Up, down and all around went the markets yesterday and post the Fed rate hike announcement. The FOMC, led by Jerome Powell, approved the widely expected quarter-point hike that puts the new benchmark funds rate at a target of 1.5% to 1.75 percent. It was the sixth rate hike since the Federal Open Market Committee began raising rates in December 2015.

Alongside the increase in rates came another upgrade in the Fed’s economic forecast, and a hint that the path of rate hikes could be more aggressive in the out years (Hawkish in nature). Fed officials raised their forecast for 2018 GDP growth from 2.5% in December to 2.7%, and increased the 2019 expectation from 2.1% to 2.4 percent (Hawkish in nature).

The market currently expects three hikes for 2018, which remained the Fed’s forecast, but at least one more increase was added for 2019. Moreover and as it pertains to 2018 rate hikes, had one more member indicated a higher funds rate, the forecast likely would have gone from 3 to 4 hikes in 2018. Given the economic strength in the latter period of 2017 and early portion of 2018, economists and analysts had been elevating their rate hike expectations from the Fed to 4 rate hikes. The fed funds futures market was indicating a 38% chance of it just before the committee statement was released. Having said that, some of the more recent economic data has come in below expectations including retail sales and wage inflation.

With regards to inflation expectations, the FOMC’s 2018 forecast remains just 1.9% for both core and headline inflation. For 2019, the forecast for core personal consumption expenditures edged higher to 2.1% from 2%, while headline remained at 2% (Dovish in nature). Surprisingly, Fed officials now see unemployment running lower than before. Currently at 4.1%, officials now see the rate for 2018 at 3.8%, down from the 3.9% offered in December. What is surprising is the strength in the labor force juxtaposed with inflation expectations. Usually we would get greater wage inflation at this point, but as the Fed is suggesting, they don’t see much in the way of wage inflation… yet raising rates?

Taken altogether, much of what the Fed delivered was expected and the baseline rate hike expectation remains at 3 hikes for 2018. But where is the inflation warranting further tightening and/or rate hikes in general? Equities rose sharply upon the initial announcement, but quickly gave up all gains during the Fed Chair’s press conference. All three major indices finished lower on the day and on Thursday equity futures are sharply lower. Alongside equity futures falling, bond yields are following suit with the 10-year yield diving in the early market hours.

Additional comments from Jerome Powell may have spooked the markets to some degree, as he stated some asset classes might be elevated. While some asset prices are elevated, particularly “some” equity prices and pockets of commercial real estate, financial vulnerabilities are still not at extreme levels, Powell said. Powell went on to say that he was not worried about excess leverage in the financial sector.

“Banking sector and household balance sheets are in good shape.”

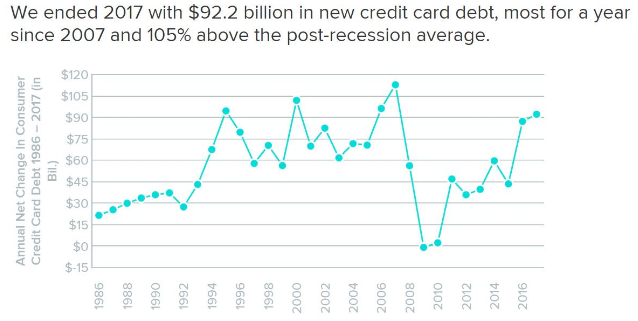

If Powell is recognizing that household balance sheets are in good shape… why raise rates, which would otherwise raise interest rates on credit card debt? Are they that concerned with the yield curve and possibly not recognizing that “this time might just be different”? And again, where’s the inflation they would otherwise be attempting to curb with rate hikes? The Fed’s rate hike might hurt consumers the most going forward if it remains on its current path. In a report this week, WalletHub analyzed data and found that U.S. consumers have been piling on credit-card debt at an alarming pace, adding $92 billion in new debt last year alone.

Credit card companies adjust the interest rate higher that they charge their customers after the Fed raises key interest rates. When the interest rate moves higher, the minimum payment goes up and potentially forces the consumer to reduce overall consumption. This has the potential to also bleed into the housing sector over time. The Fed is actually artificially creating inflation that otherwise would not exist. According to Bankrate.com, the average credit-card interest rate is 16.8%. Is the Fed on a collision course with the consumer?

Another question begs to be put forth as follows: “Is the Fed making a policy error by continuing its course of rate hikes”? I offer up this question as I opine on the notion of inflation, using the Fed’s own metric of significance. An opinion could be put forth that there is only “reflation” and not inflation. The notion of reflation is identified by nearly all measures of inflation the Fed utilizes that otherwise finds the long-term rate of Personal Consumption and Expenditures stagnating year-over-year at best with periods of deflation followed by inflation and resulting in “reflation. The Fed’s target inflation measure hasn’t risen more than 2.2% in any year since 1993. That’s a rounding error above the Fed’s 2% target and compensated for by the decade spent at 1.8% annually, or below. So why is the Fed raising rates? Fear of the economy overheating? GDP isn’t showing signs of an overheated or overheating market even as we’ve embarked on tax reform that acts as an agent of economic stimulus. Only the consumer will get hurt by these rate hikes and while the bull market and expansionary period of the economy may be long in the tooth, neither die of old age, they die due to Fed policy decisions. Some may be found calling these decisions mistakes… in hindsight.