After 5 consecutive days of declining markets, the major averages fought back with the strongest breadth since January 4th. The Nasdaq (NDX) led the indices with a 2% rally and the S&P 500 (SPX) followed with a rally of nearly 1.5 percent. The Dow Jones Industrial Average (DJIA) lagged its peers with a .79% rally, weighed down by the biggest price weighted stock in the index, Boeing (BA). Boeing fell as much as 11% intraday as one of its flagship planes crashed over the weekend, killing all passengers onboard. Shares of Boeing rallied of their lows, however, but still finished lower on the day by just over 5 percent. Check out our daily Technical Market Recap with commentary and analysis on the broader market and individual stocks.

Coming into the trading week, Finom Group’s chief market strategist Seth Golden was of the opinion that the markets would indeed bounce off of last week’s loosing streak and follow through from last Friday’s market rebound. In Finom Group’s weekly Research Report (published Sunday), the following was offered to subscribers:

As indicated in the weekly Research Report and supported with technicals, S&P 500 was likely to bounce to at least 2,770 before finding another pause. The S&P 500 managed to outperform this forecast… and then some by nearly achieving the full, weekly expected move in the first day of the trading week.

The screenshot above depicts the .SPX weekly options chain, which details a $41/point expected move. The benchmark index narrowly missed achieving the full extent of the move on Monday and may exceed it on Tuesday, but that remains to be seen.

Equity futures took a leap in the late evening on Monday with Brexit headlines surfacing, but are lower in the 7:00 a.m. EST hour.

“Britain and the European Union emerged from last-minute talks late Monday to announce they had finally removed the biggest roadblock to their Brexit divorce deal, only hours before the U.K. Parliament was due to decide the fate of Prime Minister Theresa May’s hard-won plan to leave the EU.

On the eve of Tuesday’s vote in London, May flew to Strasbourg, France, to seek revisions, guarantees or other changes from European Commission President Jean-Claude Juncker that would persuade reluctant British legislators to back her withdrawal agreement with the EU, which they resoundingly rejected in January.

At a joint news conference, May and Juncker claimed to have succeeded.

May said new documents to be added to the deal provided “legally binding changes” to the part relating to the Irish border. The legal 585-page withdrawal agreement itself though was left intact.

Britain is due to pull out of the EU in less than three weeks, on March 29, but the government has not been able to win parliamentary approval for its agreement with the bloc on withdrawal terms and future relations. The impasse has raised fears of a chaotic “no-deal” Brexit that could mean major disruption for businesses and people in Britain and the 27 remaining EU countries.”

Brexit headlines and today’s vote in the U.K. concern U.S. investors mainly due to the weakened Eurozone economy that has been impacted by the regional, political uncertainty. With the regional uncertainty has come a reduced economic outlook for the U.K and the Eurozone as a whole. This has served to weaken the Euro and boost the U.S. Dollar (DXY). With Monday’s headlines on Brexit progress, the DXY is weakening from its recent highs, dipping below $97.

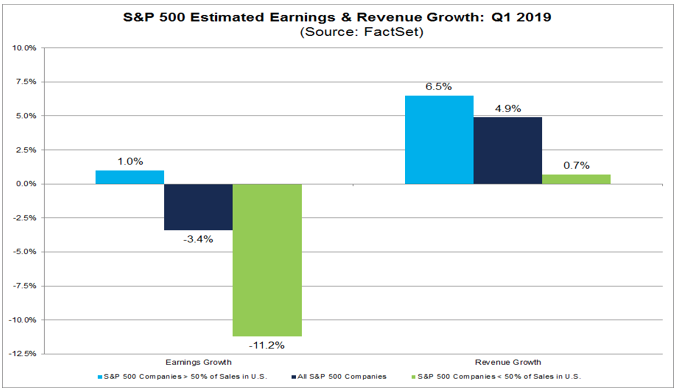

The strength of the DXY year-to-date has served to impact corporate earnings forecast, as nearly 50% of S&P 500 revenues are derived overseas. Currently, FactSet sees S&P 500 earnings declining by 3.4% in Q1 2019. Those companies with more than 50% international revenue exposure are expected to report a double-digit decline in earnings in Q1, weighing heavily on the total S&P 500 corporate earnings outlook for the period.

With Monday’s market strength, Mad Money’s Jim Cramer is of the opinion that there are more gains to come this week.

“Last week, sentiment just got too negative, and when everybody’s negative that means there’s hardly anyone left to sell. With no natural sellers, the market can roar across the board.

If I’m right that the sellers have exhausted themselves, then today won’t be the last good session we have, especially with the wave of positive analyst notes that I’m expecting this week.”

Two upgrades noted by Jim Cramer were Bank of America’s (BAC) upgrade of Apple Inc. (AAPL) from Neutral to Buy. The bank liked that Apple flipped its gross profit from negative in the first half of 2018 to positive in the second half, its loyal user base, and the potential for an acquisition. The other upgrade came from Nomura. The firm upgraded shares of Facebook (FB) on Monday. The analyst notes are as follows:

“Expect positive revisions throughout the year: Given management’s original commentary that operating margins would trend towards the mid- 30% range over “the next several years,” and considering guidance for 2019 expense growth essentially equates to 35-36% operating margins right out of the gate, we believe the expense growth outlook may be tempered as we progress throughout the year… While we’re not baking in any improvement for 2019, we assume 2020 operating margins are 100bps better than our prior model, and reach 35% in 2021…. • Regulation likely makes FB stronger: We continue to believe that increased regulation will be a net positive for large platforms like FB, though there could be some headline risk in the near-to-medium term… On the whole, we do think the negative headline headwinds have largely been exhausted, with little reaction to negative press as of late… ”

While Jim Cramer suggests more upside in the market to come this week, and he may prove accurate with his sentiment, investors should be aware that this week represents a triple witching week. In addition to being a triple witching week, with certain contracts that are a year-old expiring come Friday, investors should also recognize an issue underlying the market’s YTD-rally and even the rally that took place on Monday.

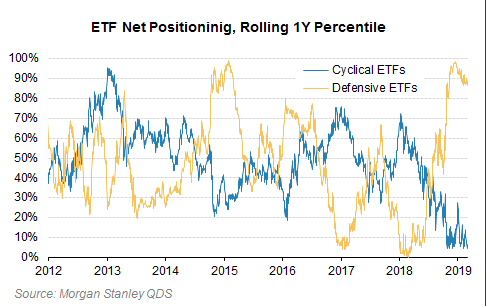

Described in the chart above is the relative defensive positioning amongst investors. Cyclical stocks are being passed over in favor of defensive sectors and/or defensive ETFs. One such defensive sector ETF is the Utilities Select Sector SPDR Fund (XLU).

While the Utilities sector ETF is up 9.5% YTD, it is up nearly 18% over the last 12 months and as the S&P 500 has underperformed. Investors have yet to relinquish their fears of the late inning expansion and bull market cycle. We can see this fear in the inverse relationship that developed between the XLU and the S&P 500 since 2018 in the following chart:

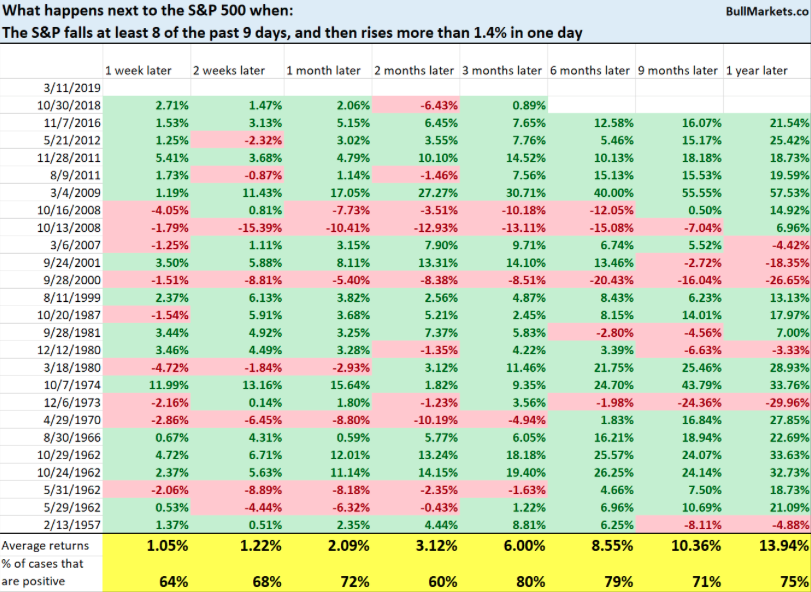

Monday’s strong market rally came with very strong breadth. Within that strength, one would have expected defensive sectors to underperform, but that isn’t exactly what we witnessed. While the XLU only rose .7% on the day, another defensive sector, Consumer Staples (XLP), rose almost inline with the S&P 500. Stocks like Coca-Cola (KO) rose nearly 3% on Monday and PepsiCo (PEP) rallied nearly 1.2% on the day. Investors are still seeking dividends and safety stocks as the market has rallied for the better part of 2019. And with Monday’s rally, the S&P 500 has fallen 8 out of the previous 9 days, before spiking.

What happens next for the S&P 500 given all the aforementioned market characteristics, but mainly the last 10 days’ performance? Let’s review a recent market study provided by bullmarkets.co to find out.

As depicted in the table above, the market tends to gravitate higher 12 months later and with a greater probability of moving higher some 3 months later.

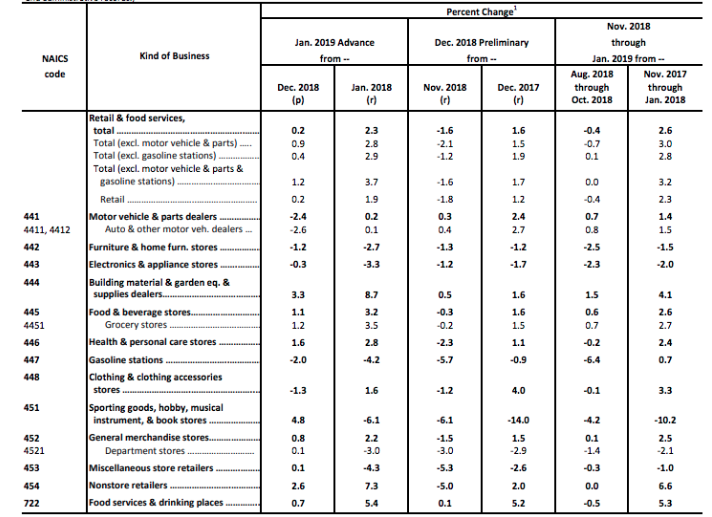

The biggest economic data point of the day on Monday came from the retail realm. The Census Bureau reported a bounce back in consumer spending for January, but a larger decline in retail sales for the month of December than originally reported.

Retail sales rose 0.2% in January, led by home centers and Internet stores, according to a government report delayed by the partial federal shutdown earlier this year. Economists polled by Reuters had forecast a decline of 0.1% for the period. Sales had tumbled a revised 1.6% in December, the largest drop since late 2009, just as the U.S. was exiting the 2007-09 recession. The government originally had reported a 1.2% decline.

If auto and gasoline are omitted, retail sales in January rose a much healthier 1.2% in January. Auto dealers saw a 2.4% drop in sales, mainly because of steeper discounts and fewer sales to other businesses such as rental companies. Gas stations reported a 2% decline as the cost of oil fell, which actually serves to the benefit of households and/or consumers.

Both the revisions to December’s retail sales figures and January’s retail sales update still lack consistency with typical reporting cycles. The even bigger drop in sales in December is still viewed with suspicion by many economists in light of other retail-industry reports such as Redbook that suggest sales were much better than the government reported. MasterCard spending data completely defies the government’s reporting from the holiday period, especially when it comes to online/Nonstore sales growth.

According to MasterCard SpendingPulseTM, which provides insights into overall retail spending trends across all payment types, including cash and check, holiday sales increased 5.1% to more than $850 billion this year – the strongest growth in the last six years. Online shopping also saw large gains of 19.1% compared to 2017.

Regardless of government reporting, investors seem to realize there are some anomalies in the reported data and have thus shrugged off the report in favor of the underlying growth reported by retailers throughout the recent reporting cycle. Most major chain store retail brands were able to beat consensus estimates and guided well for 2019. Target (TGT) and Wal-Mart (WMT) both showed some of their best same-store-sales growth numbers in years and offered guidance within or above analysts’ estimates for 2019. Additionally, both retailers reported Q4 2018 online sales growth of 34% or better for the period.

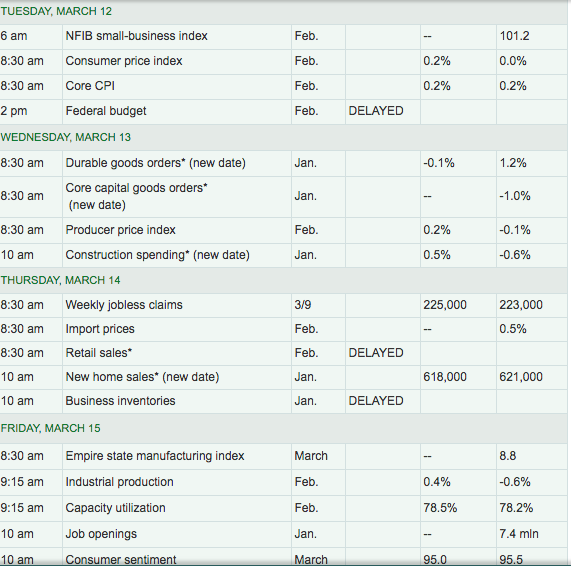

There is still a great deal of economic data to be reported during the trading week as noted in the table below from MarketWatch.

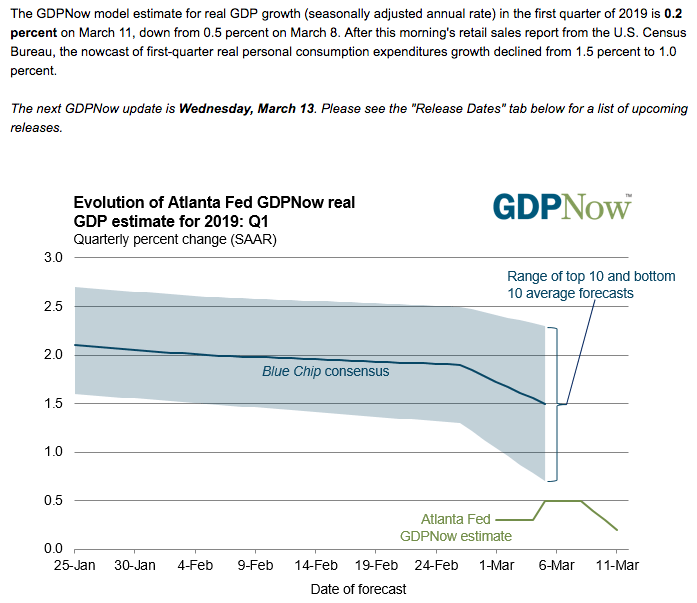

With Monday’s retail sales data, the Atlanta Fed revised lower its Q1 2019 GDP estimate. Prior to the retail sales data, the growth estimate was .5% in the Q1 period. The next revision will come Wednesday, after Durable Goods orders and construction spending data is released.

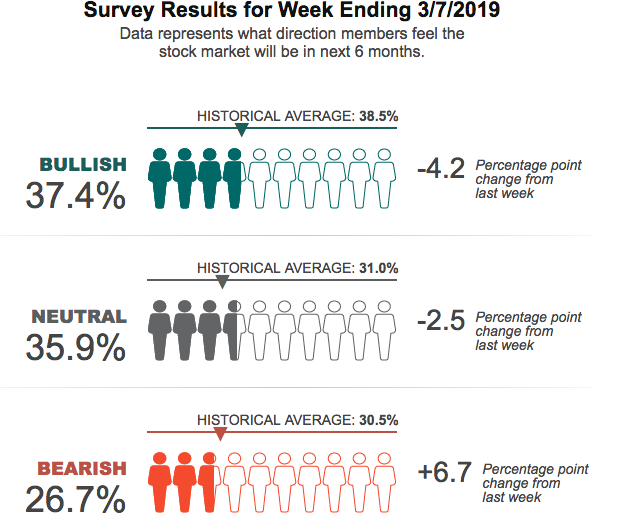

Ahead of Wall Street’s opening bell it seems as though market sentiment has rebounded from the prior week’s selling pressure.

Bullish sentiment dipped last week once again, below the historical average. But even with the surge in the major averages Monday, one analyst encourages investors to “get off the bull”. Michael Wilson, Morgan Stanley’s top U.S. equities strategist, believes investors might be buying into the Goldilocks narrative: Economy’s not too hot, and it’s not too cold. Hello new highs for stocks and tighter spreads for credit.

“What if growth isn’t ‘just right’ and Goldilocks is the wrong fairy tale? I see other reasons for the growth slowdown that have been underappreciated by most market analysts.”

Wilson reiterated in his Monday notes that buybacks and tax cuts were a one-time boost for equities and lose their luster after the first year. Additionally, higher operating costs are beginning to take their bite of corporate profits.

“Specifically, consensus EBIT margin expectations for 2019 have fallen by 70bp since October, which is the biggest decline since the last earnings recession in 2015. While it’s difficult to measure the contribution from each source of incremental cost, we are confident it’s not all due to supply chain disruption from US tariffs on Chinese goods. Instead, our contention continues to be that the majority of the cost pressure is the result of the economy running too hot last year which has led to higher labor costs among other things (see Exhibit). This essentially tipped over the profits cycle. Furthermore, the de-escalation of trade tensions with China and a pausing Fed will not alleviate those pressures, in our view. It’s also very different than in early 2016 when goldilocks was alive and well.”

While the corporate executives do seem to fall inline with Wilson’s analysis, the labor market is stronger than it has been in even the recent past and the period specified by Wilson. Nonetheless, the headwinds for corporate profits are now more realized than they may have been coming into 2019, but to Wilson’s point, they seem to be ignored by investors given the sharp rebound in the market. The rebound may be met with disappointment if indeed profits don’t rebound post the Q1 2019 reporting period and as such Wilson suggests caution amongst investors.

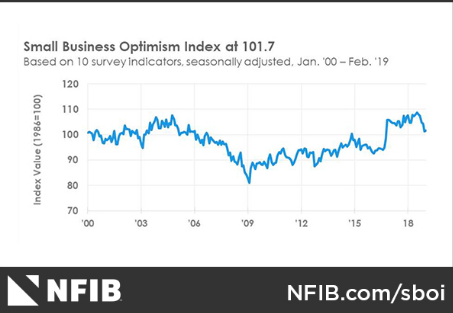

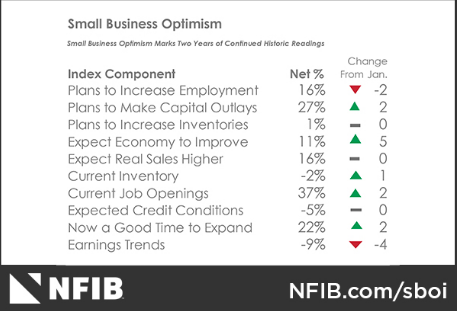

As it pertains to profit expectations, labor and employment and small business sentiment, the latest report from the National Federation of Independent Business is out.

The NFIB Small Business Optimism Index improved modestly in February, increasing 0.5 points to 101.7. Views about future business conditions and the current period as a good time to expand improved as did plans to make capital outlays. Earnings trends weakened, as a million laid off workers and others affected by the shutdown cut back on spending.

“Small business owners are thankful to have the government shutdown in the rear view mirror but need more certainty about the future,” said NFIB President and CEO Juanita D. Duggan. “Small businesses put their money where their expectations are as we’ve seen when they get tax and regulatory relief. The best thing Washington can do for the small business half of the economy is to continue the policies – tax cuts and deregulation – that leave them with more resources to invest and find qualified workers.”

And with that, the trading day is set up for another eventful day! Be sure to subscribe today in order to access our weekly Research Report and trade alert services that include a live daily Trading Room!