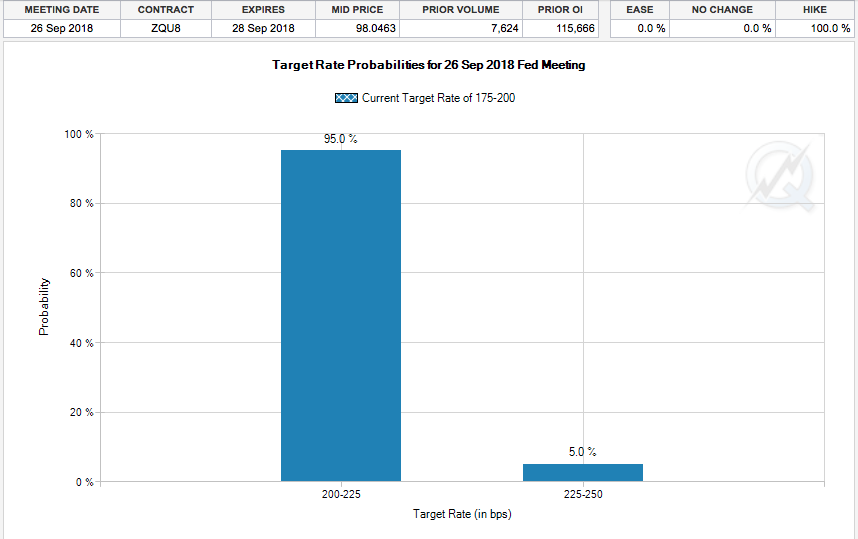

It’s not quite Monday Night Football, but Fed Chairman Jerome Powell’s press conference will prove to be “must see T.V.” shortly after the FOMC delivers a .25 bps rate hike today at 2:00 p.m. Easter Standard Time. The rate hike is not in question, but rather how the FOMC has parsed out its mandates on inflation and the future path of projected rate hikes. At present, Fed Futures contracts show a 95% chance for the Fed to deliver a rate hike today.

According to respondents to the latest CNBC Fed Survey, a full 98% of the 46 respondents, who include economists, fund managers and strategists, see the Fed hiking rates a quarter point this week to a new range of 2 to 2¼ percent. And 96% believe another quarter-point hike is coming in December. A December rate hike is showing a probability of over 70% presently according to the CME’s FedWatch Tool.

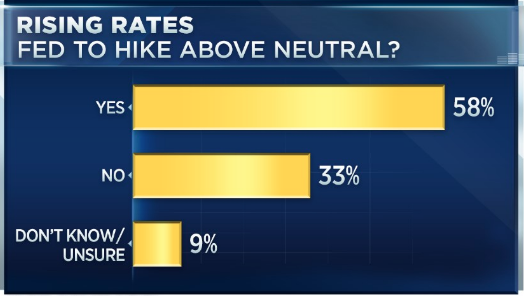

About 60% of the group sees the Fed raising rates above neutral to slow the economy. The average that respondents see the funds rate eventually ending this hiking cycle is 3.3 percent. What is on the mind of most investors with regards to all things Fed-related, but most importantly rate hikes, is how fiscal tightening will affect equity market returns.

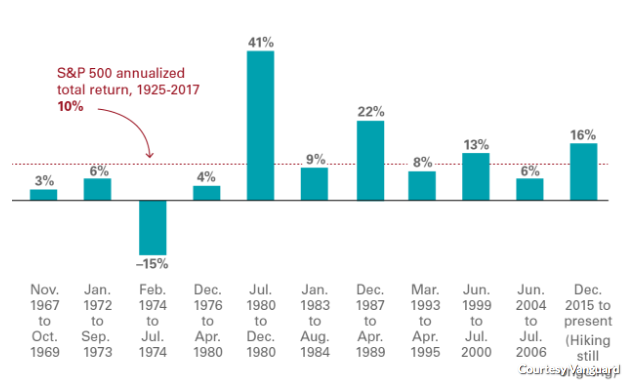

According to Vanguard, periods of rising rates almost always coincide with market gains, even if the move higher in stocks is typically modest. The asset-managing giant looked at data covering the past 50 years, which included 11 periods where the Fed raised rates. The market rose in 10 of the 11 periods, as displayed in the following chart.

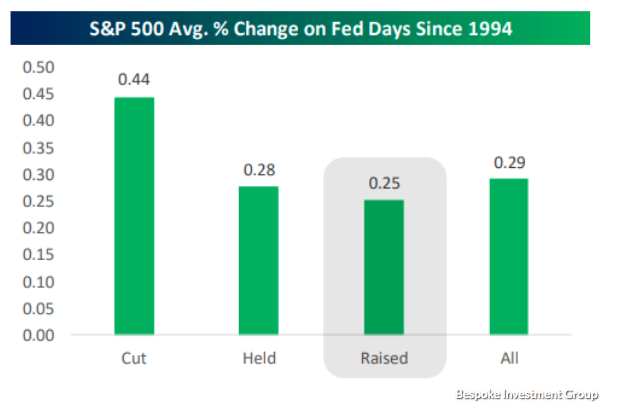

For all years, not just those with rising rates, Vanguard said the annualized average gain is 10 percent. In seven of the 11 periods, rising-rate environments coincided with gains that were smaller than that. While stocks do indeed perform well during rate hike cycles, the day a rate hike is delivered, lately markets tend to react with outsized volatility and decline on the day. Data published by Bespoke Investment Group Tuesday indicate that stocks, on average, fell 0.13% on the last 10 times the central bank held its policy meetings. Longer-term, stocks have done well on Fed Days with the S&P 500 rising an average of 0.28% since 1994 versus the average 0.03% for all trading days.

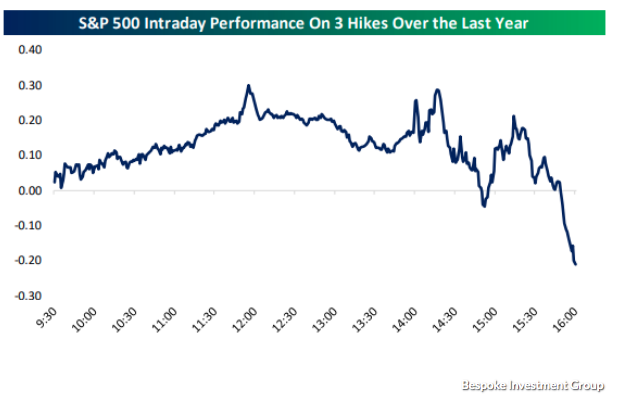

Moreover, the last 3 Fed days have initially found the markets trading well once the Fed announces its rate hike decision, but quickly reversing course thereafter and into the closing bell.

While the historic data suggests a post rate hike market pullback, history may not be our best guide given the unique timing of today’s rate hike announcement. This September will mark the first time ever that the FOMC has hiked rates in the month of September. The September rate hike will come on the heels of a rather strong performance for the markets, thus far, during a month that is usually characterized as the worst trading month of the year. Recent gains in the stock market are also encouraging given rising interest rates. Since August 24, the 10-year yield has moved from 2.81% to 3.06% while the S&P 500 is up about 3 percent. While market pundits tend to proliferate the idea that rising rates portend poorly for equities, history shows quite the opposite performance relationship.

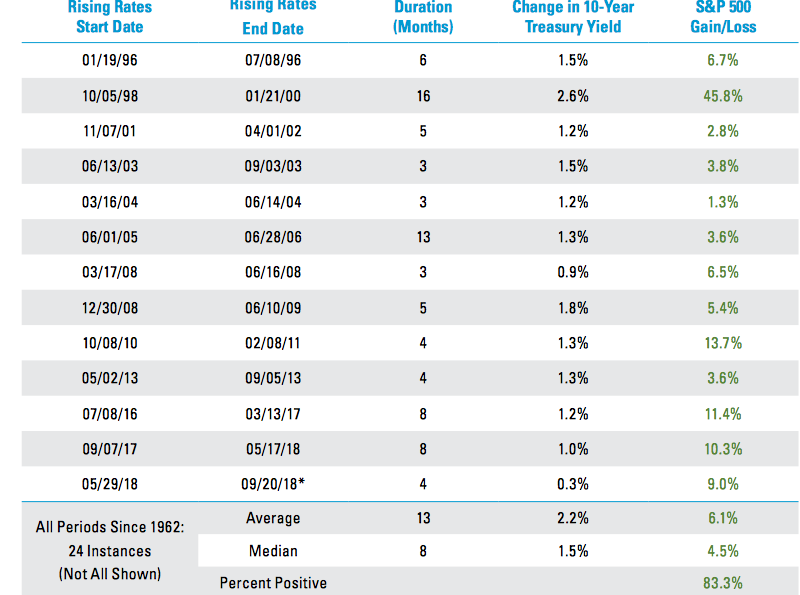

Historically, stocks have done quite well when rates rise, particularly over the past three decades as displayed in the chart from LPL Financial. In fact, since 1996, stocks have risen with higher rates every single time. Since 1962, the S&P 500 has gained an average of 6.1% during the rising rate periods, with gains in 83% of those periods (average increase in yield of 2.2%, average length of time of 13 months).

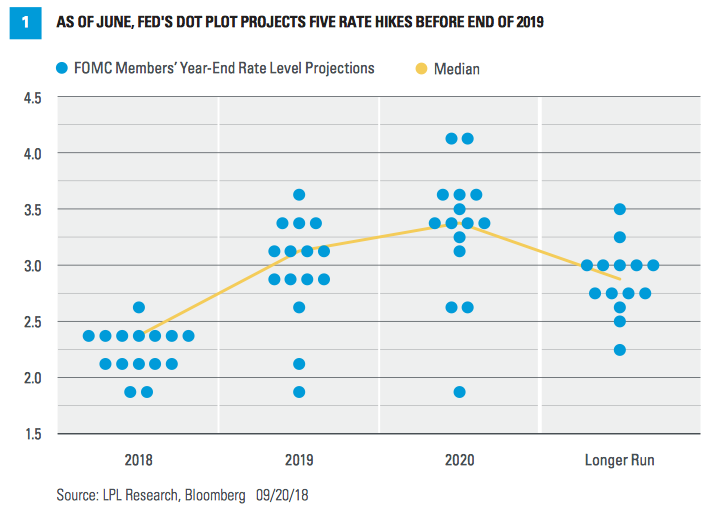

As the rate hike will be delivered firstly at 2:00 p.m. EST, investors’ attention will largely shift from the current fed funds rate to the Fed’s projections for future policy and economic growth. Investors, analysts and economists will review the Fed’s words for clues on the “neutral rate,” or the point where monetary policy is neither stimulative nor restrictive. Just where the so-called neutral rate sits is the subject of keen debate within the Fed; with officials saying it could be anywhere between 2.3 percent and 3.5 percent in the longer run. Shift above it and the economy may cool down goes the theory. But undershoot it, and even lower unemployment and higher inflation are likely. From that point of interest, onlookers will then turn to the Fed’s dot plot, which serves to underscore the Fed’s longer-term neutral rate beliefs.

The median dot plot forecasted four rate hikes in 2018, which would put the fed funds rate at 2.25-2.50 percent. The 4th rate hike for 2018 would likely come in December. In 2019, the Fed is signaling a slow down in rate hikes that depends on its updated forecast and which presently depicts 3 rate hikes in 2019.

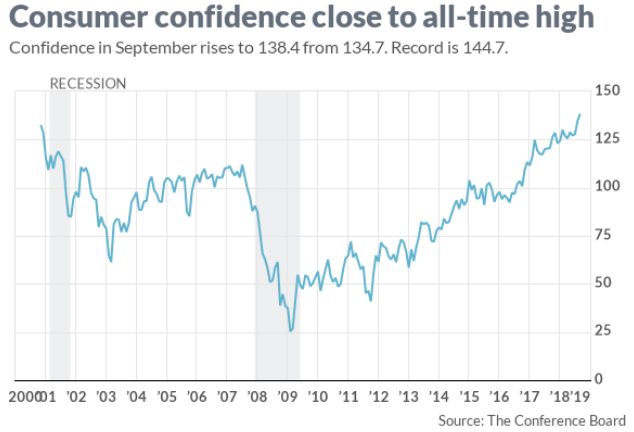

With much of the day aimed squarely on the Fed, yesterday’s Consumer Confidence data may have gone overlooked by investors. The most recent survey, however, shows that Americans are the most confident in the U.S. economy in 18 years and the level of optimism is not far from an all-time high. The consumer confidence index climbed to 138.4 in September from a revised 134.7 in August, the Conference Board said Tuesday. This is the highest level of consumer confidence since 2000.

Americans expect business conditions to improve, and they say plenty of jobs are available. They also think their own finances will get better with incomes rising.

“These historically high confidence levels should continue to support healthy consumer spending, and should be welcome news for retailers as they begin gearing up for the holiday season,” said Lynn Franco, director of economic indicators at board.”

The updated view on consumers’ expectation for rising wages refutes the recent New York Fed Survey of Consumer Expectations from July 2018. The following link and screenshot identify the findings in the New York Fed survey.

Revisiting our Fed-themed daily market dispatch, today’s Fed policy meeting will provide a lot of insight for market participants to digest. We believe markets will be focused on and react to the policy path in 2019 and any sign of changes in inflation expectations. Any change in the Fed’s view of inflation could find markets in turmoil, but we believe recent Personal Income and Expenditures data should allow the Fed to continue to view inflationary risks as balanced. And with that, buckle yourselves in for an eventful trading environment this afternoon folks!

Revisiting our Fed-themed daily market dispatch, today’s Fed policy meeting will provide a lot of insight for market participants to digest. We believe markets will be focused on and react to the policy path in 2019 and any sign of changes in inflation expectations. Any change in the Fed’s view of inflation could find markets in turmoil, but we believe recent Personal Income and Expenditures data should allow the Fed to continue to view inflationary risks as balanced. And with that, buckle yourselves in for an eventful trading environment this afternoon folks!