Kristin Hooper of Investco

One month ago in this blog, I noted that April would be a critical month to gauge the global response to the COVID-19 pandemic. Across the board, it was a massive response, including significant monetary and fiscal stimulus from a variety of economies and widespread lockdowns designed to slow the rate of infection. But as we enter May, we are seeing differences in approach come to the fore — between countries, between localities, and between political parties.

How will we know which approaches are working to stem the rate of infections and to get people back to work? By examining the data. Here are some of the key issues that we will be watching in May:

1. Infection rates. Some European countries have begun to roll back lockdown measures, and some states within the US have also begun to loosen restrictions. The concern, of course, is that a second wave of infections may arise as a result, especially given that a number of the state rollbacks are occurring in contradiction of White House guidance that a loosening of restrictions should occur after 14 consecutive days of declining infection rates. And so we will be watching infection rates very closely for signs of a resurgence. If there isn’t a second wave, that would certainly encourage other countries and other US states to open more areas of their economies. If, however, there is a second wave, restrictions may have to be reinstated, prolonging the period of time before economic activity can re-accelerate.

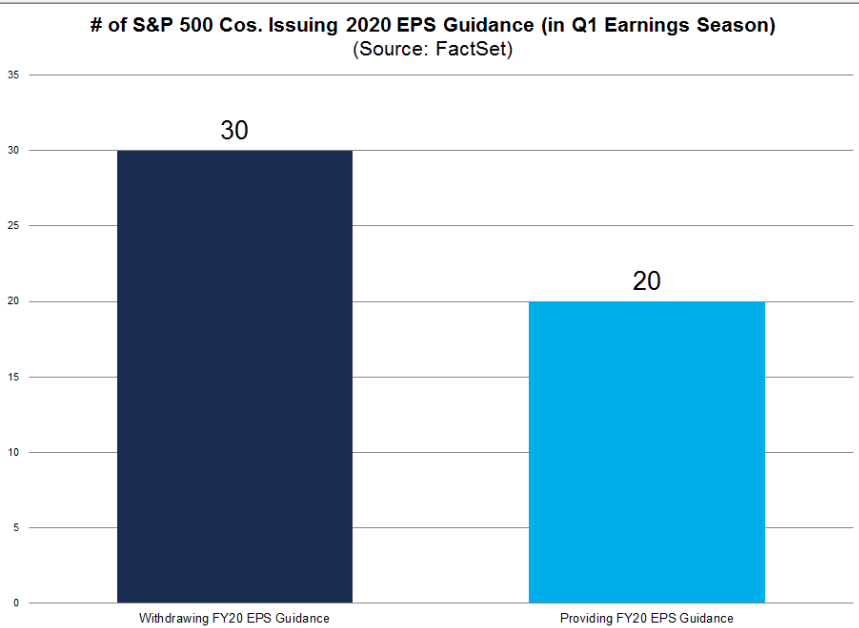

2. Earnings. We are in the midst of earnings season with 55% of companies in the S&P 500 Index having reported earnings, and 45% still left to report.1 Importantly, much of the first quarter brought relatively normal activity before the pandemic spread in earnest. Therefore, from my perspective, the most important part of this earnings season is the forward guidance — and there has been relatively scant forward guidance on earnings from companies. FactSet Research found that, of the 122 companies that reported earnings as of April 24, only 50 (41%) discussed earnings guidance for 2020. Of those 50 companies, 30 said that they had withdrawn or were withdrawing previous earnings per share guidance for 2020 because of “the uncertainty of the future impacts of COVID-19.”

Only 20 companies actually provided earnings guidance for the year: 10 lowered their previous guidance, six maintained their previous guidance, and four actually raised their earnings guidance. But while companies have not provided much guidance themselves, analysts have been slashing second-quarter earnings estimates at a dramatic clip. This is the single largest decline in a quarter’s earnings estimates to be made by analysts in the first month of the quarter since FactSet began tracking this statistic in 2002. It would be helpful to hear from more companies about any forward guidance they can provide — or lack thereof — during this crisis even if it involves a variety of possible scenarios dependent on monetary, fiscal and health policy as well as medical outcomes.

3. The US Employment Situation Report for April. This is going to be an ugly report: According to Barron’s, consensus estimates are for an unemployment rate of 16% and a loss of 21 million nonfarm payrolls. It could be even worse. Investors should expect the report to be shocking and not be caught by surprise — we have to keep in mind that there has been a dramatic drop in economic activity compressed into a very short time period, so the employment losses should be massive. What’s more important than the job numbers is what policymakers are doing to maintain solvency in the face of this.

4. Negotiations about Phase 4 fiscal stimulus for the US. While the ink is barely dry on Phase 3.5 of fiscal stimulus passed just two weeks ago, I believe the US needs to see another fiscal package soon, particularly one that’s geared towards state and local governments, as well as additional support for small businesses. This will not happen without serious debate, however, given Senate Majority Leader Mitch McConnell’s suggestion that perhaps states should just file for bankruptcy — or at least they should not expect a check to “finance mistakes” not related to the pandemic. I believe a lack of economic support for states could be disastrous and only amplify the current downturn, given that state and local governments combined are a major employer. I suspect that we will see heated debate on this topic, but I believe that ultimately Congress will pass another stimulus bill that provides support for state and local governments, small businesses and other entities.

5. Possible re-ignition of the tariff war between the US and China. The United States is becoming more vocal in blaming China for the pandemic. Last Thursday, President Donald Trump threatened to apply new tariffs to China in retaliation. The next day, White House economic advisor Larry Kudlow also suggested there could be retaliation of some kind. We will want to follow this situation closely as any new tariffs would place more pressure on the US and global economies — and even the threat of such tariffs could significantly impact the stock market, as we saw in recent days. Over the last six weeks, the stock market has enjoyed a decoupling from the economy as a result of monetary and fiscal stimulus, but that could change with the risk of another tariff war.

6. Brexit negotiations. Yes, despite the pandemic, Brexit negotiations are continuing. If a deal is not struck by the end of 2020, the trading terms between the UK and European Union would default to World Trade Organization terms. This would be a negative development, especially for the UK, dealing a blow to an economy that has already been hit hard by the novel coronavirus contagion. We will want to follow this situation closely as well. Given COVID-19, there is certainly a very compelling rationale to extend negotiations beyond the end of 2020.

7. Data reports. There are several key economic data reports we will want to watch in the next month, including:

- US Retail Sales for April

- US Industrial Production for April

- China Retail Sales for April

- The University of Michigan Consumer Sentiment Index (preliminary)

- ZEW Financial Market Survey – economic sentiment for May

- UK Retail Sales for April

- IHS Markit Eurozone Composite PMI for May (preliminary)

- Eurozone Business Climate for May

- Eurozone Consumer Confidence for May

- US Consumer Confidence

- US Durable Goods for April

This economic data will give us a sense of where various economies are in terms of bottoming, in the case of most, and recovering, in the case of China.

Perhaps the biggest question I get from clients is about the shape of the economic recovery — whether we can rebound quickly into a V-shaped recovery, or whether we will linger at the bottom of economic activity for an extended period. As I have said many times before, I continue to believe that the shape of the economic recovery will be dictated by three policy prongs: health, fiscal and monetary. We’ve seen impressive steps in each category so far, but there is still a long way to go, and differences in approach are marking the path ahead. I expect May to shed more light on what’s working and what needs to be rethought, helping us get a better sense of the shape of that recovery.

Scott Wren, Senior Global Market Strategist at Wells Fargo

Key takeaways

- The stock market is looking well beyond the deep but short recession we are expecting and focusing on the potential for better days ahead.

- Anticipated increased future consumer spending based on an easing of stay-at-home directives and pent up demand is a big part of the market’s enthusiasm.

Back on April 1, when we initially took a look at the question of what the stock market might be pricing in in terms of the evolution of the COVID-19 pandemic and its effect on consumer spending and the stock market, we were in the midst of a surge in the numbers of diagnosed cases and, unfortunately, deaths due to the virus.

In early April, we speculated that the stock market was pricing in a mid-May peak in new coronavirus cases. But news in recent weeks has been more upbeat with many projecting that the peak may come a bit earlier. However, looking at current Centers for Disease Control (CDC) data through last Friday, new U.S. cases on a daily basis have moved sideways since mid-April rather than trending noticeably down. But we are seeing good news from New York state as it appears to be well past the peak as the number of new cases on a daily basis has declined meaningfully. It is also interesting to note that the S&P 500 has rallied slightly more than 14% since the middle of last month. The stock market is certainly pricing in the beginning of a downtrend in new virus cases for the U.S. as a whole.

The labor market and other economic news in recent weeks has been terrible, and that is unlikely to change soon. This Friday’s employment report could easily show a mid-teens unemployment rate and a loss of more than 20 million jobs in the month of April. But investors continue to look beyond the bad current news and see brighter skies on the horizon. The initial projections of economic contraction in the third quarter have given way to a view of positive growth that would carry through the end of the year and into 2021. We have been predicting a short but very deep recession that appears to have started earlier than we initially thought but will likely still end in the second quarter. The market seems to agree.

In terms of the coronavirus, there have been additional hints of potential good news on the both the treatment and vaccine fronts. We know there are numerous world-class companies and universities around the globe and here at home that are working hard to produce medicines designed to help cure or prevent the virus from spreading through the population. The equity market, at current levels, is pricing in an expectation that additional good medical news is still to come, at least in our opinion.

The bottom-line question is what will American consumers do? The market appears to also be pricing in a successful initial “reopening” of at least some segments of the economy with an expectation that pent-up consumer demand will follow reasonably soon.

Our view is that market expectations are probably a bit ahead of themselves and a pullback would not be a surprise after this major rally.

Jeffery Miller is now a part of the team behind Incline Investment Advisors. Check out Incline Investment Advisors and see what they can do for you.

“Since 1928, reviewing the past 25 bear markets, there has been a lower price put in by the S&P 500 index 60% of the time.”

Suppose this statement is accurate. Is it worrisome?

- It means that there was a lower price 15 times, but not the other ten. Looking at the actual numbers instead of creating 60% “odds” presents a clearer picture. The chance of returning to the lows would be little more than a toss-up. 25 cases do not provide a very good sample for this type of conclusion. Suppose that you learned that your child’s class had 15 girls and ten boys. If a new student transferred in, would the odds be 60% that it was a girl? If you looked at another class at the same school would the gender division be the same?

- Are the prior bear markets similar to current conditions? No, they actually seem quite different. Every metric I examine shows unprecedented readings. Investors are confronting a unique problem. Will the recovery be as fast as the decline? Will it require revisiting the lows? I don’t know, and I won’t find out by looking at past bear markets.

What can we learn from the data? The author writes as follows:

Making a finer point, however, Bespoke notes that of the 11 bear markets from 1928 through 1940, 9 of them saw the S&P 500 make a lower low, but since 1940 most bear markets have tended not to see retest (see attached table):

Another way of describing the result would be to look only at the time after the Great Depression. Six of 14 cases, only 43%. Or look at the time since 2000 and say that a new low was made 75% of the time!

Takeaway for Investors

I chose an article that accurately provided all the data and where the author’s conclusions were modest and nuanced. The headline is another matter.

- Look past the headline. These are often presented in a dramatic manner that overstates the evidence.

- Ask whether the evidence supports the conclusion. You need not be an expert in statistics to spot problems like an inadequate number of relevant cases.

- If possible, look at the data yourself. What patterns, if any, do you see? If you were to write a report summarizing the information, what would you say?