Wall Street is waking up to equity futures and bond yields moving in opposite directions. U.S. treasuries had their largest moves on Wednesday, since June 2011. The 10-yr. Treasury yield climbed over 15 bps to 3.18% and has since moved higher on Thursday morning. It’s not that yields are rising that is causing a modest sell-off in equities this morning, but rather the pace of the rise. Bond yields rising for the right reason is actually a good thing and supposed to occur. The market is a little spooked either way, but the better news is that the yield curve has actually steepened. With the recent rise in the 10-yr. vs. 2-yr. yields, the curve has steepened by roughly 10bps this week alone and since the announced Fed rate hike a week ago.

So what are the “good” reasons for rising rates? We’re glad you asked! The answer isn’t as dramatic as one might think and something probably well known: A strong economy. A strong economy should express higher or rising rates and/or yields. Yesterday’s ADP report showed that the U.S. economy is strong and possibly strengthening that much more into the final quarter of the year.

Yet another piece of the economic puzzle pointing to a strengthening U.S. economy came in the way of the ISM services index on Wednesday. The Institute for Supply Management’s survey of non-manufacturing firms climbed to a 21-year high of 61.6 last month from 58.5.

It’s the highest mark of the current 9-year-old expansion and the second strongest reading in the history of the index. The latest ISM survey shows little likelihood that growth will slow anytime soon.

“A robust report, consistent with further strength in the overall economy,” said chief economist Scott Brown of Raymond James, who added that the strong pace of U.S. growth all but assures the Federal Reserve will raise interest rates again by December.”

The strength in the economy gives the Fed ample reasoning for continuing on their rate hike path. The Fed is scheduled to hike rates one more time in 2018, during the month of December. In recent comments, Fed Chairman Jerome Powell offered the following, which indeed does fall inline with the latest rounds of economic data:

“Business cycles don’t last forever, but there is really no reason to think that this cycle can’t continue for quite some time.”

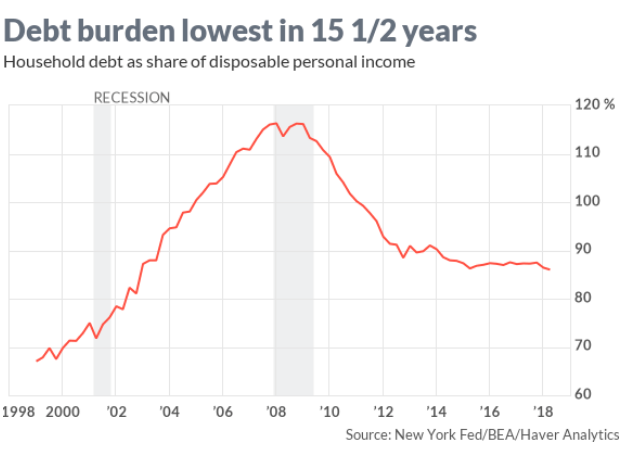

Regardless of the supportive reasons for rising rates/yields, the media cycle will play on the fears of investors, promoting that higher rates are not only inflationary, but a drag on the economy. The reality, that won’t make for much airtime, is that rates are rising from very depressed levels. Even with the 10-yr. Treasury yielding roughly 3.22% at present, it is not near the levels reached prior to the Great Financial Crisis at above 5 percent. Another point to remember, as it will also be forgotten in the news cycle, is that wages are rising alongside rising rates, even if not as quickly. On that note, the consumer has the ability to absorb higher rates, as shown in the chart below.

The debt burden of U.S. households is the smallest it’s been in nearly 16 years. Again, this will likely get absolutely no airtime in the media. Household debt, including mortgages, credit cards, auto loans, student loans and other credit, grew for the 16th consecutive quarter in the April-to-June period, rising by 0.6%, or $82 billion, to $13.29 trillion, according to the New York Fed.

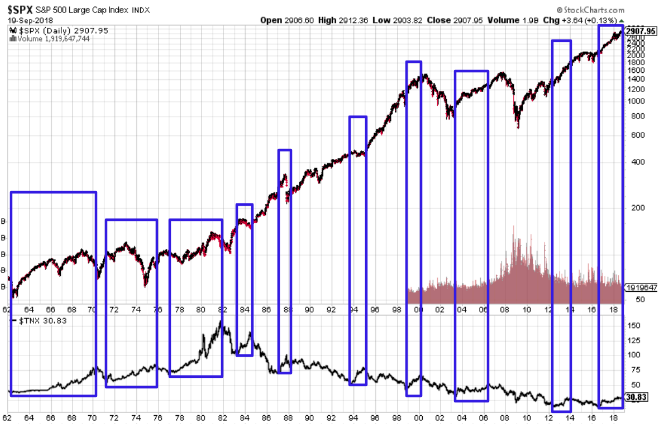

The fact is that interest rates and/or yields are going up; it’s a rarity as the path of least resistance is for rates to go lower over time. In fact, that’s really the only thing rates do… over time. And there will be another snap back in rates from the current spike. But in between now and then upticks can and do occur. The U.S. is in the middle of one of those rate upticks, which actually began in mid-2016. The following chart depicts the movement of the 10-yr. yield (TNX) and the S&P 500 (SPX).

So if you’re overly focused on selling stocks into rising rates, as shown in the chart above, you’re likely not making a sound, long-term choice. Remember earlier this year how the 10-yr. Treasury yield first tipped over the 3% mark and everyone became obsessed with interest rates rising? Remember they said, “The stock market will fall because interest rates are going up”? And yet the market did quite the opposite after a hissy fit, of course. So now here we are again, with rates/yields on the rise and ahead of more economic data to be announced.

The economic calendar in the U.S. on Thursday includes weekly Jobless Claims at 8:30 a.m. ET, and Factory Orders for August at 10 a.m. On Friday, investors will get another look at the labor market and wages by way of the Nonfarm Payroll report. Earnings reports are expected Thursday from Constellation Brands Inc. (STZ) and Costco Wholesale Corp. (COST). Next week kicks-off earnings season with the financials set to report quarterly results.

Finom Group’s chief market strategist Seth Golden urged subscribers back in February to continue monitoring the progress of the economic data and earnings, shorting volatility and buying stocks along the way. The short-term pain led to long-term gains. The short-term pain from rising rates of today, may be lending itself to another opportunity for investors/traders; time will tell.