Heading into the weekend the markets have awakened in the early Friday hours and ahead of the opening bell on Wall Street. Asian Markets traded sharply higher overnight and the activity has carried forward into the European markets. After 4 straight sessions whereby the U.S. major indices trading lower and near their lows into the closing bell, equity futures are up more than .5% across the board in the 6:00 a.m. EST hours. Please review our daily Technical Market Recap by clicking the link.

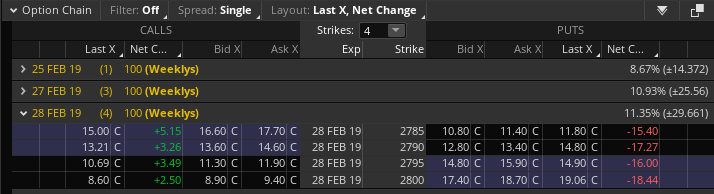

This being Friday, we’re forced to review the S&P 500 weekly expected move. Options pricing has been pretty efficient of late and found with premium sellers more abundant than during the Q4 2018 market downturn.

As shown in the screenshot above, the weekly expected move is $29/points. The S&P 500 came into the trading week at 2,788 and over the last 4 trading days has compiled just a $4/point move week-to-date. It remains to be seen how those options expire today, in the money or otherwise, but if the recent “sell the close” trend persists we’d be of the opinion the early market hour rally may fade in the late afternoon.

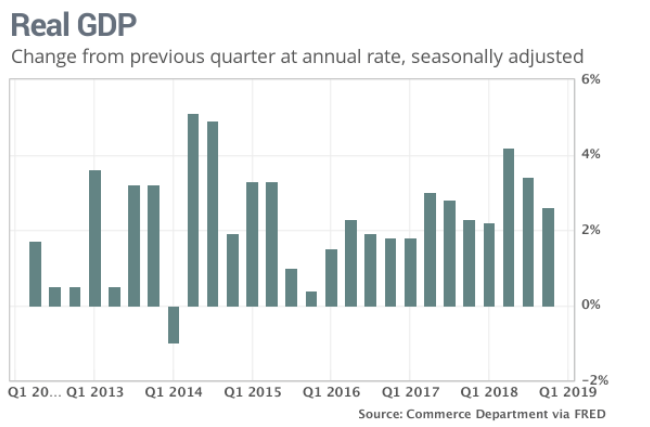

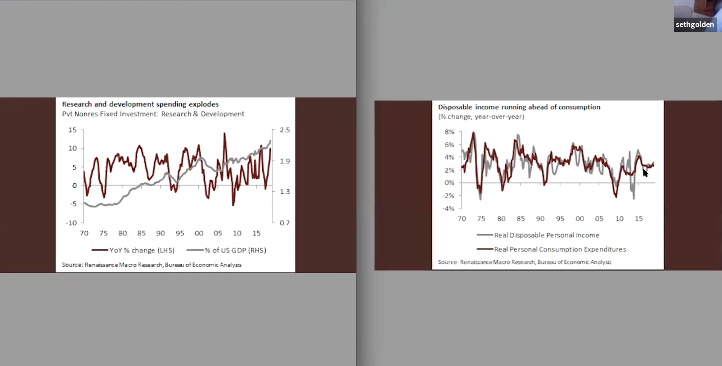

The economic data released Thursday proved puzzling to the permabears given all the rhetoric of a sharp deceleration in the economy occurring during the Q4 2018 period. But Q4 GDP proved the deceleration was a touch over exaggerated, coming in at 2.6% growth versus estimates of roughly 2% growth.

Consumer spending, the main engine of the economy, increased a healthy 2.8% in the fourth quarter. Americans spent more on new cars and trucks, health care and financial help, among other things. Households didn’t spend as much as they did in the previous two quarters, but it was more than enough to keep the economy on a steady keel.

Keeping today’s Daily Market Dispatch rather short, but sweet, we invite our readers to review our State of the Markets video. Please click the link to review the video, which is 66 minutes in duration.

Video Outline:

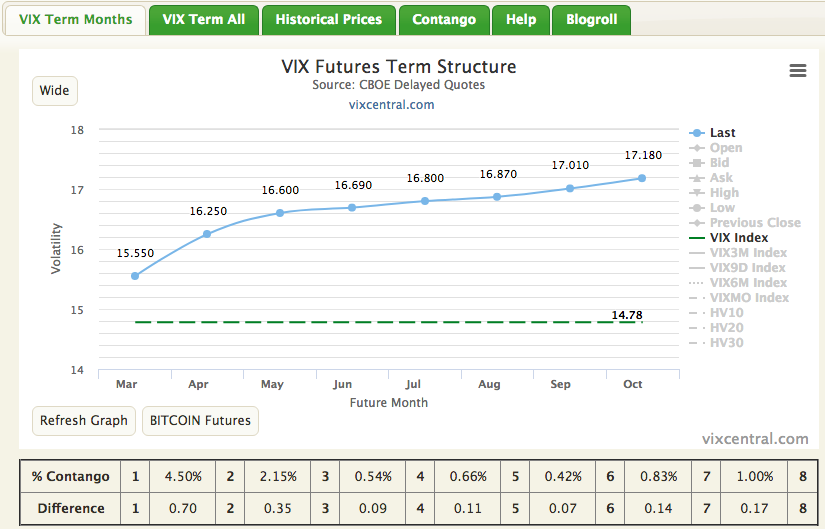

- Introduction to VIX Futures Term Structure. Discussion on the calendar cycle for m1 (March VIX Futures) which is 33 days and will achieve its halfway point in the cycle come next week. Importance of knowing what stage of the calendar cycle Futures are in. Review of Proshares UVXY holdings as example of how the cycle progresses from m1 to m2 (April VIX Futures). When to focus on m2 contango as opposed to m1 contango. (0-11 minutes in)

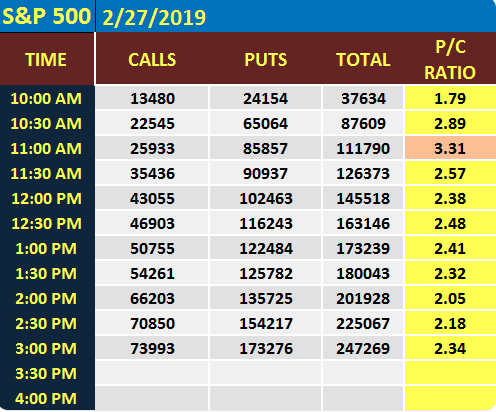

- Lack of volume in the market resurgence since New Year. Heavy SPX put buying this week as SPX went above 2,800. Mostly programmed hedging activity. Most VIX options traded since Thanksgiving last year occurred this week. (11-20 minutes in)

- Earnings season is coming to an end. Best Buy, Macy’s, J.C. Penny, Wal-Mart, Target; discussion on retail sector as a whole. Who with thrive, fold, survive? Why Amazon got the Whole Foods acquisition wrong and discussion on DSD delivery. Macy’s or J.C. Penney buyout potential is extremely limited due to trending results and carried debt. (21-35 minutes in)

- Fund flows continue to prove negative YTD for equities and positive for bonds. Weekly expected move is $29/points and we’ve only accomplished a week that expresses a $4 move week-to-date. EOM for fund managers to window dress and/or rebalance. (35-41 minutes in)

- Discussing Starbucks (SBUX) from a technical perspective. Finom Group has no position in SBUX since selling shares in 2018, but offered the investment to subscribers in 2018 and it netted a 11.5% return. SBUX is simply moving with the market presently, but outperformed during the Q4 2018 market downtrend. Boeing (BA) discussion and a dive into how big funds are targeting shares in order to arbitrage the market given it’s the most heavily weighted stock in the DOW and it can trigger other programs within the other major indices to follow its uptrend. Introduction of Finom Group’s Trading Room, will go live on Monday next week. (41-56 minutes in)

- Brief discussion on GDP, which beat expectations. Wages have risen and so has disposable income. But consumption is lagging disposable income, which insinuates theres room for consumption to pick up. Comparing 2018 GDP with 2007 GDP. Unemployment rate is lower today at 4% than in 2007 at 5 percent. Don’t take any one piece of economic data to draw conclusions on the economy. (57-104 minutes in)

- Discussion on the markets and how fund managers exercise distribution and accumulation cycles. Conclusion of State of the Markets.