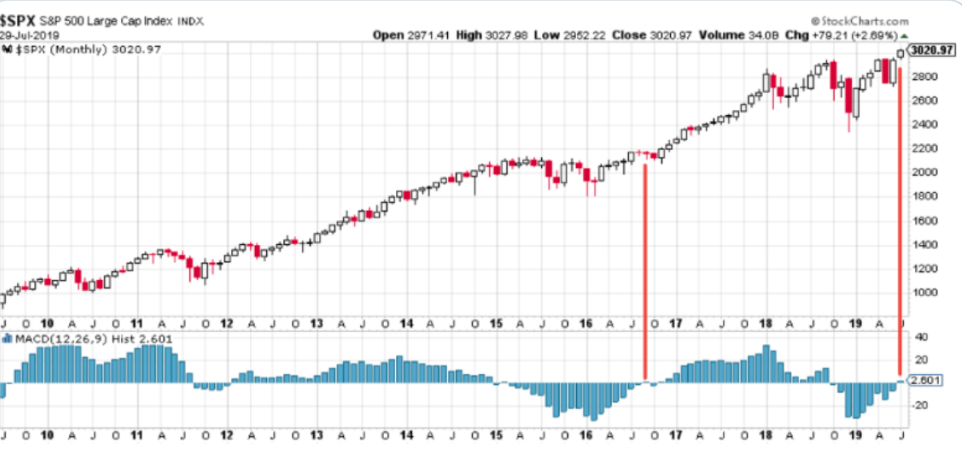

The Dow Jones Industrial Average (DJIA), boosted by shares of Apple Inc. (AAPL) was the only of the the 3 major indices finishing in the green on Monday. Investors are preparing for the potential move in markets that will come after the FOMC rate announcement on Wednesday afternoon. The Nasdaq (NDX) was led lower by tech stocks while the S&P 500 (SPX) finished off about 4 points, but still yet achieving a technical feat of strength.

Although there has been a weakening of market breadth of late, with many analysts heralding the coming correction, the S&P 500’s monthly MACD is turned positive for the first time in more than half a year. Moving Average Convergence Divergence (MACD) is a trend-following momentum indicator that shows the relationship between two moving averages of a security’s price. The MACD is calculated by subtracting the 26-period Exponential Moving Average (EMA) from the 12-period EMA.

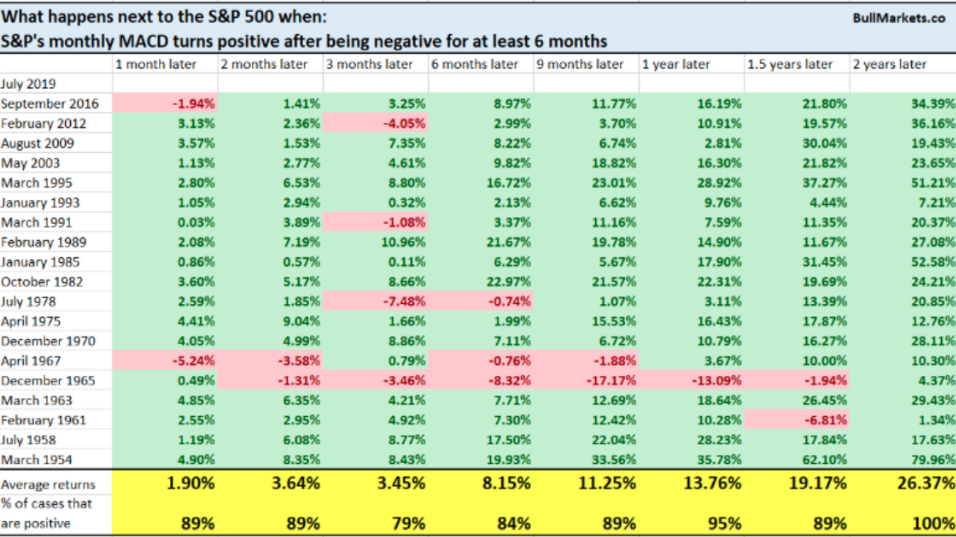

When the MACD turns higher, this is usually a bullish technical sign of things to come for the market, at least based on history. (See table from Bullmarkets.co)

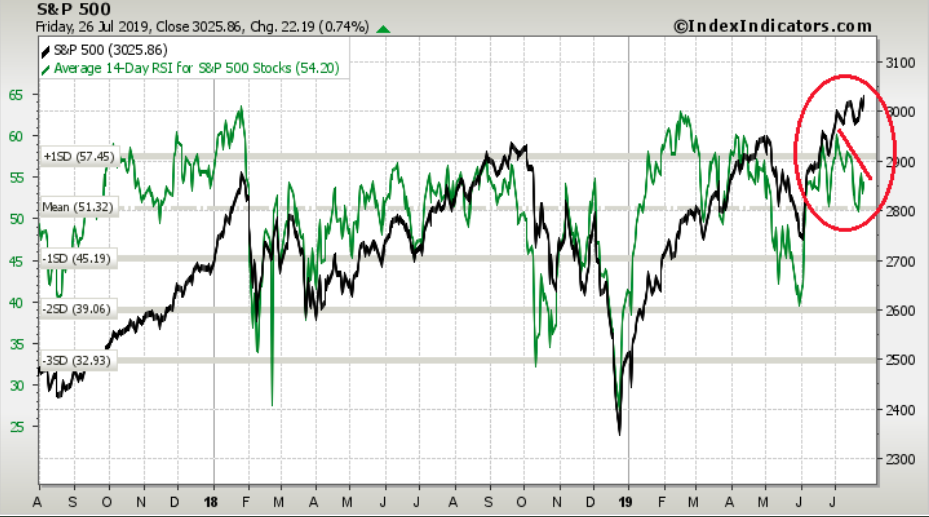

While the MACD has turned up for the S&P 500, unfortunately, the average S&P 500 stock’s momentum has begun to create a bearish divergence. We can see this in the latest S&P 500 14-day RSI. The chart below shows the S&P 500 running to new highs in July, but the 14-day RSI has edged lower during the month.

The relative strength indicator (RSI) aims to signal whether a market is considered to be overbought or oversold in relation to recent price levels.

MACD measures the relationship between two EMAs, while the RSI measures price change in relation to recent price highs and lows. These two indicators are often used together to provide analysts a more complete technical picture of a market.

One of the main problems with divergence is that it can often signal a possible reversal but then no actual reversal actually happens – it produces a false positive. The other problem is that divergence doesn’t forecast all reversals. In other words, it predicts too many reversals that don’t occur and not enough real price reversals.

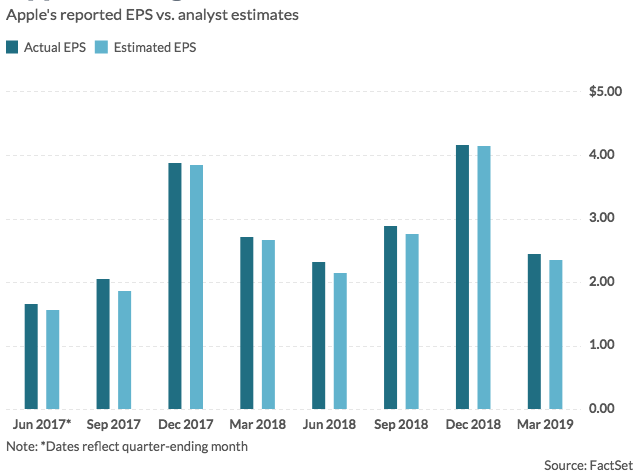

With the technical market scope out of the way, investors will refocus their attention on two main events this week and the first one of these events will take place after the closing bell Tuesday. Apple Inc., alongside a host of other multinational companies, will delivers its highly anticipated results ahead of the FOMC rate announcement. Going into the report, AAPL shares are up some 33% in 2019

UBS analyst Timothy Arcuri raised his price target on AAPL to $235 from $225 on Monday. While he said that the upcoming results are “unlikely to be [a] material catalyst,” he sees low expectations going into the report. “Even if this year is subdued, it only sets up for a stronger 5G cycle in 2020 (at least two models),” Arcuri wrote. “Apple has traded with the market in the recent weeks, but July/Aug are historically the best months to buy for three-month return and we slightly bump up our target.”

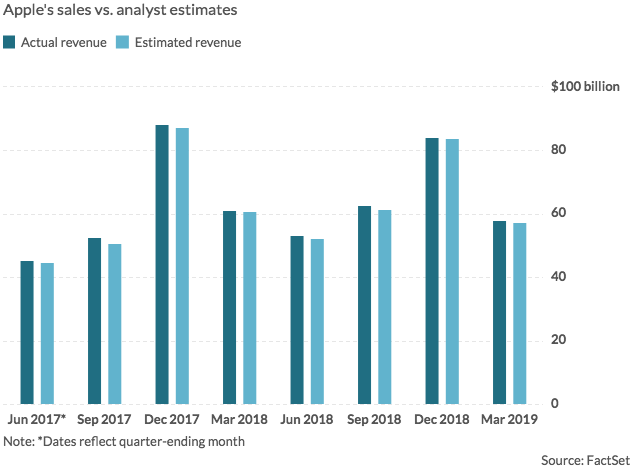

Analysts surveyed by FactSet expect that Apple earned $2.09 a share in the June quarter, down from $2.34 a year earlier.

The FactSet consensus calls for $53.3 billion in June-quarter revenue, while the Estimize consensus projects $53.7 billion. The company gave a forecast of $52.5 billion to $54.5 billion. A year prior, Apple recorded $53.3 billion in quarterly revenue.

Morgan Stanley’s Katy Huberty has called Apple’s earnings setup “attractive,” also citing analysts’ low expectations for the September forecast. Her look at third-party iPhone data suggests that trends are improving for Apple in China, which could come as welcome relief after quarters of uncertainty. She rates the stock at overweight with a $247 target price.

Instinet’s Jeffrey Kvaal is also upbeat about the modem-business acquisition, calling it a “savvy move” that’s in line with Apple’s historical ability to benefit from vertical integration. As for Apple’s actual earnings numbers, he doesn’t see room for an inflection in either services or devices, and he rates the stock at neutral with a $180 target.

CNBC Mad Money host Jim Cramer suggests that Apple’s report, if better than feared, can boost the stock and the entire market.

“I know it’s a big week for earnings, but I’m really focused on Apple,” Cramer said Monday on “Squawk Box. ” “There’s a lot of thought that Apple, people are so bearish on it, that it can rally on a subpar number.

That’s been the theme: When you have this better than feared, the stocks go higher. It’s all about better than feared. People really feared this earnings period. It turns out that that fear was not justified.”

Beyond Apple’s earnings, yes, the market is more prominently focused on the FOMC and what they will say after the widely anticipated 25 bps rate cut. That’s where all the concern comes into play; what will they signal, suggest and surprise with regarding monetary policy and interest rates going forward. At this point, it’s all about what comes next, and how to communicate it, Cornerstone Macro economist Roberto Perli said.

“I bet the statement will … leave the door open to more, to at least another 25 (basis-point cut) down the road. But as for what economic threshold would trigger a further rate cut, I don’t think they have a clear idea.”

What does bode well for not just the Fed, but also investors, is that they will have no “dot plot” to consult, as they have after with every other policy move since the Fed began in 2012 to publish quarterly interest-rate forecasts from individual policymakers. This should eliminate the ever present obstacle of mirroring the dot plot with the press conference messaging by Fed chair Jerome Powell.

“Not having the projections this month gives them a lot more leeway in sending a message of ‘we’ll respond as warranted,’” said Richard Moody, chief economist at Regions Financial Corp.

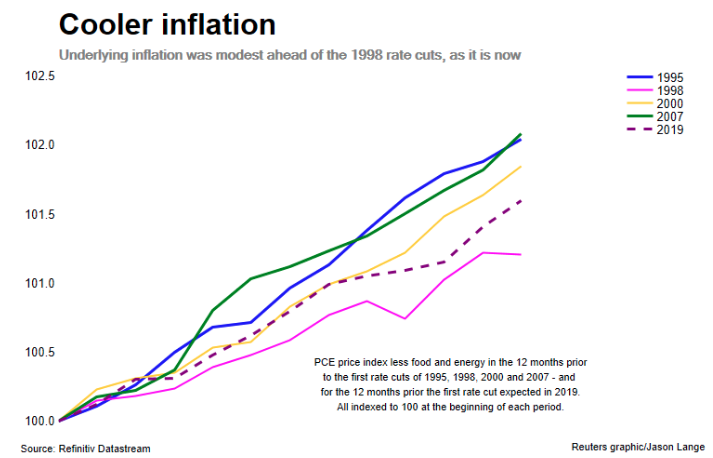

For all the media prose, consternation, speculation and hyperbolic intentions, the Fed is lowering rates due to factors appropriately aligned with, at least, its price stability mandate. U.S. consumer prices rose 1.5% in the 12 months through May, the same rate it has averaged since the Great Recession ended in June 2009. The Fed wants inflation at 2%, and weak price gains have become a defining characteristic of what is already the longest U.S. economic expansion on record. Inflationary pressures were higher in 1995, 1998 and 2007.

The central bank’s price stability mandate offers flexibility in managing the already longest expansion cycle in history. It can stoke economic growth with less worry about fueling above-target inflation. Second, some policymakers worry the persistence of weak inflation could be a signal they miscalculated how high interest rates should be to keep prices on target. That could mean they went overboard hiking rates between 2015 and 2018, which most believe they had done

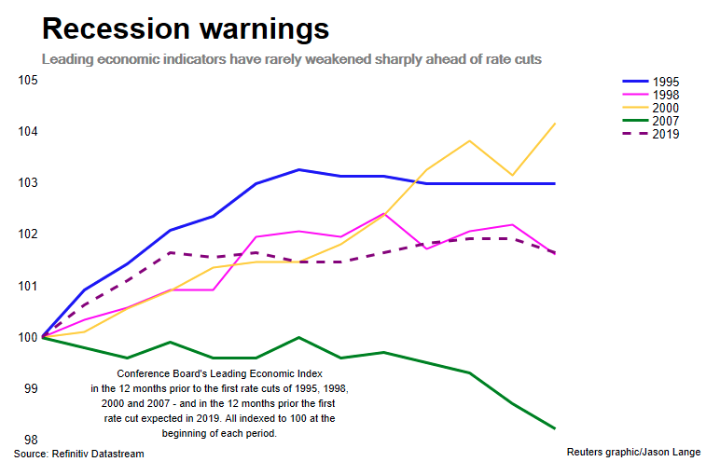

Although the FOMC is embarking on an easing cycle, the U.S. economy isn’t showing much sign that a recession is looming. The Conference Board’s index for the outlook turned south ahead of the last easing cycle in 2007, which came just before the United States slipped into a profound recession. By the time the Fed cut rates then, a recession was already in progress.

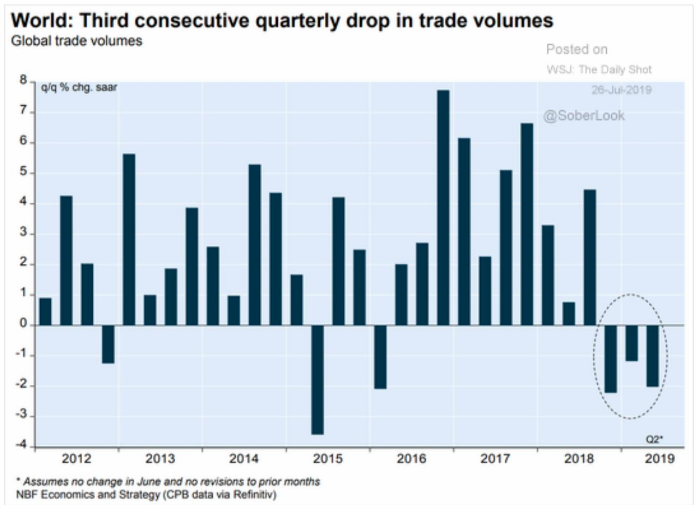

While the U.S. economy doesn’t appear to be stumbling into a recession, the global economy is certainly reeling from, what is now, a protracted trade feud between the U.S. and China. Quarterly trade volumes have been declining since the U.S. began imposing tariffs on China in July 2018.

Countries that have been heaviest hit by the trade feud are those which are dominated by manufacturing. One of the reasons the U.S. has been able to weather the trade feud better than other industrialized regions is due to its services based economy, largely bolstered by the U.S. consumer. Nonetheless, the U.S. like its peers has seen it’s smaller manufacturing sector in sharp decline through 2019 and with recent weakening in the service sector as outlined by the latest ISM index data.

The Fed is not all seeing and all knowing, but to the extent it has outlined future easing in monetary policy, it certainly has weighed concerns and impacts surrounding the ongoing trade feuds. Moreover, with an easing cycle all but started, not everyone is of the opinion it will provide a boost to economic activity. Morgan Stanley’s chief equity strategist Mike Wilson is one such analysts that doesn’t see the FOMC as being able to provide an increase in economic activity with a mere rate cut, with rates already having been so low for such an extended period. Additionally, Wilson states in his recent notes that the S&P 500 3,000 level will fail at its 3rd attempt.

“While our 2400–3000 call from 18 months ago may look vulnerable, we think this latest surge will fail again, as we don’t expect a Fed cut to rekindle growth the way market participants may be hoping, and now pricing.

While The Federal Reserve is likely to cut interest rates by 25 basis points on Wednesday, the boost from the easing will not sustain the breakout that many investors are expecting.

A growth slowdown fueled by a trade war between the U.S and China and the Fed’s policy pivot have caused interest rates to fall. This low rate environment have made equities to appear attractive when they are not, preventing a larger expansion.

Big disappointments in capital spending and business surveys suggest growth could slow further in 2H.

“We remain of the view that the consensus S&P 500 earnings forecasts are still materially too high for both the second half of 2019 and 2020 and think the Fed’s expected rate cut next week should not be celebrated if it is accompanied by an earnings and possibly economic recession.”

Wilson has been warning investors about a correction since January 29, 2019. His warnings have fell on def ears as the market has gained another 15%+ since January. While the analysis offered by Wilson is worth considering, it does beg to question if the multitude of easing around the world is more than the analyst has considered, and the impact from global easing.

Nancy Lazar of Cornerstone Macro believes that China’s stimulus-driven pick-up, a weaker dollar, and lower Global bond yields will lead to a bottoming of U.S. companies’ foreign profit growth, in turn leading to a pickup in S&P 500 earnings, which have an ~85% correlation to foreign profits.

Many regions of the world have already begun easing and expectations for more easing are ramping. It’s hard to imagine a global easing cycle that wont’ serve to bolster or backstop economies of scale from further deterioration of growth.

Somewhat contrasting Mike Wilson’s concerns and/or warnings is Goldman Sachs, which has come out in favor of equities despite the backdrop of weakened global growth. The firm determines its S&P 500 outlook on the basis of EPS going forward. The following notes from Goldman Sachs shows the firm is boosting its S&P 500 FY19 and FY2020 price target, but lowering EPS estimates.

- Lower top-down S&P 500 EPS estimates to $167 in 2019 and $177 in 2020

- Most of the reduction to our EPS estimate stems from the YTD slowdown in economic growth, lower oil prices, and weaker margins than expected, particularly in the Info Tech sector

- Our macro variable estimates suggest EPS growth will modestly accelerate to 6% in 2020 followed by 5% in 2021.

- We expect negative revisions to consensus 2020 EPS estimates in 2H 2019

- We raise our year-end 2019 price target to 3100 (from 3000) and introduce a year-end 2020 price target of 3400

- Our valuation model implies the forward P/E multiple remains stable at 17.6x in 2019, before expanding in 2020 to 18x as interest rates remain low and elevated policy uncertainty is more than offset by the tailwind from continued economic expansion.

Analysts’ opinions will always differ. What we are seeing in the way of accommodative monetary policy and possibly trough earnings growth presently suggests the worst may be behind us in the U.S., barring any future trade feud escalations/s. A mix of technicals and fundamentals don’t suggest a bear market or recession is imminent.

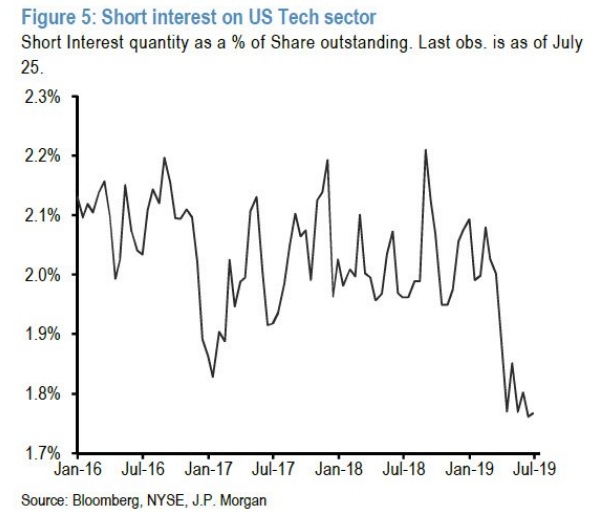

Heading into the FOMC rate announcement and with the S&P 500, Dow and Nasdaq achieving a number of new, all-time high levels in 2019, investors have also leveraged up.

And while they’ve leveraged higher it begs of the question as to how much more do they have left to buy and with multiples having extended beyond their 10-year average. The U.S. tech sector is just about as “long” as it gets and with short interest extremely low. Is this a contrarian indicator, the mark of an interim top ahead of a pullback?

Savita Subramanian, head of U.S. equity and quant strategy at Bank of America Merrill Lynch discusses the Fed and tech concentration amongst the investor community.

Savita’s research showed that institutional fund managers overlap has reached peak levels due to uncertainty and career risk. She warns investors of such funneling of capital into a small number of stocks, such as FANG stocks.

It’s a bit of a conundrum for fund managers that Savita points toward. The global economy is weakening, the SPX 2020 EPS estimates are too high and most understand that, but the Fed and global central banks are easing… how can you not be in equities? And just to make the decision that to buy equities that much more enticing…

U.S. companies are on pace to break another record for share repurchases in 2019, using a combination of cash and debt to push the total to close to $1 trillion.

Goldman projects buybacks for S&P 500 companies to total $940 billion, a 13% increase over the previous year and a new high for a number that has continued to increase through much of the post-financial crisis period. Total buyback executions among all companies this year were up 26% through mid-July.

The rise in buybacks has had a twin effect on corporate balance sheets, both drawing down cash and increasing leverage. It also represents a more-of-the-same trend that has come despite the $1.5 trillion tax cut passed in late 2017. The record cut had spurred hopes that companies would eschew the buyback formula that has helped generate the longest bull market run in Wall Street history and instead lead to more investment in equipment and personnel.

“Although we expect growth in capex, R&D, and cash M&A, we expect companies will continue to increase cash return to shareholders as they have in recent years,” David Kostin, chief U.S. equity strategist at Goldman, said in a report for clients.

Unless earnings growth accelerates materially, companies will likely continue to fund spending by drawing down cash balances and increasing leverage.”

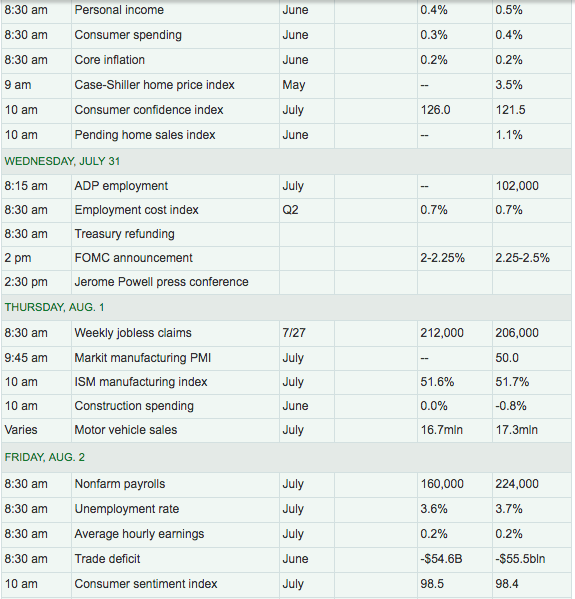

It’s going to be a very busy 2-day period for analysts, economists and investors alike. Don’t forget about the heavy economic data calendar that kicks into swing today with PCE, Pending home sales and Consumer Confidence readings.

And be sure to follow Seth Golden and Wayne Nelson on Twitter where they post their market insights and considerations daily. Yesterday, Seth offered the following morning-tweet regarding the pending Beyond Meat quarterly results:

Beyond Meat raised its fiscal 2019 outlook for revenue and expects to net sales for the full year to reach $240 million. Last quarter, in its first report since its May initial public offering, the company said that it was forecasting fiscal 2019 revenue of $210 million, a number that did not include sales from restaurants that were only testing the product.

“We’re being very conservative and viewing this as a floor,” Brown told analysts on a conference call in June.