It’s not often that you’re able to witness a brutal interview of an analyst who was formerly glorified in the financial media for his/her former calls which were accurate… kind of. Morgan Stanley’s Mike Wilson coined and predicted a rolling bear market for 2018, established with an S&P 500 price target of 2,750. After topping out at 2,940 in September 2018, the market dropped precipitously in the Q4 2018 period. When we actually parse out the reasons the stock market fell roughly 20% in the Q4 period and to its trough on Christmas Eve, we come to realize two considerable factor that played roles in proving out Mike Wilson’s calls, luck and fear. That’s right folks, luck and fear.

Sometimes, yes, it’s better to be lucky than good. Unfortunately, luck can only take you so far and that luck does eventually run out. Hence, we’re discussing Mike Wilson’s former calls juxtaposed with his seemingly misguided market outlook in 2019 that points the spotlight on him once again, but for unfavorable reasons.

After a market route in Q4 2018, whereby the S&P 500 fell into the 2,300 range, one would think the Morgan Stanley analyst would have adjusted his market outlook and analytics to capture the Fed’s pivot, Chinese economic stimulus and the general resetting of earnings expectations. But that didn’t happen. Wilson stuck to his guns, urging on several occasions for market participants to “Get off the bull”, as the market rally persisted in late January 2019.

“Employing a rodeo metaphor, Wilson on Monday urged his clients to “dismount” as the market’s rally since late 2018 is starting to look precarious.

“Maybe the bull ride since Dec. 24 has not gone a full ‘8 seconds’ but we’d look to dismount anyway—we’re close enough and bulls can be dangerous animals,” he said in a report, referring to the number of seconds a bull rider is required to stay on to earn a score for a ride.

“We struggle to see the upside in hanging on just to see how long we can. We think it is better to hop off now and rest up for the next rodeo.”

It was only a couple of weeks later in February that Wilson doubled down on his warnings, sending out notes to clients urging them to accept that an earnings recession was at-hand.

“Mike Wilson, chief equity strategist at Morgan Stanley, on Monday downgraded S&P 500’s earnings-per-share growth target for the year to 1% from 4.3% and warned of a looming earnings recession.

Our earnings recession call is playing out even faster than we expected,” said Wilson in a report. “When we made our call for a greater than 50% chance of an earnings recession this year, we thought it might take a bit longer for the evidence to build.”

“We have seen this kind of inflection happen a few times, but these inflections were all related to 1) comping against negative or slower EPS growth or 2) tax cuts mechanically lifting the growth rate. Neither of those forces is at play this year. In fact, it’s the opposite making the achievability of these estimates even more unlikely,” he said.

The strategist actually took it further and suggested that investors should brace for more downward revisions, higher volatility and increased pressure on returns.

“If current estimates move in line with history, we could see a full year decline of about 3.5% in S&P earnings,” said Wilson.

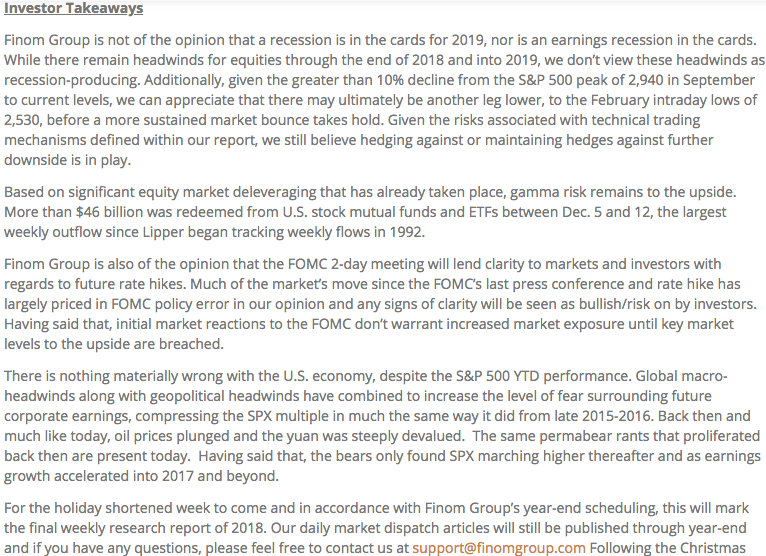

It’s at this time that we’d like to step in and highlight what Finom Group was offering to it’s subscribers during the depths of the market swoon in December 2018, as Wilson was pounding the “sell” button.

From the graphic depicted above, which headlined our weekly Research Report titled The SPX/VIX Divergence Signals & The Rising Tide of Algos Weigh on Markets, Finom Group was forecasting a near-term bottom for the markets and a subsequent rebound. The following notes to our subscribers suggested hedging during the market’s downturn leading to a subsequent rebound in the markets. ( fromDec. 16, 2018)

And why were we so confident that the market would rebound… earnings and the rationale for the market sell-off wasn’t altogether logical and/or warranted. As noted above, Wilson’s calls demanded a good deal of luck and fear. While Wilson offered an earnings decline post the tax stimulus surge in corporate profits through 2018, the extent of the earnings decline is presently being proven to have been over stated. We’ll take a look at why this is in just a minute or two, but what we really need to rationalize for investors is the components of fear and luck that drove Wilson’s provocative, yet accurate 2018 calls.

Can you point to an analyst, an economist or any market participant that forecasted the Fed’s autopilot rate hike commentary when the FOMC raised rates in late September 2018? Who was that person, I’d like to meet them and shine a spotlight on that person because WOOOOOO; now that was an amazing call/prediction! The fact is that nobody forecasted such commentary surrounding the future path of rate hikes to come out of the Fed Chair’s mouth. And that was just the first unforeseeable characterization of future Fed activity offered up to the public by Fed Chair Jerome Powell in 2018. It was that commentary that spooked investors and found the first bout of volatility in the market since earlier in the year. Once September rolled into October, the market entered the volatility box and didn’t look back.

Certainly as the global equity markets began faltering, by December the situation became bleaker with algorithmic trading and seasonal hedge fund redemptions drawing liquidity out of the market. Even with the FOMC walking back the notion of auto-pilot rate hikes in 2019, there was one more misstep in messaging put forth by the Fed, with yet another rate hike that seemed unwarranted, unnecessary and without justification given the PCE had been declining for nearly 4 months leading up to the December rate hike.

The Fed once again hiked rates by .25 bps in December, but also suggested that no further rate hikes were necessary in the present economic climate. Unfortunately, accompanying this last rate hike was the question of the Fed’s Quantitative Tightening program, the sales of balance sheet assets that had also been in affect throughout 2018. Once again, the Fed signaled to markets that QT activity, which is another form of tightening, was being comfortably executed and expected to continue going forward. The commentary surrounding QT was almost identical to the former autopilot rate hike commentary and thus the markets took yet another leg lower.

The current Powell led Fed’s messaging to markets has been characterized as some of the worst messaging in decades, failing to guide market participants toward reasonable expected activity from the Fed, stimulating volatility in the equity markets. Nobody, including Mike Wilson forecasted such extremely poor messaging from the most powerful and important central bank in the world. This my friends, this proved most fortunate for Wilson’s bearish calls on the market; this was pure luck! And from all of that poor messaging also brought about with it a great deal of fear, which ultimately proved irrational and with the S&P 500 rationalized for ACTUAL corporate earnings.

We invite investors to always keep in mind what drives the market over time, earnings! Earnings are the key driver of equity prices over time and while the rate of change in growth can ebb and flow with time, the economy and earnings have always proven to grow with time. You don’t like what’s proving to grow the economy and earnings, suck it up; brush it off! What you like and what the market is designated to react to are not to be joined at the hip. Don’t like that debt laden economic growth has proven to drive the current economic expansion cycle; we get it, but to spite one’s portfolio because we don’t like what’s driving corporate profits is only self-destructive.

For all of Mike Wilson’s earnings mourning and recessionary calls, this isn’t being forecasted for FY19 presently. Moreover, we’ve likely seen a trough in downside EPS forecasts, as we are now seeing Q1 2019 EPS forecasting curling higher, but still negative.

According to FactSet, Q1 EPS is expected to decline by -3.9%, up from a decline of -4.3 in the previous week. Is that enough to suggest Mike Wilson’s forecast for FY19 to elicit a -1 to +1 EPS is out of bounds? We’d suggest it isn’t, but the quarter isn’t yet completed and earnings season is at its height this week with 150 S&P 500 companies reporting results. What we really need to look at are the companies that have reported already, their beat rate and model that against the remainder of the quarterly earnings season. So after doing that…

Over the past 5 years on average, actual earnings reported by S&P 500 companies have exceeded estimated earnings by 4.8 percent. During this same period, 72% of companies in the S&P 500 have reported actual EPS above the mean EPS estimate on average. As a result, from the end of the quarter through the end of the earnings season, the earnings growth rate has typically increased by 3.7% on due to the number and magnitude of upside earnings surprises.

So if we take the aforementioned and apply it to the current earnings cycle the actual earnings decline for the quarter would be -0.6% (-4.3% + 3.7% = -0.6%). But wait…!

Recall how quickly, persistently and decisively earnings estimates continued to decline throughout the 1st quarter of 2019. When you dredge that deeply with forecasts, you’re bound to overshoot to the downside right? With that offered, it is interesting to note that the S&P 500 is currently outperforming the 5-year averages in terms of actual earnings relative to estimated earnings. As of Monday, 78% of S&P 500 companies are reporting actual EPS above estimated EPS, above the 5-year average of 72 percent. S&P 500 companies are beating EPS estimates by 5.7%, which is also above the 5-year average of 4.8% noted previously. And these before the titans of tech begin reporting. The titans of tech usually have outsized beats as they stretch sales internationally, which can be difficult to analyze and project. Having said all of that with respect to the current earnings cycle, if the trend of beats continues at the current rate only, the earnings growth rate should increase by more than the 3.7% average. So what does that mean or what can we conclude from this exercise? The math is all there folks; it means we could see earnings result for Q1 2019 be found with growth on a YOY basis. And that’s why Mike Wilson’s forecasts may be proven wrong and why his previous 2018 calls and forecast were found with more luck and fear than logic and expertise.

Nonetheless, we have to appreciate the Mike Wilson’s of the world in the same token we appreciate the Marko Kolanovic (J.P. Morgan Chase analyst) of the world. Being a market strategist and/or an analyst is a very difficult job, often a thankless job at that. When you’re right, you’re the Golden Goose and when you’re wrong… well you’re asked to come on CNBC and stand before the “Judge”!

On CNBC’s Halftime Show Tuesday, Mike Wilson offered his errand call that did not anticipate the market’s rebound in 2019. But Wilson isn’t changing his S&P 500 target for 2019. His base case year-end price target for the S&P 500 is 2,750, while his bull case is 3,000 and his bear case is 2,400. Deutsche Bank has a base-case 3,250 price target and Credit Suisse has a price target of 3,025.

“We’re going to go to new highs. We’re there already. We’re going to probably go to 3,000 at some point in the next couple weeks just because they want to touch it,” Wilson, the firm’s chief U.S. equity strategist, told CNBC on Tuesday.

When asked about his prediction of an earnings recession in light of stronger-than-expected first-quarter earnings, Wilson said, “We stand by that call.”

“I’m not going to deviate from my models and things that have helped us throughout the last 30 years to say, ‘the market is breaking out so I have the change my fundamental view,’” he said.

Finom Group isn’t of the opinion an earnings recession will present itself for 2019 and has offered it’s S&P 500 price target within weekly Research Reports. We anticipate the price target to be achieved now in Q2 2019. But with regards to Mike Wilson’s CNBC appearance, there was something so disingenuous offered in the Q& A session, something rather appalling in our opinion.

Mike Wilson stated, “We have been overweight equities”. One more time and please review the video recording where he states this quite clearly, “We have been overweight equities”. Based on Wilson’s calls, warnings and invitations to dismount the bull all year long, we can’t help but to rationalize Wilson stating, “we’ve been overweight equities”, to mean Morgan Stanley has been overweight equities, not Mike Wilson’s team of analysts. That’s the market and market “experts” we’re working with folks! Tread cautiously and with morally reputable resources!

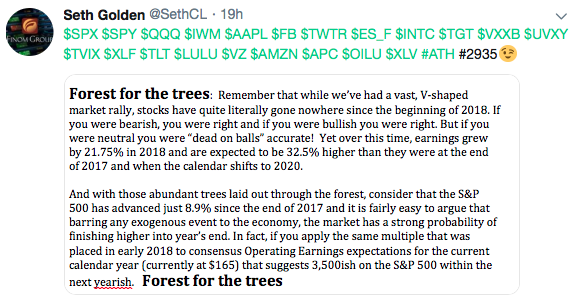

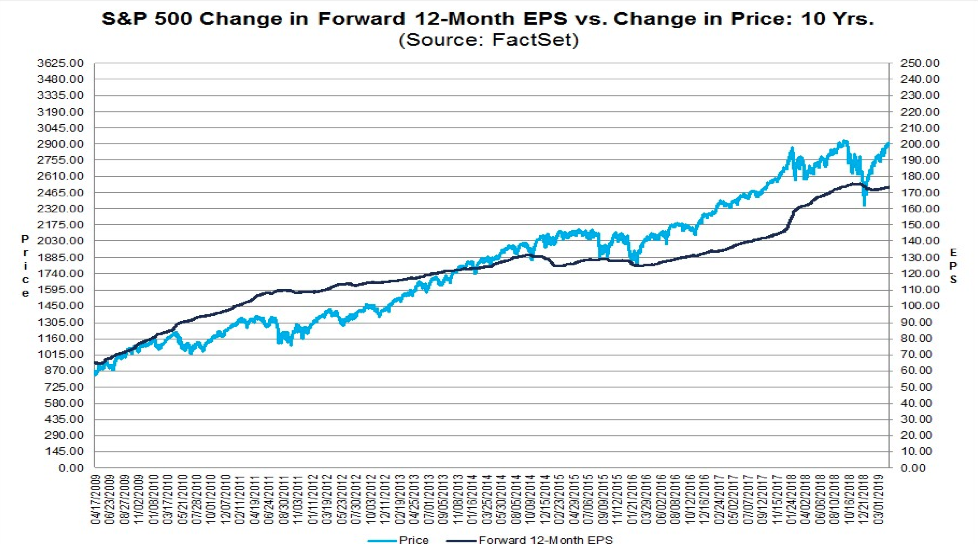

Lastly, but certainly not least, we ask investors to consider these very important points with regards to the last 15 months give or take and from Seth Golden’s Tweet on Tuesday. It paints a bigger picture on what has happened within the S&P 500 and with regards to corporate earnings since the tail end of 2017.