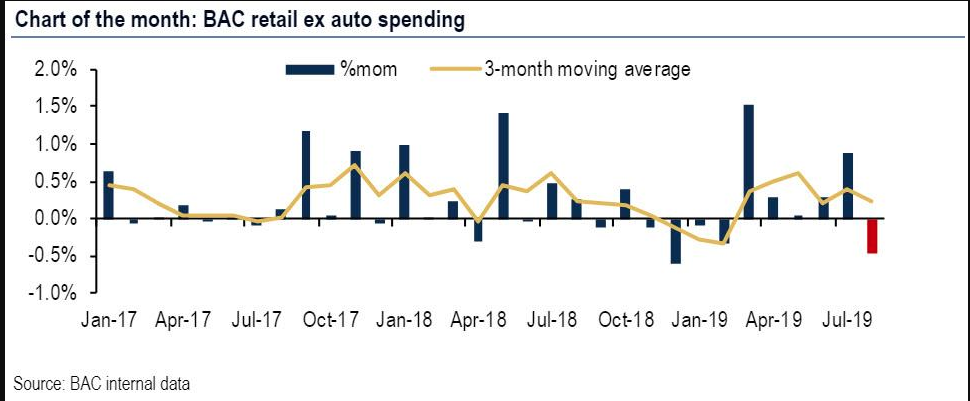

“Bank of America credit and debit card data, which shows that after a strong month of spending in July, consumers aggressively tightened the strings of their wallets in August.

Specifically, BAC found that retail sales ex-autos fell 0.5% month-over-month, which reversed the 0.9% gain in July, and was not only the first monthly contraction since February this year, but was also the biggest monthly drop in 2019.

- Based on the aggregated BAC credit and debit card data, retail sales ex-autos fell 0.5% month-over-month (mom) seasonally adjusted (sa). This reversed the 0.9% mom gain in July. As always, there were a number of “special factors” which we decipher in this note.

- Amazon Prime Day and other retailers’ summer promotions in mid-July provided a significant boost to spending, as we showed last month. In our view, these promotions effectively pulled forward demand into July and out of August.

- Outside of the promotion distortions, we also think spending was dampened by weakening sentiment.

- According to BofA, Amazon Prime Day and other retailers’ summer promotions in mid-July provided a significant boost to spending, in effect pulling forward consumer demand from the future, into July and out of August. Focusing specifically on discretionary spending categories likely impacted by the promotions, the bank’s economists found that it increased 1.7% mom in July but tumbled 1.4% in August.

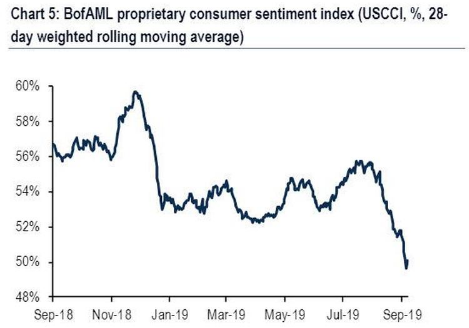

- Also, BofA’s own proprietary “Word from Main Street” index showed that the BofAML US consumer confidence indicator (USCCI) dropped in recent weeks, tumbling to the lowest level in years. It briefly dipped below the 50% breakeven level before rebounding, signifying that respondents, on balance, are more pessimistic. BofA suspects that the drop in sentiment left consumers a bit more hesitant to spend this month.

This wouldn’t be the first time BofAML credit card and sentiment data has painted a negative light on their retail sales forecast. The firm called for a decline in April retail sales, which on first reporting was accurate, but with monthly revisions was not. April retail sales were revised from a negative .2% print to positive in the following monthly data release. The BofAML data is skewed due to credit card profile tracking. Nonetheless, the size of the reversal forecasted is notable and also identified in current economists’ expectations. Most economists only expect a modest .1% growth in August retail sales, largely due to the Amazon Prime affect and lower MoM gasoline prices. If the major issue in the report is in fact gasoline price related, investors are likely to look beyond a weak report. Additionally, a weak report may also be found favorable for investors cementing rate cut expectations by the FOMC next week.

Now when the August retail sales were reported, here is what the Census Bureau outlined: U.S. retail sales got a big boost in August from purchases of new autos and building supplies, but most other stores reported weak or declining receipts in a sign that consumers trimmed spending toward the end of summer. Retail sales rose 0.4% last month, the government said Friday, but sales were flat excluding new cars and trucks. In short, BofAML was extremely wrong with their tracking and forecasting for monthly retail sales!!

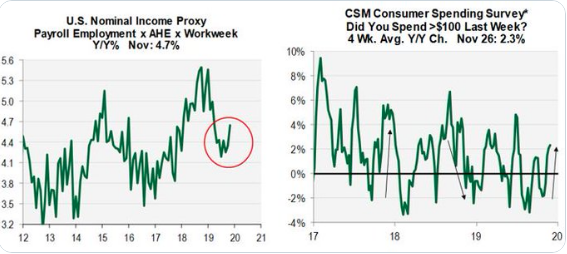

As we await the latest retail sales report, it’s also important to recognize the difference in the strength of the consumer from monthly retail sales. Again, monthly retail sales can have hiccups and for a wide variety of reasons, so we don’t put too much emphasis on any singular monthly retail sales report. We discussed this subject matter in this weekend’s Research Report:

“Retail sales do not always correlate to the strength of the consumer and consumer spending. Retail data is volatile, and one disappointing month doesn’t make a trend, which is something we’ve already seen this year. Consumer spending accounts for 70% of the U.S. economy, but retail sales make up less than half of that figure. The category also includes spending on services like healthcare and education. Although retail sales have slowed recently, consumer spending as a whole has expanded at a 4% annualized pace over the past five years. Over time, retail data will rise and fall with broader GDP and labor market trends.

Consumer spending is driven by income and wealth: The labor market says more about the state of the consumer than retail trends do.”

It seems like, nowadays, every research firm and big money center bank has a proprietary retail sales tracking strategy or system of data gathering. Cornerstone Macro is no different. Cornerstone Macro’s Nancy Lazar highlights that holidays sales appear healthier than previously thought, given the recent acceleration in core personal income growth. “Our proprietary survey of consumers also shows that consumer spending plans have improved going into 4Q.”

It would seem as though Cornerstone Macro’s research for growing retail sales also maintains labor market and personal income components. We reiterate our sentiment: “Consumer spending is driven by income and wealth: The labor market says more about the state of the consumer than retail trends do.” With that being said the latest Nonfarm Payroll data showed a strong trend of job growth, although moderating to slower growth on a YoY basis.

The Bureau of Labor & Statistics Nonfarm Payroll report came in much higher than expected for the month of November. some 266K jobs were created during the month of November, as the unemployment rate dipped to 3.5 percent. Even if we strip out some 40K+ jobs from the GM auto union strike that were added back to the Nonfarm Payroll growth in November it would have totaled more than 200K jobs added for the month, above the 3-month trend. The prior 3-month rolling average of 189,000 jobs added is a better assessment of the U.S. labor market’s ability to generate incremental hiring. That is enough to absorb population growth and keep unemployment low.

Moreover, there’s another less followed or discusses aspect of the labor market statistics that identify strength in the labor market; African American unemployment. According to studies from DataTrek, this cohort of workers has been historically vulnerable to U.S. labor market downturns, leading any upturn in general unemployment trends. Here are November’s data/recent trends:

- Last month’s unemployment rate here was 5.5%. This is the same as the prior 3-month average and lower than 2019’s average reading of 6.1%.

- Labor force participation rates remain stable at 62.3% in November, the same as the 2019-to-date average.

- African American unemployment remains low and participation stable is a very positive sign about the U.S. labor market.

No matter the reason, November’s Jobs Report is one more indication that it’s not just capital markets that believe in the promise of earnings growth in 2020. Corporate America clearly buys that storyline as well. All the more reason that a US-China trade deal needs to happen soon, before companies decide to trim headcount.

We can’t predict whether or not the tariffs will be implemented on Sunday. As investors, we are forced to think more long-term and with the data we have at-hand. The data suggests the ability to withstand the current and even future tariffs. There may be an adjustment period to the upcoming tariffs, but that period may also prove a brief period and find a resumption in rebounding metrics. Nonetheless, if the tariffs are imposed, it couldn’t come at a worse time for the global economy and with consumer confidence rebounding, according to J.P. Morgan.

The chart above identifies a rebound in global consumer confidence. One would hate to see the metric hit with a proverbial slap in the face, by way of a fresh round of tariffs. With that being said, Goldman Sachs economist Jan Hatizus offered the following to clients regarding the go-forward U.S./China trade negotiations/status:

Hatzius: the risks around the US-China trade policy outlook have increased again in recent weeks….

……as the two sides have yet to agree on the amount of Chinese purchases of US agricultural goods and the extent of the rollback of the existing tariffs.

“Our baseline assumption remains that China will purchase more US agricultural products in exchange for a rollback of the September 1 tariff step of 15% on about $100bn of US imports from China as well as cancellation of the December 15 tariff threat of 15% on the remaining $150bn.

If this materializes, we think the drag from the trade war on the annualized pace of GDP growth will diminish from our current estimate of 0.4pp to near zero by the end of 2020. If this assumption proves wrong and the escalation continues, however, the drag could remain near current levels or even increase from here.”