That was something for all the market pundits and critics to behold last week was it not? The mantra surrounding the disbelief in the market rally that started in late April has been FANG, FANG, FANG. What we actually saw during the 5-day reporting cycle for FANG, however, was a market that held up rather well despite some dramatic, individual FANG stock declines. Netflix (NFLX) and Facebook (FB) were the 2 individual names within FANG that depreciated significantly since reporting a disappointing metric or two. Shares of NFLX have fallen some 20% since reporting, but that fails to compare with FB’s record setting daily market cap plunge.

Alphabet (GOOGL) and Amazon (AMZN) managed far better share price performances with their reports that blew away analysts’ estimates on the bottom line…but the gains for each stock didn’t hold up too well. Shares of GOOGL gave up half their post reporting gains in Friday’s trading session while AMZN shares, which had been up by as much as $70 intraday, finished the day higher by only $9 per share.

Tech Too Heavy

While other tech sector names dropped mightily last week, FANG will continue to grab the bulk of investor attention. Since Thursday, the FANG stocks, Facebook, Apple, Netflix, and Alphabet, have lost nearly $166 billion in market cap. Apple is set to report results this coming week.

The tech-heavy Nasdaq fell by 1.46% on Friday only faring better than the Russell 2000, which fell nearly 1.9% on the day. The Dow Industrials and S&P 500 also fell on Friday, but by a more scant .30% and .66% respectively. When it was all said and done for the trading week, it’s hard to ignore the market’s performance.

The biggest economic data point from the past week was delivered on Friday in the way of Q2 GDP. The Commerce Department said the U.S. economy grew by 4.1 percent in the second quarter, in line with analyst expectations.

SPX Held Well, but Why?

Investors shouldn’t ignore the fallout from the tech sector that occurred last week and we’re certainly not ambivalent to the weighting of tech within the SPX. What investors should be considering, however, is the reason/s as to why the broader markets didn’t fall apart, given the weighting of the tech sector.

Since the announced buybacks from some of the largest banks, the Financials Select Sector Spiders (XLF) has largely moved higher alongside individual banks.

The chart/screenshot above represents the XLF and it’s strength since June 28th. Furthermore, it identifies certain gravity points, which are represented by $26.50 on the downside and $28.70 on the upside. So what held up the market last week while FANG and tech crumbled, the financials! That being said, the gravity points still remain and should be monitored closely this coming week.

Earnings Apex This Week

Thus far, over 50% of S&P 500 companies have reported earnings. Of those companies, 79.8% have reported better-than-expected earnings, according to data from FactSet. We are near the apex of the Q2 earnings season, with almost a thousand companies set to report results this week, including 139 S&P 500 members. With more than half of S&P 500 results already out, we will have seen results from more than 80% of the large-cap index’s total membership by the end of this week.

Many bears have been promoting the notion that Q1 marked a peak in the earnings cycle, a peak that was largely advantaged from what is also being referred to as one-off, conditional tax reform. While we certainly can’t deny the advantages in the economic and corporate earnings cycle, a peak in earnings we take umbrage. To-date, both FactSet and Thomson Reuters raised their respective forecasts. Last week’s earnings results coupled with the coming earnings results may very well find Q2 2018 S&P 500 earnings eclipsing that of Q1 2018 results.

To date, the blended Q2 earnings growth (blending the reported with the unreported) of +23.6% is below the preceding quarter’s +24.6% level. But given the momentum from the 265 S&P 500 members that have reported already, both in terms of growth as well as positive surprises, we can see Q2 earnings growth moving past the Q1 level as the remainder of this earnings season unfolds. The kicker or standout performance in the current reporting cycle, however, comes from revenue growth.

What revenue growth tells us is that while share repurchase programs are playing a large role in earnings beats, true demand for goods and services is also playing a large role in earnings results. With Q2 blended earnings presently up 23.6%, we should keep in mind that actual results typically come in better than expected, with actuals exceeding estimates in the 3% to 5% range. This means that the 22% growth pace currently expected in Q2 will likely be closer to the 2018 Q1 achievement when all is said and done.

Investors should also keep in mind that 2018 has been a tug-of-war between market fundamentals (earnings) and geopolitical headwinds, which has served to suppress the S&P 500 multiple. In short, earnings aren’t everything, especially this late in the economic and market cycle where trade tensions have been erected, rates are rising and the yield curve is feared to invert.

Fed Meeting & Economic Data

The market will carry forward long-term and long-term markets do indeed follow the trajectory of earnings, even if lagging from time-to-time. This coming week will be highlighted by earnings and some further economic data revelations. With a strong Q2 GDP print already in-hand, investors will desire to see confirmation in this Friday’s Nonfarm Payroll report.

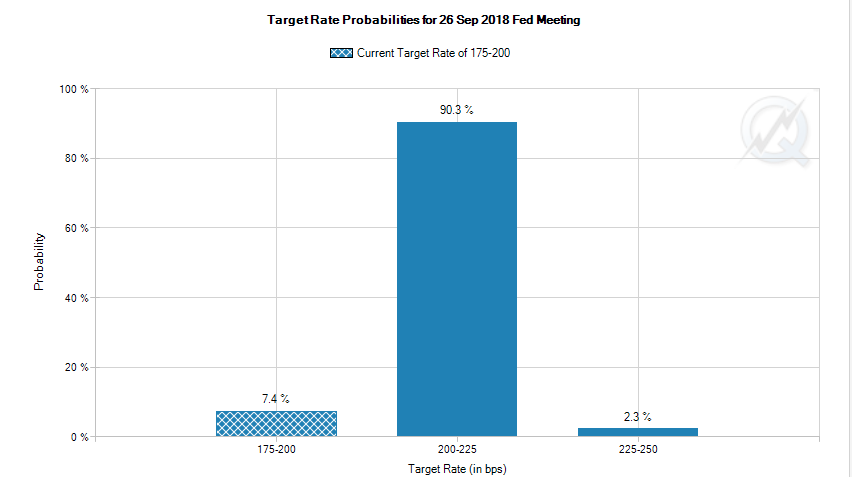

The week will kick-off with pending home sales data on Monday and is highlighted on Tuesday with the Fed’s favorite and most relied upon inflationary gauge, Personal Income and Expenditures (PCE). This is to be followed by the Fed’s rate hike decision on Wednesday. There is less than a 10% probability for a Fed rate hike in July. The Federal Reserve will issue a statement on Wednesday that likely declares strong growth in the economy and inflation moving toward its 2% target, making clear more interest rate hikes are coming. The Fed has indicated that 2 more hikes would be forthcoming in 2018.

Using the CME’s FedWatch Tool indicated in the chart above, we recognize there is a 90% chance the Fed will raise rates in September and a 62% chance, at present, that the Fed will raise rates again in December.

Thomson Reuters Revised S&P 500 Q2 Forecast

As Finom Group has been offering throughout they year, earnings estimates are likely to be found ratcheted higher in continuum from quarter-to-quarter. Below is the most recently revised Thomson Reuters Q2 forecast for the S&P 500 earnings season.

Aggregate Estimates and Revisions

- Second quarter earnings are expected to increase 22.6% from Q2 2017. Excluding the energy sector, the earnings growth estimate declines to 19.5%.

In Finom Group’s most recent weekly, research report the Thomson Reuters forecast called for 22% Q2 earnings growth YOY. Now the forecast has been revised to reflect 22.6% earnings growth YOY.