On Monday, SocGen’s equity derivatives team cautioned that in addition to possible “further de-grossing in hedge fund balance sheets,” last week’s events could also “manifest in another pullback from vol sellers.”

The bank’s Jitesh Kumar and Vincent Cassot noted that there are “already signs of excessive stress in the VIX complex as it is trading at extreme premiums, both to realized as well as S&P500 1-month variance swaps.”

There are myriad factors that could postpone normalization. Last week may have complicated the situation further.

Kumar and Cassot discuss the prospect of “the Reddit crowd” (and, yes, they do specifically refer to Reddit) venturing into the VIX ETP complex. As we saw in February of 2018, retail investor participation in the VIX complex (and making volatility a readily available “asset class” for the masses) can be perilous.

SocGen strikes a somewhat fretful tone while musing about what might unfold should Reddit decide to storm into volatility products.

“The fact remains that the structure of the modern financial market is simply not built to suddenly absorb a very large marginal buyer or seller – and the volatility market is no exception,” Kumar and Cassot wrote Monday. After noting that “membership of r/wallstreetbets has grown from 1.8 million members at the end of 2020 to ~8 million now,” SocGen’s derivatives team called it “ominous” that the volatility complex “has been the topic of recent discussions on the forum.”

Kumar and Cassot touched on that while trying to estimate the impact of a possible Reddit assault on the volatility space.

“While some of these recent members are likely to be hedge fund analysts trying to monitor the forum activity, even if 1.8 million original members add one additional call option on VXX or UVXY, the new flow will double the existing open interest of VXX (1.92m) and almost triple that of UVXY (1.04m),” they said, adding that “this is happening against a backdrop of already elevated AUMs and call option open interest.”

After taking a look at open interest in calls on the products, Kumar and Cassot observed that there’s “some decent existing inventory” above spot. Given that, “hedging activity from market makers could initially lead to some exacerbation in price moves on the upside,” they went on to caution.

Is that bad? Well, it’s not great. Remember: Liquidity and market depth are closely linked and inextricably bound up with one another. As I repeatedly emphasize (so often, in fact, that regular readers are probably tired of hearing about it), liquidity never recovered after the events of February 2018. A lack of market depth exacerbates directional moves, which in turn feeds into more volatility. Kumar and Cassot explicitly referenced those dynamics on Monday. To wit:

Thanks to the VIX ETP-related shock in February 2018, investors are very well aware that flows in the VIX complex can pull the wider volatility market around and a large increase in volumes/open interest on VIX/VIX-related ETPs could lead to convex upside moves. It took many weeks for volatility markets to recover from the Feb-18 VIX event. And arguably on some level, liquidity has never fully recovered.

So, how far could Reddit theoretically push the envelope? That’s not totally clear, but SocGen points to three factors that theoretically limit the impact in vol markets versus what retail investors can manage to achieve in what the bank called “penny stocks.”

For one thing, Kumar and Cassot noted that volatility is mean reverting. Additionally, they wrote that “VIX options are bounded theoretically to the pricing of S&P 500 options, and as volatility rises, the leverage in options decreases significantly.”

Perhaps the most foreboding passage from their missive came when they wrote that,

Even if volatility on penny stocks rises and options become expensive, one can always roll the strikes up to the sky. However, we would like to believe that the upside in a VIX-related option cannot continue to be rolled up forever if the investor wants a positive expected P&L. The volatility of an individual stock with large short interest can reach 500%, that of a large market cap index such as the S&P 500 arguably cannot.

I also asked Invest In Vol and 6 Figure Investing Founder Vance Harwood about the probabilities of a GME-like event within the Volatility complex. Here is what he offered:

- Liquidity: How many people can participate in this security’s market? How do outstanding shares compare to daily volume. In the case of VIX futures/Vix Options/Vol ETPs there are multiple, well developed mechanisms for dealing with flow imbalances (net selling vs buying). For futures/options no borrowing is required to service demand for shorting, the market maker can just create whatever is needed and hedge the other side internally. ETPs shorts do require borrowing shares but the eco-system is well established for doing this. Because these ETPs can be more or less perfectly hedged with VIX futures some institutions will do “create to lend” processes where they create shares, loan them out—for a fee, and hedge their long positions with VIX futures. It’s a luxury having a parallel market that enable this precision hedging.

- Leveraging effects: Short term options can require significant delta hedging in the underlying by the market maker (MM). This can result in significant positive feedback effects because the MM delta hedging is real, relatively price insensitive demand. The MM’s capital is effectively leveraged to create more demand.

- With a stock like GME there are no real alternatives for the MMs to buy or sell, nothing else is correlated well enough. With Vol ETPs there are a myriad of choices, in addition to the ETP itself, the underlying futures, other vol ETPs, options for each of these, and for the more sophisticated the SPX options market can be tapped also. The MMs are adept at using all these tools. Exchanges offer tools like Exchange for Physical (EFP), also called Exchange of Contract for Related Position (ECRP) that allow efficient conversions between VIX futures and VIX options and vol ETP shares.

- Short interest: How many shorts are out there

- Time concentration: With Vol ETPs the known rolling & releveraging requirements are focused at end of day settlement. This is an open invitation to front runners to try to game the close. This likely caused the 5-Feb-2018 volatility Tsunami. Recent CBOE changes to move the settlement to 4PM ET and soon to go to a 30 second VWAP right before close will make the vol market much less susceptible to liquidity holes. A few more thoughts:

- VIX levels / VIX Futures levels are running significantly higher than realized volatility. This suggests to me they will be tougher to move up, the premium over realized is already high from a valuation standpoint

- I do think the ETPs are significant drivers on the VIX futures market. I think institutions are likely getting better at using SPX options to backstop the VIX futures, but this is a complex problem that gets even tougher when the market is disrupted. It takes a lot of capital / operational sophistication to hedge VIX futures with SPX options

- Long side assets in the Vol ETPs have been growing rapidly recently. UVXY+VXX+VIXY is around $4B. This the highest it’s been since March 2020. If there are big VIX futures moves there will result in big end of day releveraging trades required, but this is not a new problem in this space.

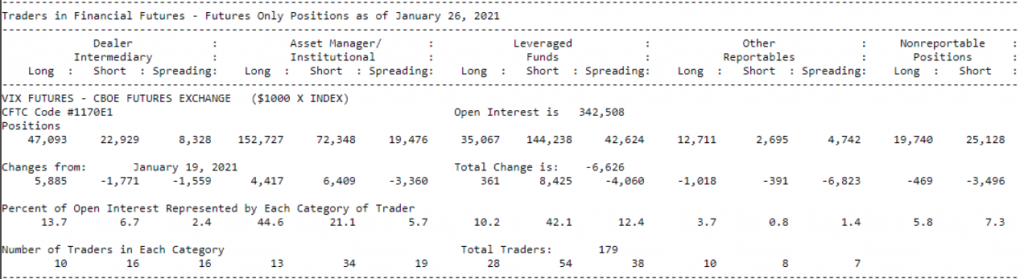

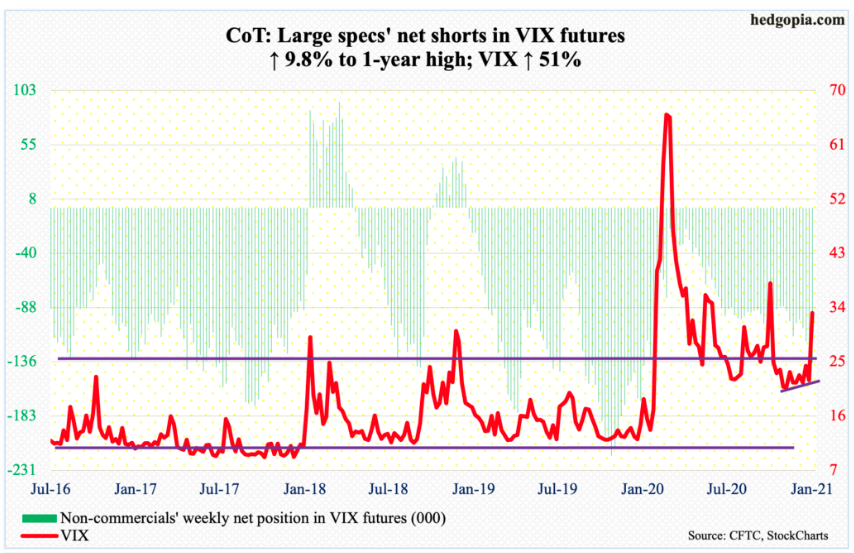

- The newer CFTC report https://cftc.gov/dea/futures/financial_lf.htm… with VIX futures at the end indicates that there is quite a bit of short positioning with the “Leveraged funds”, which is players other than MM & the ETPs themselves (attached) .

- This link gives some definitions https://cftc.gov/sites/default/files/idc/groups/public/@commitmentsoftraders/documents/file/tfmexplanatorynotes.pdf… I don’t see any particular driver of problems with these numbers.