Geopolitical headlines have tilted in favor of the bulls after a month long bearish salting through August. Remember, the S&P 500 was down over 1.5% for the month of August as Hong Kong protests, U.S./Iran sanctions took form, Brexit issues escalated and U.S./China trade relations worsened. Certain of these geopolitical issues, which have economic policy undertones that impact the global economy and corporate earnings are being met with remedies as we turn the calendar page to September. Investors came into Wednesday’s trading day with the Hong Kong government confirming the removal of the formerly introduced Extradition Bill. On the heels of this geopolitical headline, global equities surged Wednesday.

The S&P 500 (SPX) rallied just over 1% Wednesday, while the tech-heavy Nasdaq (NDX) led the way with a 1.3% gain. The Dow Jones Industrial Average (DJIA) rallied by just under 1% as investors sought out tech stocks. Mark Newton of Newton Advisors denoted his favor for tech over other cyclical sectors heading into and September and with Apple (AAPL) potentially breaking out near-term.

As a fan of CNBC’s “Fast Money” program (5:00-6:00 p.m. EST), it’s always interesting to see how the tenor and sentiment of the program mirrors that of the daily market action. This is something we encourage investors to understand and reflect upon as it has little to do with the fundamental realities of the market. Recall from Tuesday’s market drop that the Fast Money crew were heavily bearish on the day, basically aligning with the negative sentiment of the market, which was spurred by the ISM Manufacturing Index showing a contraction in the month of August.

Guy Adami, Dan Nathan and Stephanie Link all outlined their concerns for the market going forward.

“I’m not buying anything. I’m not out there buying and I’m surprised the VIX isn’t higher, said Stephanie Link.”

“Things are not bullish for stocks right now. I think the market bottom will be defined when the VIX hits 30. I think there’s a big move in the market coming and I think it’s to the downside, said Guy Adami.”

They expressed doubts over the Fed’s current easing cycle and the expression of the market, which has maintained in a tight range through August. Tim Seymour was the only panel member that suggested the range-bound S&P 500, with everything that had been thrown at it during August, might actually be a bullish signal.

With Wednesday’s market turnaround and the S&P 500 taking back all it had lost and more from Tuesday, the narrative all of a sudden shifted from the CNBC contingency. We encourage readers to watch both CNBC archived videos offered, from Tuesday’s Fast Money show and Wednesday’s “Halftime Report” program.

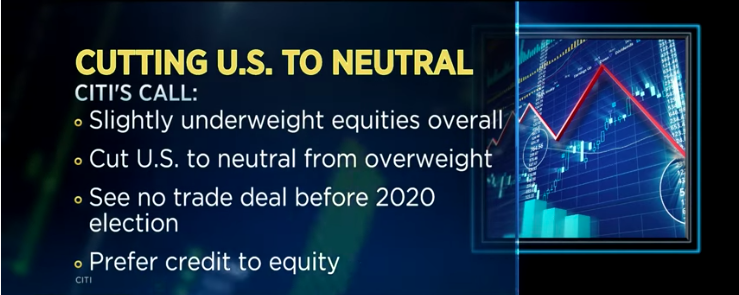

The more bullish tone on Wall Street Wednesday was not without its detractors. Citigroup cut its rating on U.S. equities to Neutral Wednesday.

The base case for Citigroup’s call is the protracted trade feud between the U.S. and China. Citi no longer sees a conclusion to the trade war with China before the next U.S. presidential election.

″[The] base case for the trade war now is no deal before the 2020 US election.”

Citi’s shift represents a departure from others on Wall Street who see a trade deal likely happening before the election next year. UBS in May said a trade deal was not imminent but should be expected “just before 2020.”

“Implied probabilities of a 2020 recession are now high enough to warrant caution.”

It’s not exactly the best timing for the call from Citi, as global equity markets continue to rally into Thursday on yet another geopolitical headline. More to the point, the headline is centered on the very reasons Citi reduced its equity market rating, U.S./China trade. Asian markets gained in early trading Thursday after an announcement that the U.S. and China will resume trade negotiations early next month. China’s Ministry of Commerce announced early Thursday that the two sides will meet in Washington in early October.

Investors also were cheered by encouraging global developments, including British lawmakers seeking a less chaotic exit from the European Union. In Europe, Britain’s parliament took a big step toward passing a law that could stop Prime Minister Boris Johnson’s plan to pull out of the EU on Oct. 31 with or without a withdrawal agreement. Leaving the EU without a deal that covers trade and other issues could result in economic chaos for Britain and complicate trade with member nations in the EU.

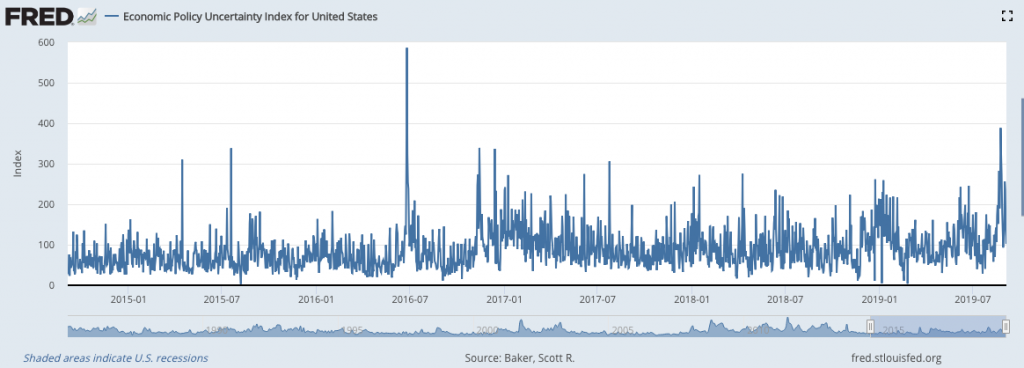

Geopolitical headlines have been the key driver for markets throughout 2019. No, it’s not safe to say that implied and now commenced central bank easing cycles have fueled the markets. Even after the FOMC lowered rates by .25 bps in late July, equities failed to rally. The main market driver and consideration from the greater contingency of investors is that which is more geopolitically charged. Investors know what to expect from the Fed during economic slowdowns, an easing of financial conditions. Investors don’t know what to expect from the White House Administration policy makers, be it on trade or a plethora of other economic issues. To that point, the Economic Policy Uncertainty Index for United States has remained extremely elevated.

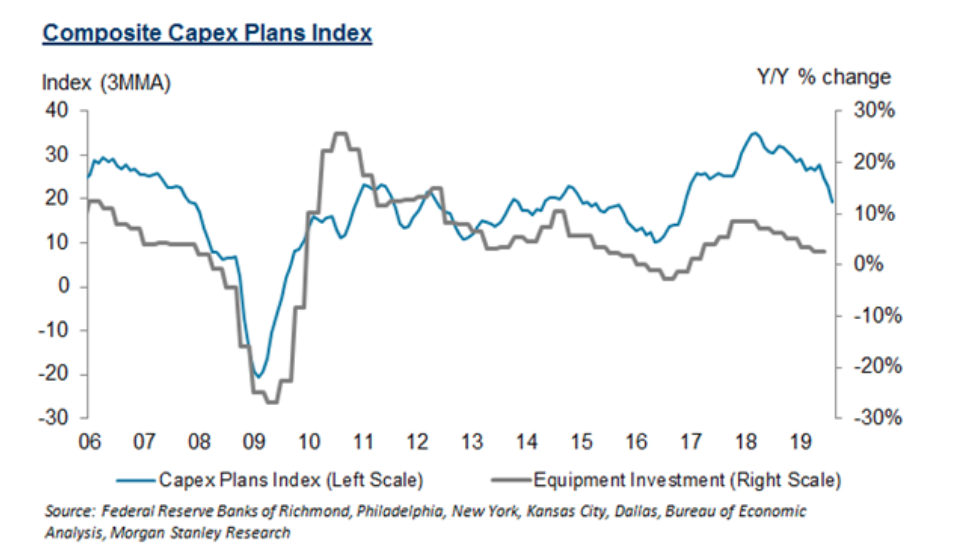

The uncertainty surrounding economic policy is quite astounding and we would suggest that investors not hang their proverbial hats on U.S./China trade talks in October. The likelihood that any breakthrough at these meetings in October remains minute. Should the meetings lack anything meaningful that drives greater business certainty which would lend itself to a rebound in CAPEX spending, the damage to the global economy is unlikely to abate. Both Capex Plans and Equipment investment have faltered throughout 2019 after a ramp in business expenditures and investment in both 2017 and early 2018.

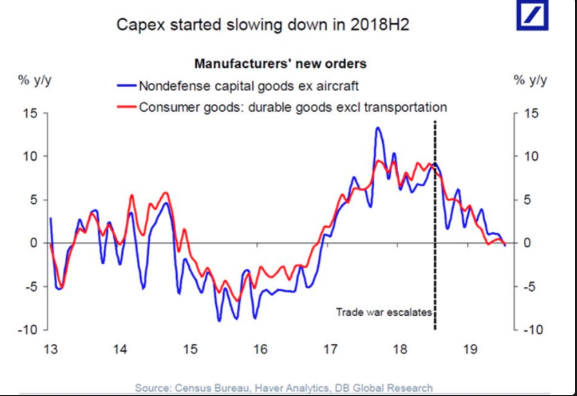

Deutsche Bank has noted its concerns about the trade wars impact on Capex recently. They denote and depict the slowdown in Capex that begin shortly after tariffs went into place, going into the Q3 2018 period.

“We are getting more and more worried about the impact of the trade war on capex spending.”

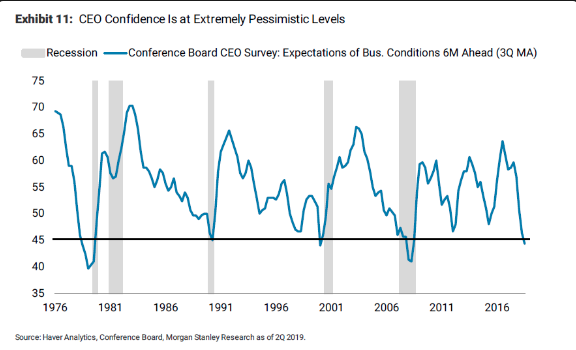

CEO pessimism over the probability of a U.S./China trade resolution near-term remains very low as reflected in their overall pessimistic tone according to the latest survey results from Morgan Stanley.

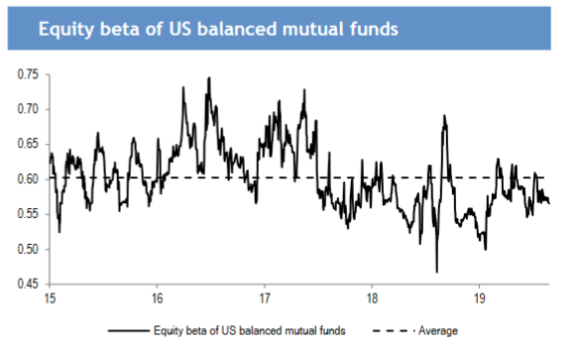

Switching gears for a moment as we denote the fears over the economy and that which finds many financial firms shying away from equities… The average investor shouldn’t feel as though they are missing out on big market moves. You’re not alone in that camp and no lesser than that of the “big boy” funds, which have been less exposed to equities than in past years. Long/Short hedge fund equity beta (L/S) is little changed, at 57% decile, on the year, according to J.P. Morgan.

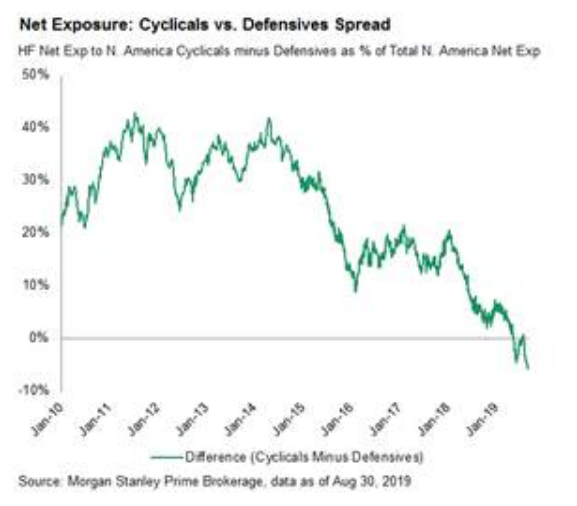

And to point out where the greatest market exposure is taking place in equities, Morgan Stanley denotes that cyclicals are still vastly underperforming defensive sectors of the market.

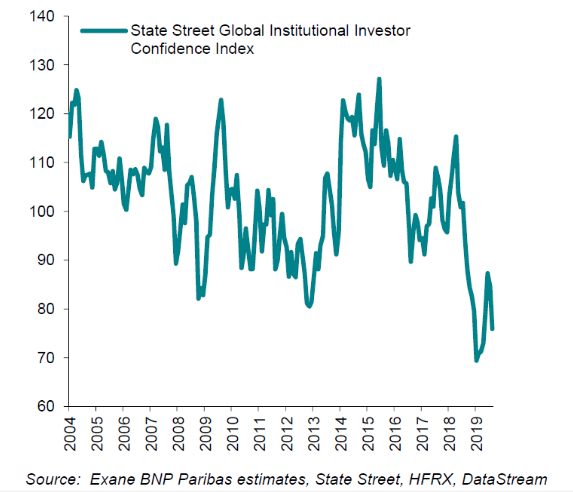

Why are investors so defensive with equity exposure and/or positioning? No confidence! Be it in the domestic or the global economy, investor sentiment, even at the institutional level remains quite low. Such low levels have not been seen since the December 2018 period.

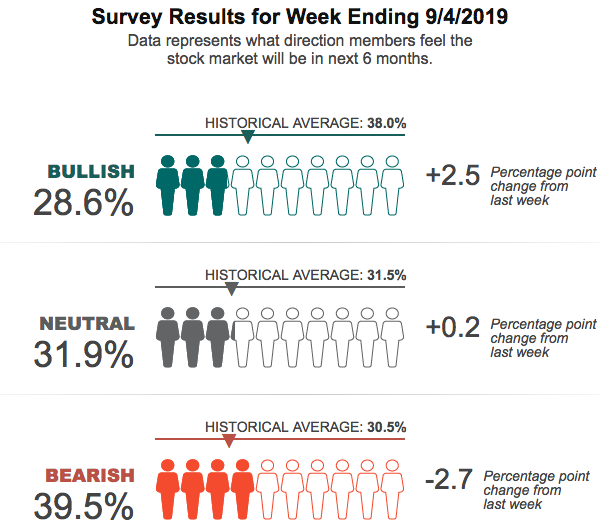

Investor sentiment hasn’t improve meaningfully amongst individual investors either, even with last week’s market rebound of roughly 2.5 percent. According to the latest AAII survey results, bullish sentiment improved only 2.5 points last week, but remains below the historical average of 38.5 percent.

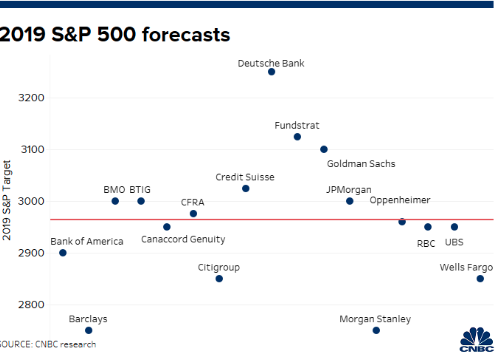

Reverting back to our previous comments that outline Citigroup’s lowered rating for U.S. equities, let’s face facts, analysts and firms are all over the map with their ratings and forecasts for equity markets/S&P 500. In 2018, it seemed as though firms were more aligned and with a more favorable outlook for the S&P 500 than in 2019. Leading stock forecasters differ greatly on where the S&P 500 will go in the final four months of the year compared with predictions made the same time a year ago.

Strategists at Wall Street’s top brokerages and investment banks see a broad array of possible outcomes by the end of December with Deutsche Bank calling for an 11% rally to 3,250 while Barclays and Morgan Stanley seeing another 5% downside from current levels to 2,750.

That map of forecasts looks rather muddled and with quite the range of expectations. The 17 top stock prognosticators tracked by CNBC’s Market Strategist Survey show Wall Street, on average, sees the S&P 500 drifting 2.2% higher from current levels by the end of the year. But the standard deviation between their forecasts, a gauge how spread out the guesses are, was 127 points or 4.4% of its current level.

The latest update to a strategist’s stock-market expectations came on Tuesday, when Bank of America’s Savita Subramanian updated her outlook to reflect “trade talk, political campaigning & tweets.”

Subramanian left her 2,900 forecast untouched and noted that investors have been hesitant to rejoin the equity market, she wrote that geopolitical headwinds are enough to keep her on the sidelines for now.

“Dovish central banks and tepid equity positioning are supportive, but trade tensions/global growth concerns/geopolitical risks plus signs of margin compression and further downward risk estimates are likely to limit upside going forward. These warring factors leave us neutral on the S&P 500.

Finom Group’s chief market strategist Seth Golden had initiated a new 12-month S&P 500 target of 3,120 back in July and after achieving his 2,950 price target this year. The Finom Group outlook is one that outlines both headwinds and tailwinds for the market as follows:

Tailwinds

- Central bank easing cycle

- Peak trade conflict in 2019

- Peak Dollar in 2019

- Strong labor market

- Best Household debt:income ratio in 50 years

- Delinquency rates remain very low

- Generally easy financial conditions

- Rate of change for EPS cycles from low to moderately higher

Headwinds

- Brexit resolution remains ambiguous

- Economic policy uncertainty in election year

- China economy continues to slow

- Exogenous shock to economy

- Recession talks foster self-fulfilling prophecy

While the headwinds to the market outlook are more limited, they are not without their merits. The media will always focus on the negative, hyperbolizing fears of market declines and recessions. In that sense, the main bullet points of concern regarding market headwinds going forward are the rise of an exogenous sock (9-11, Subprime Mortgage Meltdown) and/or the self-fulfilling prophecy for a recession. Sometimes, market downturns/correction can contribute to the self-fulfilling prophecy thesis. We saw what happened to retail sales last December, as the market melted lower into Christmas Eve.

The wealth affect from the stock market is a living, breathing organism that resides within the consumer. When the consumer sees a steady stock market, they feel more confident in their jobs and it filters down to their spending plans and activities. Former FOMC chairman Alan Greenspan recently discussed these principles of the economy as it pertains to the stock market somewhat feeding into economic activity.

“Strangely enough, it’s going to depend in large part on the stock market,” Greenspan said on CNBC’s Squawk on the Street. “We underestimate the wealth effect on the economy and this type of volatile stock market moves, it has an impact which I don’t think we fully understand nor measure correctly.” Wealth effect suggests people spend more when the value of their assets rise.

I think it’s important to recognize that if we get a major stock market adjustment, we are going to feel it in the economy, which has very short lag.”

Most recessions are indeed self-inflicted. It comes by way of economic policy missteps or self-fulfilling fears that underline expansion cycles, especially when those expansion cycle press upon extreme duration. In kind with Greenspan’s articulations, Robert Shiller, the Nobel-prize winning economist and Yale professor, says he’s not convinced the yield curve is a leading indicator of the next recession this go round. He says public panic could be the real driver of a recession after the longest expansion cycle in U.S. history.

Shiller states that while the yield curve has preceded each of the seven recessions since the 1950s, with only one false positive, it’s a fairly small data set to be really conclusive.

“A lot of what happens with the markets is a “self-fulfilling prophecy. I hear so much talk about a market correction, it might make it happen.”

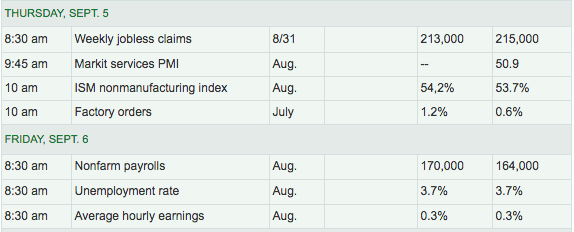

We’ve a great deal to consider as investors every single week of every single month of every single year, but only if we choose to worry about that which eventually finds resolution. A long-term approach to investing is usually that which lends itself to a better nights sleep. With that being said, the market still has a lot of work to do near-term for which will likely be governed by certain economic data releases Thursday and Friday. The private sector ADP payroll report is due out a 8:15 Thursday and accompanied by Initial Jobless Claims at 8:30 a.m. EST.

After an abysmal ISM Manufacturing Index report earlier this week, the ISM non-manufacturing data will be released at 10:00 a.m. EST Thursday. The more pressing report on investors’ minds will come by way of the August Nonfarm payroll report Friday. We’ve seen a significant YoY decline in the number of jobs created on a monthly basis, although the unemployment rate has remained at record low levels.