Over the weekend, Finom Group’s weekly research report focused some attention on the strength of corporate buybacks. In the report titled “Markets Look Poised For Gains, but Mid-Term Turbulence Looms Large”, we discussed how outsized corporate buybacks are during the month of August and as displayed in the following chart.

Corporate buybacks are set to hit record highs in 2018 with new forecasts worth upwards of $1trn in corporate buybacks to be announced. The corporate buyback outlook has set a floor under the market. It’s been said that where the Fed is tightening and offloading it’s balance sheet, subsequently draining liquidity from the market, corporate buybacks are a liquidity bridge providing support during this central bank activity. In more simplistic terms and to the point, the quantity of corporate buybacks is/has been bullish for equity markets.

With regards to corporate buybacks and their relative execution in the market, earnings season marks a blackout period for such activities that are regulated by the Securities and Exchange Commission. Under SEC rules, companies are required to pause stock buybacks approximately 5 weeks (1 month) before they release their earnings reports. For most U.S. companies, now, they are exiting this blackout period and are allowed to activate their corporate buybacks, which falls in line with why August tends to produce the largest quantities of share repurchases.

Finom Group has maintained its bullish outlook on both the economy and the market for the totality of 2018. We’ve focused on economic activity, consumption, reflation and all the while market pundits have stomped their feet and banged the proverbial drum. What the bear market promoters may have overlooked are the principles of supply and demand; corporate buybacks play a critical role in the supply-demand equation.

Finom Group has maintained its bullish outlook on both the economy and the market for the totality of 2018. We’ve focused on economic activity, consumption, reflation and all the while market pundits have stomped their feet and banged the proverbial drum. What the bear market promoters may have overlooked are the principles of supply and demand; corporate buybacks play a critical role in the supply-demand equation.

“Namely, U.S. companies appear poised to eclipse the $1 trillion mark in share buybacks this year, a pivotal record that will keep the stock market going even as many retail investors are beginning to fear equities, according to a Goldman Sachs analysis for clients.

“Corporate repurchases remain the largest source of demand for shares,” wrote David Kostin, chief U.S. equity strategist at Goldman.

Kostin also noted that the year already has seen a wealth of buyback announcements, with companies authorizing $754 billion worth. History shows that there’s typically an 85 percent follow-through rate, so that would add up to $640.9 billion worth with 20 percent of S&P 500 companies yet to report second-quarter earnings.”

Although Goldman suggests a boost in the markets from corporate buybacks, it doesn’t expect a lot of upside for markets. The firm maintains its S&P 500 price target at just 2,850 for the full year, a level hit just yesterday. The price target is maintained even though the firm offers that “fundamentals remain extremely positive” as GDP is growing at a healthy pace, unemployment remains low and consumer confidence is strong.”

One of the main reasons why David Kostin doesn’t believe there is much upside to the market despite all the noted bullish aspects is the swelling U.S. budget deficit. Kostin states that the deficit presents an obstacle for investors, especially if it causes government bond yields and interest rates to rise, putting pressure on market valuation. So the question is whether or not history supports Goldman’s limits on the market’s performance. We’ll get to that in a moment!

Morgan Stanley has been one of the largest bear voices in a crowd of bullish financial firms for the majority of the year. Even as their chief U.S. equity strategist, Michael Wilson, lays claim to a potential large pullback in the market near term the firm has raised their outlook on the economy for 2018. Here are Wilson’s notes to investors last week.

“I’m a bit leery about the fact that small caps have become a perceived safe haven in the event of trade conflicts,” and that this “perception may now be overpriced.

Just remember that those last innings can bring a lot of excitement and anguish, too, depending on which team you are rooting for.

Within the U.S. market, we have noticed a significant divergence between the perceived weakest links and the stronger ones. From a sector standpoint, it’s really down to just technology and consumer discretionary [maintaining strength].

Our call was that these groups are likely to get hit next and, indeed, we think a meaningful correction in these asset categories began late last month. The bad news is that these sectors make up almost 40% of the S&P 500 and close to half of the Nasdaq Composite Index, so the correction will leave a mark on the broader U.S. indexes if we’re right.”

Again, this is all information that Finom Group discussed over the weekend with our subscribers, but becomes more pertinent given Morgan Stanley’s revised GDP outlook for 2018. Morgan Stanley popped its GDP forecast for 2018 from 2.5% to 3 percent. The firm actually lowered its 2019 estimate a notch, from 2.1 percent to 2 percent on belief that the effects from tax cuts and higher spending caps on the fiscal side will begin to wear thin in the coming year. And here are some of the reasons Morgan Stanley’s economist Ellen Zentner offered for raising the firm’s forecast:

- The 2Q18 GDP report and comprehensive annual benchmark revisions painted a much more favorable backdrop for domestic economic activity than we expected, with upside in almost every core demand component of GDP

- A big boost to the savings rate, from 3 percent to 7 percent, stood out most as a factor reflecting pent-up demand and more room to grow ahead

- The bank changed its forecast that the central bank indeed would do only one more hike this year and now believes two more are in store

When good bears go bad, right? The bottom line is that Morgan Stanley is bumping its GDP forecast, but according to its chief equity strategist, this will not lend itself to more favorable equity valuations. One would have to believe future corporate earnings growth is already baked into the market for not just the market to stall out here and now, but decline going forward. Doesn’t seem to jive with the history of markets, but we’ll have to see what the future comes to be. Moreover, keep in mind that for the remainder of 2018, S&P 500 earnings are expected to grow in the 20% range on a YOY basis. Now let’s look at the rationale behind Goldman Sachs’ raised GDP outlook.

“Friday’s 157k jobs headline significantly understates the strength of the July employment report,” Jan Hatzius, chief economist at Goldman Sachs, said in a note. “The composition of job growth was strong, with sturdy gains in cyclical sectors such as manufacturing and temporary help services offset by weaker numbers in less cyclical ones such as education/health and local government.”

Goldman is holding firm on its expectation for the third quarter in 2018 to see a 3.3% GDP gain, but raised its fourth-quarter outlook to 2.5 percent. Based on the respective first- and second-quarter numbers, that would take the full-year average to 3.15 percent. The firm also raised its 2019 estimate to 2% from 1.75 percent.

So both Goldman Sachs and Morgan Stanley are raising their GDP forecast, which is directly tied to consumption activities that produce corporate earnings, but they don’t expect much or any market appreciation. It’s an interesting dichotomy for sure!

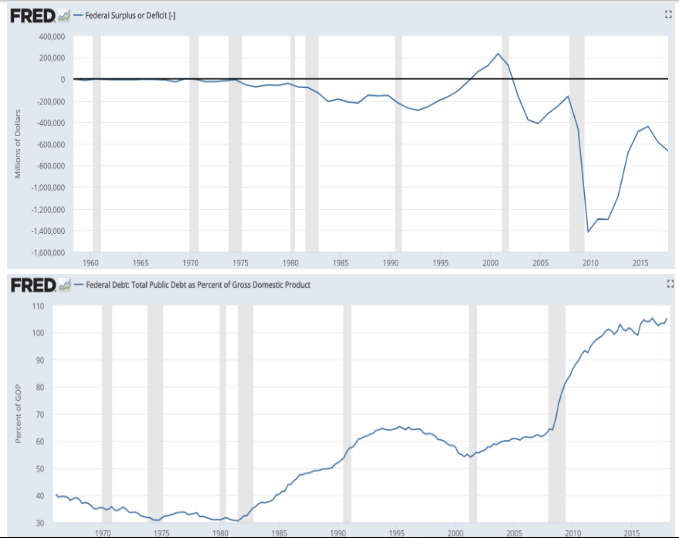

Recall earlier in this article that Goldman’s chief U.S. equity strategist had highlighted the growing U.S. deficit s negatively impacting his outlook on the S&P 500 for the year. One of the loudest bear cries against the market continues to be the growing national deficit and “exploding” debt levels. Keep in mind this particular bear mantra has been around and promoted since the 1980s. With this in mind, let’s take a look at the history of the national deficit juxtaposed with the market.

Based on the federal governments own historical data and while both deficits and debt has grown over the many decades, markets have done one very obvious thing… appreciate in value! As such, what we come to recognize from David Kostin’s rational for a stalling market going forward is that the strategist is attempting to time market performance for stated reasons that are not historically supported. We’re not saying Kostin’s outlook won’t come to fruition, we’re simply providing the historical context that begs of some alternative interference in the market to satisfy the outlook. Kostin can be proven right, for all the wrong reasons!

Again, and as we always try to bottom-line the economic and market narrative for subscribers, the market follows earnings and if earnings go higher over time, the market will follow. As such, we also urge investors to recognize that other bear cries will surface as the market trends higher, be it now or later in the year. One of the more recent bear cries suggests that the S&P is more overvalued today than during the dot –com bubble. “Survey says…wrongggggg! What these folks are referring to is not price-to-earnings, but rather price-to-sales. Investors value the market to earnings, not revenues/sales. It’s a cute little trick proposed by the bears, but a trick only wagered against those with lesser market experience and understandings.

What’s also relevant in the price-to-sales understanding for the current economic and market climate is the fact that sales are growing faster than earnings, but eventually level out over time. Most importantly, however, most importantly is that those sales are producing greater profits.

With respect to the dot-com era and PE multiples, the chart above tells us all we need to know when it comes to the concerns about valuation. We’re not saying that the current market is not expensive. In fact we admit that it is expensive according to both the 5 and 10-year average. The forward 12-month P/E ratio for the S&P 500 is 16.5. This P/E ratio is above the 5-year average (16.2) and above the 10-year average (14.4). Even with the market presently above it’s historic average, earnings growth is projected to climb to levels not seen since 2011. Trying to pin investors into a gloom and doom corner over false narratives surrounding the national deficit, corporate and household debt and valuations seems a poorly constructed game plan by the bears. Investors, bulls and bears alike, need to do their homework to support or refute their long-term outlook and position investments appropriately.