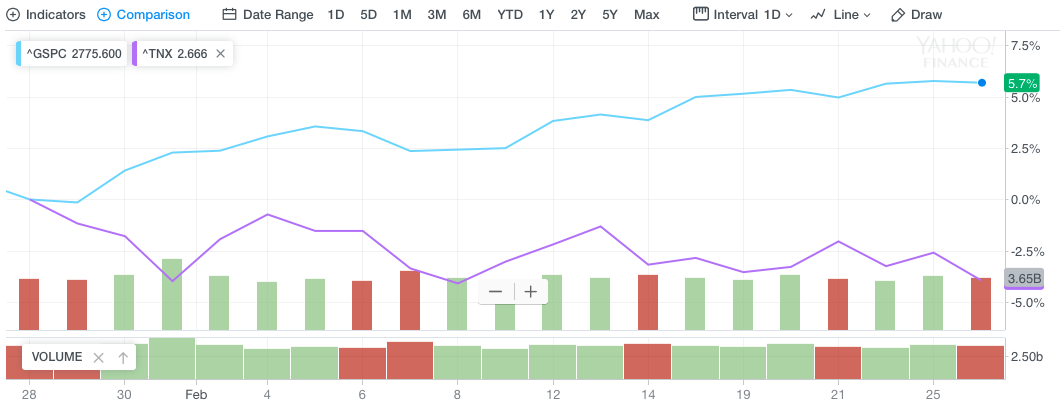

Try as it may, the S&P 500 is finding it difficult to stay above that critical 2,800 level. In Tuesday’s trading session, the benchmark index made another run above 2,800 intraday, but much like Tuesday it sold off into the closing bell.

Chairman Jerome Powell will continue with his testimony before Congress today and after a rather uneventful testimony on Tuesday. Nonetheless, Treasury yields came under pressure once again. Interestingly enough, the equity markets continued to shake off or ignore the flight to bonds.

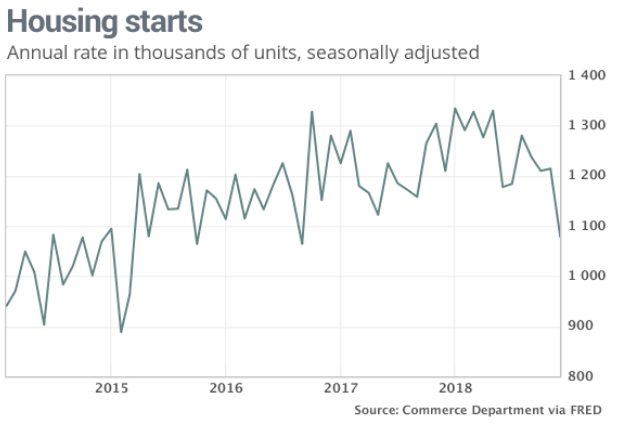

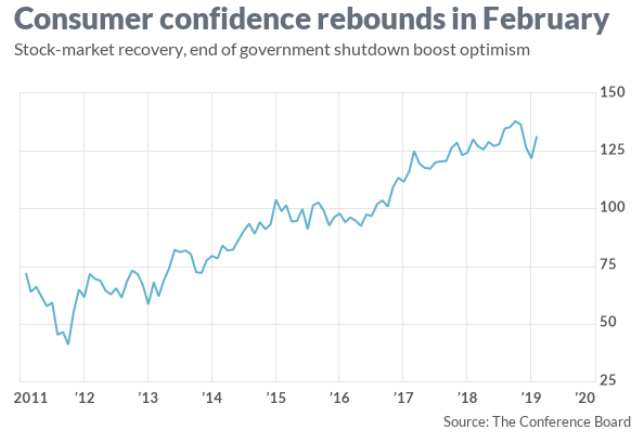

The economic data from Tuesday proved a mixed bag once again with housing data continuing to underwhelm while consumer confidence showed a stark improvement from January.

Housing starts tumbled to an annual rate of 1.08 million, down 11%, in the final month of 2018 from a revised 1.21 million in November, according to a report Even though new construction hit a lull in December, permits to build additional houses edged up 0.3% to a 1.33 million annual pace.

“Compared to housing starts, building permits are less volatile and are considered a leading economic indicator,” said Neil Dutta, head of macroeconomics at Renaissance Macroresearch.

“Permits rose for three of the last four months while starts plunged,” he noted. “Thus, we would expect construction growth to pick up in the months ahead.”

Housing starts still rose to 1.25 million last year from 1.20 million in 2017, however. The decline in 2017 was the first since 2010.

Because of delays caused by the partial government shutdown, which ran a record 35 days, the U.S. Census incorporated updates into the latest housing-start figures that normally would have occurred later on.

While the housing market conditions continue to demand improvement, Consumer confidence surged in February and rose for the first time in four months, a sign that Americans have regained optimism after the end of the government shutdown and diminished worries about recession.

The consumer confidence index climbed to 131.4 this month from a revised 121.7 in January, the Conference Board said Tuesday. The reading was well ahead of economists estimates. The consumer makes up nearly 70% of economic output/GDP.

“Looking ahead, consumers expect the economy to continue expanding,” said economist Lynn Franco of the Conference Board. The “pace of expansion is expected to moderate in 2019.”

An index that tracks expectations six months from now jumped to 103.4 from 89.4. Consumers aren’t as confident as they were last fall, however. The index had hit an 18-year high in October before suffering three straight declines that dropped it to an 18-month low.

Factory Orders, Durable Goods and Pending home sales will all be out this morning as a politically charged trading day will likely also highlight Michael Cohen’s testimony on Capital Hill. It should be quite the headline day folks. Nonetheless, Cohen’s testimony won’t change the economy or trajectory of corporate earnings. On that note and with respect to the S&P 500’s current path, here is what J.P. Morgan Chase believes the market needs to see in order to stay above the critical 2,800 level going forward.

- The ingredients for a break in the SPX above 2800 – the following macro developments need to occur to get the SPX north of 2800: 1) the Fed confirms plans to complete balance sheet normalization by the end of 2019 and commits to keeping reserves at $1.25T or more; 2) the Fed more explicitly signals the end of rate hikes (this has been strongly suggested but the recent minutes left the door open to additional tightening actions); 3) the ECB delivers on the market’s LTRO expectations; 4) Chinese growth continues to stabilize and inflects higher; 5) the US and China reach a trade compromise and Trump avoids other trade-related battles (in particular, Trump backs away from his auto threats); and 6) US growth momentum doesn’t decelerate dramatically. Bottom Line: this scenario is likely to occur but it may not be apparent for a few more weeks and thus the SPX will likely tread water for the time being.

Finom Group’s chief market strategist Seth Golden would add the following to J.P. Morgan’s well advised list:

- Crude oil remains above $55 in 2019, trends towards $65.

- U.S. Dollar comes under pressure, averages at least $93 in 2019

- Congress opts against impeachment hearings and in favor of infrastructure package

- Consumer spending remains steady and growing

The S&P 500’s breakout has been impressive and found with strong breadth and momentum. Most importantly, he S&P 500’s breakout above its 200-DMA has been sustained. The S&P has not gone back-and-forth around its 200-DMA, even with earnings expected to decline in the Q1 2019 period and bond yields falling.

Retail earnings season is in high gear this week and Tuesday’s corporate releases were met with some disappointing results. Home Depot (HD) shares fell as the company missed both and topline results, but with a one-time impairment charge muddying the results.

“Wet weather delays projects, and that is evidenced in our sales performance in the quarter,” CEO Craig Menear told analysts on the conference call.”

Here’s what Home Depot reported for the fourth quarter compared with what analysts were expecting, based on data from Refinitiv:

- Earnings per share, adjusted: $2.09 vs. $2.16 expected

- Revenue: $26.49 billion vs. $26.57 billion expected

- Same-store sales: up 3.2 percent vs. growth of 4.5 percent expected

Home Depot reported net income for the quarter ended Feb. 3 of $2.34 billion, or $2.09 per share, compared with $1.78 billion, or $1.52 a share, a year earlier. The latest results included a pretax impairment charge of roughly $247 million, or 16 cents per share, tied to Home Depot’s wholesale business, Interline Brands. Analysts were calling for earnings of $2.16 a share, according to a poll by Refinitiv.

Sales at stores open for at least 12 months were up 3.2%, missing expected growth of 4.5 percent. Home Depot said customer transactions were up 7.7% during the quarter, while the average shopper’s ticket increased 2.5 percent, and sales per square foot were up 4.9 percent.

Home Depot also announced a dividend increase of 32%, to $1.36 a share, and a new $15 billion share repurchase program.

Looking to fiscal 2019, which includes 52 weeks compared with 53 in 2018, the company said it expects to earn $10.03 per share, 23 cents short of analysts’ forecasts, according to Refinitiv data. Home Depot is calling for same-store sales to be up 5% in fiscal 2019, with revenue climbing roughly 3.3 percent. In fiscal 2018, same-store sales climbed 5.2%, and revenue was up 7.2 percent.

Macy’s (M) was able to top lowered expectations for its fourth quarter. But same-store sales came up short of expectations, as tourism spending weakened toward the end of 2018. Macy’s was forced to cut its 2018 outlook last month, after dealing with a lull in December where the number of holiday shoppers dropped off at its stores. Gross margins also remain under pressure, as Macy’s is looking for ways to better manage its inventory.

Macy’s is targeting $100 million in annual cost savings, starting in fiscal 2019, with its new restructuring plan. It said part of this plan consists of reorganizing upper management, cutting 100 vice-president level or above roles, “to increase the speed of decision making.”

Here’s what the retailer reported compared with what analysts were expecting, based on Refinitiv data:

- Earnings per share, adjusted: $2.73 vs. $2.53 expected

- Revenue: $8.46 billion vs. $8.45 billion expected

- Same-store sales: up 0.7 percent vs. growth of 0.9 percent, on an owned plus licensed basis, expected

Macy’s reported net income for the fourth quarter ended Feb. 2 of $740 million, or $2.37 a share, compared with $1.35 billion, or $4.38 per share, a year ago. Excluding one-time items, Macy’s earned $2.73 cents per share, ahead of expectations for $2.53, according to Refinitiv data. This quarter was one week shorter than the fourth quarter of 2017.

Revenue fell to $8.46 billion from $8.67 billion a year ago, but came in ahead of the $8.45 billion analysts were expecting.

Sales at stores open for at least 12 months, on an owned plus licensed basis, were up 0.7%, short of expected growth of 0.9 percent. Macy’s said online sales grew a double-digit percentage.

Most importantly, the department store retailer found gross margins falling 110 bps in the period and with elevated inventory levels going into the 1st quarter of 2019. And looking to 2019, Macy’s is calling for same-store sales, on an owned plus licensed basis, to be flat to up 1 percent. It says net sales will be about flat. Earnings are expected by the company to fall between $3.05 and $3.25 a share. Analysts were calling for earnings per share of $3.29. The sales forecast is a deceleration from 2018 and earnings are forecasted to decline. Seth Golden discussed his thoughts on Macy’s and the retail sector in an interview with TDANetwork Live on Tuesday morning.

With Macy’s and Home Depot out of the way, there are still some more retail earnings to come. Next week’s retail earning season will end with Target (TGT) reporting its Q4 2018 results. The company had previously reaffirmed it’s earnings expectations for the period, in January. Until then, we await results from the following company reports as follows:

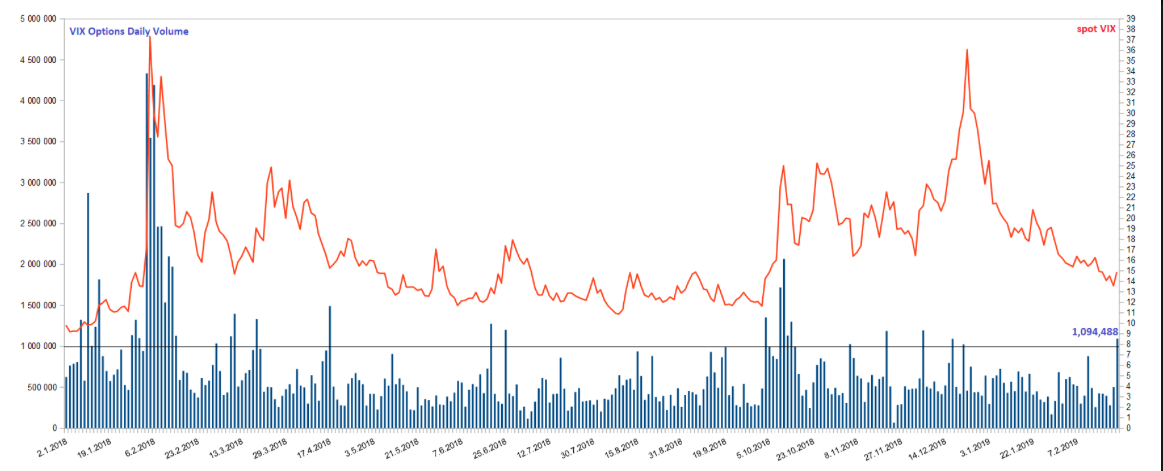

Lastly, looking forward to the opening of daily trading on Wall Street, equity futures are modestly lower once again. It’s important to denote at this stage of the market’s rebound that in each of the last 2 trading sessions, the market has actually sold off into the closing bell, a contrast to much of the 9-week equity market rally which favored equities into the closing bell. What we also saw in Tuesday’s trading session, that mirrored Monday’s trading session was VIX call buying pressure.

Tuesday’s VIX option activity was the highest since before Thanksgiving 2018. Option activity reached over 1 million contracts on Tuesday as cheap hedging opportunities persist with the S&P 500 seemingly achieving a zone of resistance.

Please review our daily, Technical Market Recap with Wayne Nelson and as he discusses what moved the markets Tuesday and what we might expect going forward. Additionally, for our Premium Subscribers, we will be formerly announcing our new-to-launch Trading Room that will be moderated by Seth Golden and Wayne Nelson, in our upcoming State of the Market video Thursday. Please click the link to review the Technical Market Recap