Last Friday’s stock market rally carried forward on Monday with the tech-heavy Nasdaq leading the way. The Nasdaq Composite closed at a record for the first time since March 12, rising 52.13 points, or 0.7%, to 7,606.46. The S&P 500 finished up 12.25 points, or 0.5%, to 2,746.87. The Dow Jones Industrial Average advanced 178.48 points, or 0.7%, to 24,813.69.

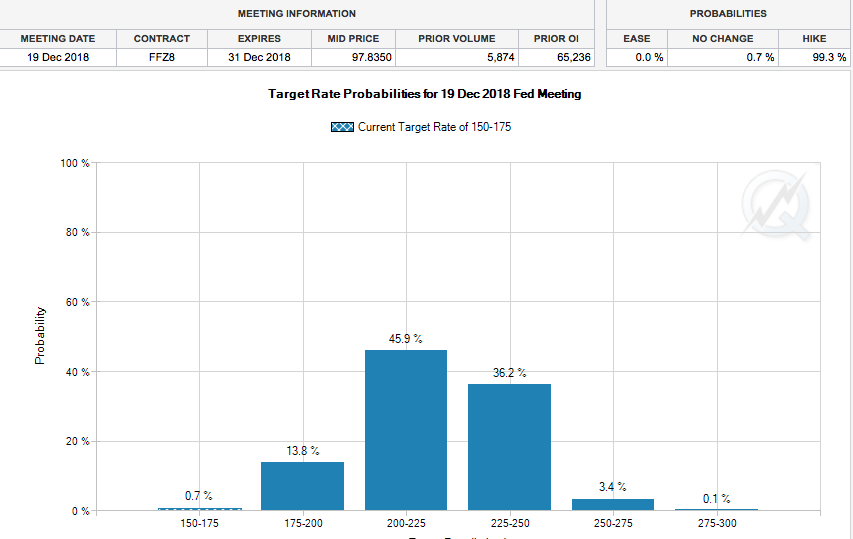

Equities rallied in the face of a sell-off in bonds and with the 10-yr Treasury yield creeping toward 2.95% once again. A recent speech by Fed Gov. Lael Brainard has helped dispel the belief that policymakers may hold off on a fourth rate hike this year. Brainard said she would not slow down the pace of rate hikes based on a flattening yield curve, which some have read as the bond market pricing in an economic slowdown. The CME’s FedWatch Tool has shown an increase in the probability of a 4th rate hike since bottoming last week below a 20% probability. Since then, the probability has increased to above 35% as shown below.

U.S. equities have chosen, at least for the time being, to forgo concerns about trade and geopolitical issues surrounding the European Union. But these concerns are still looming underneath the surface of equity markets. What is serving to offset these risks is the general economic backdrop of the U.S. economy that is steadily improving and ratcheting corporate earnings forecasts higher.

“With Italian political risk on the backburner, focus may shift toward the trade front and whether or not Europe, Canada and Mexico will follow through with retaliatory action. While last week’s Italian government formation and positive Friday data (employment and ISM) drove a rebound in yields, we think there is room for Treasuries to sell-off further,” said Jonathan Cohn, interest-rate strategist for Credit Suisse.”

As it pertains to those trade talks with China, little has been detailed since Commerce Secretary’s weekend meetings in Beijing. What we have learned has largely come from China’s latest “threat”. Beijing threatened that it won’t abide by a deal on farm and other products if the U.S. goes ahead with sanctions and tariffs. U.S. Commerce Secretary Wilbur Ross and Liu He, China’s economic czar, held discussions centered on getting China to carry out recent promises to buy more American farm and energy products. Basically, before committing to anything, the Chinese side wants assurance that Washington won’t go ahead with its tariff threats.

A statement released Sunday by China’s official Xinhua News Agency said both sides achieved “concrete progress” in areas including agriculture and energy but details are yet to be hammered out. “If the U.S. introduces trade sanctions including tariffs,” the statement added, any results from the negotiations “won’t go into effect.”

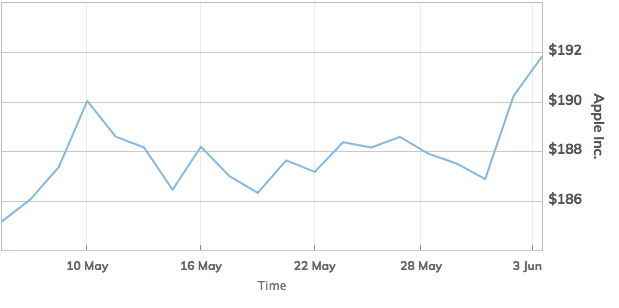

In corporate news, Apple’s 11th annual WWDC kicked off Monday with a keynote speech at 1 p.m. Eastern time. Among the announcements were new augmented-reality features for its next mobile operating system, iOS 12, a measuring app that makes use of AR technology to map the dimensions of real-life objects, changes to its stocks, news and CarPlay apps and new personalized, animated emojis, called “memoji.” Apple’s stock rally has pushed the technology giant’s market capitalization to $942.9 billion. It would take a further 6.1% gain from current levels for Apple to become the first $1 trillion company.

One of the biggest reasons for the tech sectors most recent surge, the Nasdaq closing at a record high and the market’s recent resurgence is Apple and the level of buybacks being executed in 2018. U.S. corporations are on track to deliver $700 billion to $800 billion in buybacks, $500 billion or more in dividends, and $1.3 trillion in M&A. Announced buybacks in the tech sector are up $160 billion, or 200%, in 2018 (with Apple Inc. accounting for $100 billion). That accounts for more than 60% of S&P buyback announcements and nearly all the year-over-year increase. Such share repurchase activity coupled with a strengthening economy makes for a difficult market to short for the bears.

In other Apple-related news from the WWDC, the consumer goods and services giant unveiled new controls to help people curb the amount of time they spend on iPhones and iPads, as well as allow parents to remotely track and limit their children’s use of those devices. The company said a new app it will release in September called “Screen Time” will provide users with weekly reports of the apps they use and allow them to set time limits for their use of those apps. Parents will be able to use the system to remotely monitor the apps their children use and limit their time on devices.

The headlines haven’t stopped when it comes to Starbucks and with that, after the closing bell yesterday there was another announcement surrounding the company. Howard Schultz will step down as executive chairman and as member of the retailer’s board at the end of the month, according to a memo from Schultz to employees. Shares of Starbucks fell more than 2% after the news. Schultz will become Starbucks’ chairman emeritus on June 26. “As I prepare to step away, I’d like to humbly remind you not to lose sight of what matters most: your fellow partners and our customers,” Schultz wrote. “Onward with love,” he signed off.

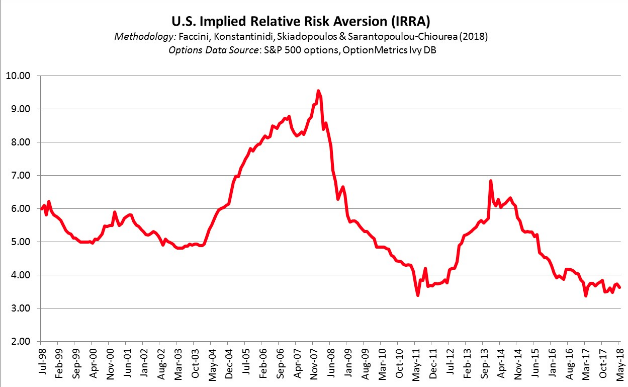

While individual stock performances will vary over time and sometimes find themselves impacted by headlines, the market is sending signals that the economy is expected to continue on its current path or growth trajectory. The options market, in particular, tells us the degree to which investors are averse to risk. The Implied Relative Risk Aversion data (IRRA) offers insights into how investors feel about the economy through their participation in the options market. A decrease in IRRA predicts an increase in economic growth because investors boost investments when they become less risk averse. Conversely, an increase in risk aversion points to a slowdown in growth because investors lower investments when they become more risk averse. Implied Relative Risk Aversion is currently very low, at 3.6 for May, implying that traders in the S&P 500 options market anticipate an increase in U.S. economic growth.

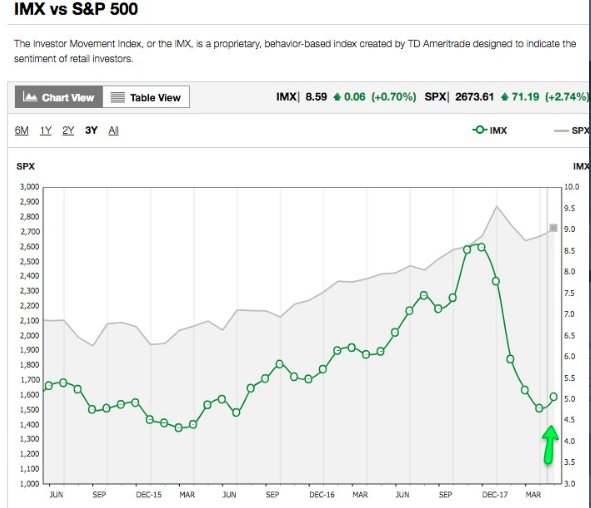

In addition to the insights from the IRRA, the latest from TD Ameritrade’s Investor Movement Index (IMX) proved positive for the markets in May. The IMX increased for the first time in 5 months, increasing to 5.06, or 5.64% during the period.

TD Ameritrade clients increased their exposure to equity markets during the May IMX period. Clients were once again net buyers of equities, causing the increase in the overall IMX score. Volatility of the S&P 500 was relatively modest during the period, with the index only having one day with a change in excess of +/-1% during the period.

It remains to be seen whether or not global trade issues will throw a wrench into the latest surge in the equity markets. Investors would be wise to keep with the pulse of ongoing trade discussions and active portfolio management.