Certainly we’ve all heard the term, “don’t fight the Fed”? As we enter rate decision and future rate forecasting week, the theme and terminology will loom large overhead the markets around the globe. As we discussed in this week’s weekly Research Report, a binary outcome for the week is founded upon the FOMC and ECB meetings this week that kick-off on Tuesday and are already found with market reactions overseas.

European Central Bank (ECB) President Mario Draghi defended the tools that the organization has available on Tuesday, saying that it could cut interest rates again or provide further asset purchases if inflation doesn’t reach its target.

Speaking at the ECB Forum in Sintra, Portugal, Draghi gave a defiantly dovish tone, saying that if the economic situation deteriorates in the coming months the bank would announce further stimulus. The euro dropped 0.2% against the dollar in a matter of minutes as Draghi delivered the remarks.

“In the absence of improvement, such that the sustained return of inflation to our aim is threatened, additional stimulus will be required,” Draghi stated.

The (European) Treaty requires that our actions are both necessary and proportionate to fulfill our mandate and achieve our objective, which implies that the limits we establish on our tools are specific to the contingencies we face. If the crisis has shown anything, it is that we will use all the flexibility within our mandate to fulfill our mandate — and we will do so again to answer any challenges to price stability in the future.

We remain able to enhance our forward guidance by adjusting its bias and its conditionality to account for variations in the adjustment path of inflation. This applies to all instruments of our monetary policy stance.

Further cuts in policy interest rates and mitigating measures to contain any side effects remain part of our tools. And the APP (asset purchase program) still has considerable headroom.”

The headlines from the ECB President have sent global bond yields to record level lows with the German Bund at its lowest level in history.

U.S. bond yields are spiraling to their lowest levels in more than 2 years and likely further forcing the FOMC’s hand, a rate cut in the near future. The FOMC will kick-off its 2-day meeting on Tuesday and culminate its June meeting with a rate announcement and press conference Wednesday at 2:00 p.m. EST.

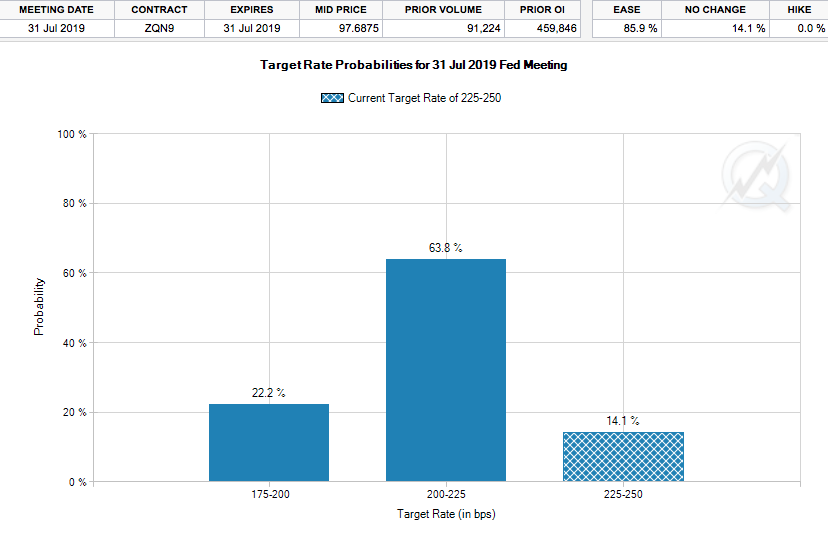

The market is not “demanding” a rate cut for the June 2019 meeting and giving a rate cut only a 27% chance of occurring. With that said, the probability of a Fed rate cut of at least 25 bps in July has moved up to greater than 85% as of Tuesday.

Most economists and analysts are anticipating a shift in language from the FOMC in favor of a rate cut as early as July, removing the word patient. Here is what a well-regarded Fed watcher, Tim Duy, had to offer with respect to the expected dovish shift in language he expects from the Fed when it releases its statement Wednesday:

“In the FOMC statement, I expect the Fed will signal that a more dovish stance by replacing “the Committee will be patient” with “the Committee will act as appropriate” to sustain the expansion. I would expect Powell in his press conference to note that “appropriate” policy could be a rate hike, but we all kind of know which way the wind is blowing. It would be a signal that the odds of a rate cut clearly outweigh the odds of a rate hike.

What about the dots? Powell, in his recent Chicago speech, told us ignore the dots in favor of understanding the dynamics behind the dots:

A focus on the median forecast amounts to emphasizing what the typical FOMC participant would do if things go as expected. But we have been living in times characterized by large, frequent, unexpected changes in the underlying structure of the economy. In this environment, the most important policy message may be about how the central bank will respond to the unexpected rather than what it will do if there are no surprises. Unfortunately, at times the dot plot has distracted attention from the more important topic of how the FOMC will react to unexpected economic developments. In times of high uncertainty, the median dot might best be thought of as the least unlikely outcome.

“With respect to the dots, I have quite a bit of sympathy for the Fed’s communication challenges. The dot plot arose from a good faith effort on the part of the Fed to more fully communicate the analysis behind monetary policy decisions. What is being communicated, however, is not a consensus view whereas the actual policy decision is a consensus view. The Chair is stuck trying to bridge that gap in the press conference, sometimes less successfully than other times.“

Still, what has been given is difficult to take back. Powell can downplay the dots, but they will nonetheless be published. And if they are published, we have to talk about them. That’s the way this works. I expect the 2020-rate median projected rate hike will revise away. I think the 2019 median will hold steady. My expectation is that there will be at least one dot that anticipates a rate cut later this year. Regarding the remainder of the forecasts, I expect that the inflation forecast for this year and the longer-run employment forecasts will both be revised lower. Due to the solid first quarter GDP number, the growth estimate is likely to be revised higher.

Bottom Line: The Fed is likely to turn more dovish this week and open up the possibility of a rate cut. I think they still need more data to justify a rate cut. Another jobs report alone the lines of the May report would go a long way toward supporting that cut in July.

Expectations for signaling a rate cut are pretty unanimous, which creates a risk in and of itself to the market should the Fed disappoint with its statement and language during the post-statement/rate decision press conference. Goldman Sachs analysts/economists are not of the opinion a rate cut is necessary without more economic weakness showing up in the economic data, the outlier of the analysts community to-date.

Goldman Sachs chief economist Jan Hatzius wrote today: “A Skeptical View of Insurance Cuts”. Hatzius thinks the Fed will remain data dependent (any rate cut will be based on the data), and not cut rates as “insurance”. We think the hurdle for such cuts is likely to be higher than widely believed.”

Goldman economists said the three-quarter point in rate cuts in 1995-1996 and 1998, which some analysts point to as recent examples of pre-emptive policy easing from the Fed, were responses to data “rested at least as much on observable deterioration as on an insurance motive.”

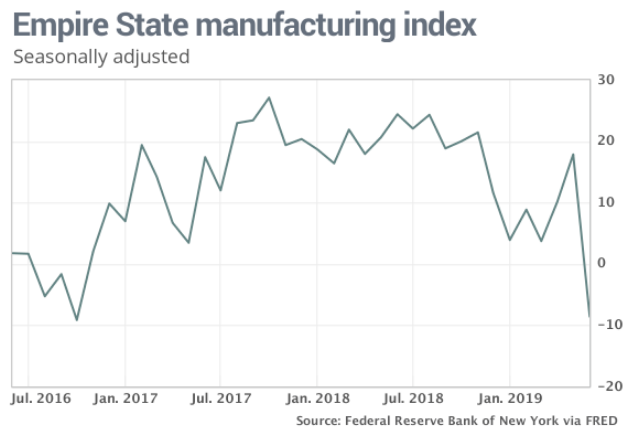

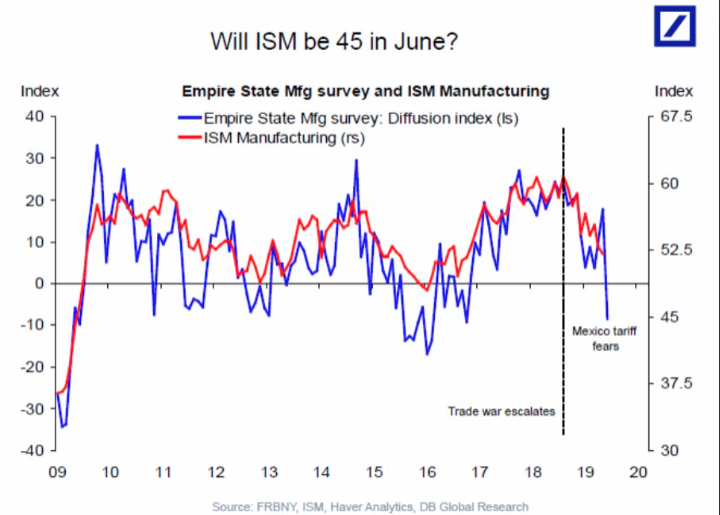

The backdrop or cover for the Fed to signal a rate cut continues to improve, as the economic data shows deterioration in the manufacturing sector by and large. The New York Fed’s Empire State business conditions index took a sharp turn for the worse in June, falling into negative territory for the first time in more than two years.

The Empire State manufacturing index plummeted 26.4 points to negative 8.6 in June, the New York Fed said Monday. That’s a record decline. Economists had expected a reading of positive 10, according to a survey by Econoday.

The Empire State manufacturing plunge was somewhat shocking to investors when released on Monday. Finom Group urges investors to consider, however, that the weakness was largely due to uncertainty surrounding the threat of Mexico tariffs moving toward implementation. This likely created the collapse in the composite index activities.

It’s been pretty clear that even without implementing tariffs that had been previously threatened, the threats alone have taken their toll on the manufacturing sector. Additionally, corporations have reacted by pulling in the purse strings, curtailing capital expenditures. According to Deutsche Bank’s Capex tracking, “The incoming data shows that the trade war is having a much bigger impact on business hiring and capex decisions than the consensus thinks.”

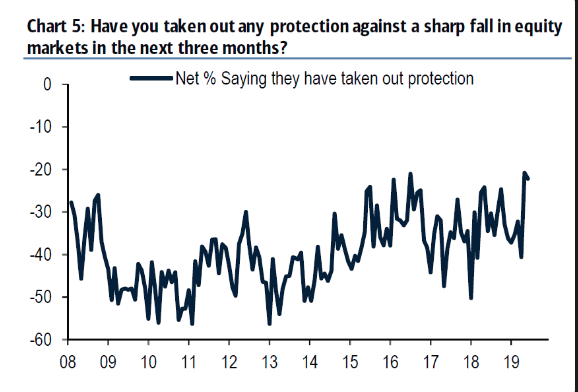

With a continued focus on what the Fed will say and/or do, there are no absolute certainties, but one thing is for certain, investors are prepared and continue to prepare for the potential of an adverse market reaction to the downside. Investor hedging is at multi-year highs.

When it comes to predicting an outcome for any particular FOMC meeting, this likely proves to be an inconsequential exercise long-term. The Fed at some point will step forward to backstop the U.S. economy, using a litany of tools at its disposal and as such any weakness in the economy or the markets is likely temporary. Will they or won’t they for the current meeting date will offer lots of headlines and consternation and is bound to disappoint those with lofty expectations. Underneath the present concerns, however, rests a fundamentally strong economy that is weakening, but only weakening from above trend-growth to trend-growth conditions presently. There’s nothing wrong with trend-growth, especially when contending with an 18-month and ongoing trade feud. Having said all of that, Morgan Stanley continues to warn investors that even if/when the Fed does come to the rescue so far as market expectations, it may not prove to eliminate the prospects and eventuality of a market decline.

Morgan Stanley points to weakened oil demand, capital spending, manufacturing and its proprietary Business Conditions Index. The firm believes that all the weakening will lead to continued negative earnings revisions, which is consistent with defensive equity positioning. The firm does anticipate recommending a rotation back to more cyclical positioning once valuations come down to “absolutely cheap levels, some 10% lower than present valuations”.

Although Morgan Stanley has maintained a bearish stance on the equity markets throughout 2019 and largely based on an earnings recession thesis, that thesis hasn’t born fruit. Heading into the Q2 earnings season, FactSet has forecasted an earnings decline of -2.5% for the S&P 500. Finom Group expects the forecast to deteriorate further over the next few weeks and before a trough is found. While this expectation may come true, the market has continued to rise through June, rebounding since the May pullback in the major averages. Why?

On June 4 Fed Chair Jay Powell signaled a possible cut by saying “we will act as appropriate to sustain the expansion,” and since then, as of Friday, June 14, 2019, the S&P 500 is up 5.6 percent.

The Fed hasn’t cut rates since the Great Financial Crisis of 2008. Moreover, the last two starts to easing cycles (a cut in rates after a series of hikes) in January 2001 and September 2007 immediately preceded recessions. Those business cycles were about to end due to the tech bubble and financial crisis, and Fed policy far too tight heading into those recessions. Where we are in the business cycle is of critical importance to the easing outcome.

As you can see in the chart above, after the five initial rate cuts before 2001 (1984, 1987, 1989, 1995, and 1998), the S&P 500 rose an average of 11.1% and 15.8% over the subsequent 6 and 12 months, respectively. Even including the poor stock market performance after the 2001 and 2007 cycles, the average S&P 500 gains over subsequent 6 and 12 months were a respectable 4.5% and 5.8 percent.

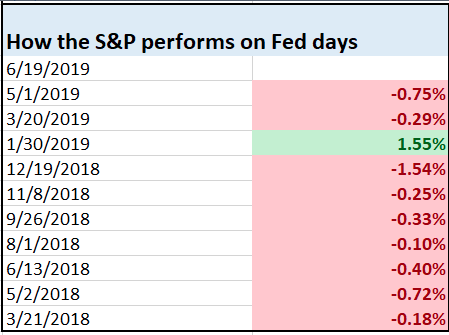

It can prove difficult to forecast how the market will react to what the Fed says and/or does and as such we’d encourage investors to focus on the economic fundamentals more so than the Fed, or at least broaden the focus. With the markets having rallied through much of June, the anticipated dovish Fed statements may prove a “sell-the news event”; you never know. What we do know is what the Jerome Powell-led FOMC results have been on “Fed decision days”.

Yep, Jerome Powell has a horrific track record when it comes to S&P 500 performance on Fed days. Given the 10 Fed days for which have been found under Powell’s leadership, the market has finished in the red 9 times. With this in mind and the market having rebounded nearly 6% off its May lows… will this prove another “sell the Fed” day on Wednesday?

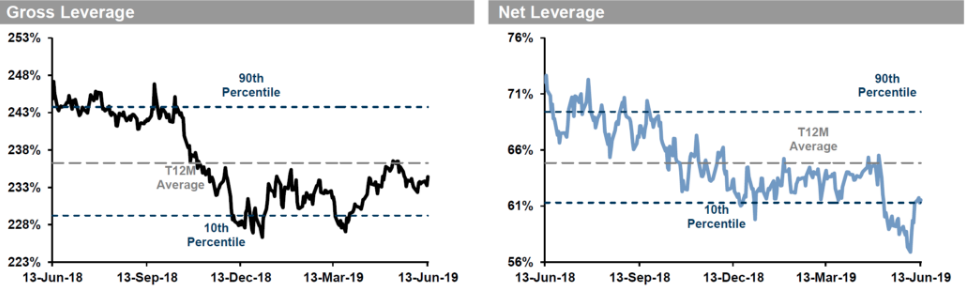

While we can’t say for sure how the market will react, we would be of the opinion the immediate reaction may prove short-lived unless earnings surprise to the upside again during the Q2 reporting period. By and large, most investors have remained with light exposure/leverage to the overall market for the vast majority of the year. After the May swoon, leverage to the market trough and has since rebounded, but remains with very low leverage amongst CTA/s and trend-following market strategy participants.

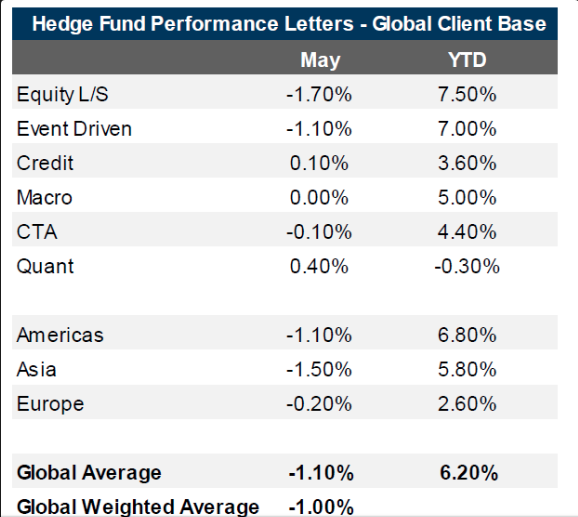

And according to Goldman Sachs, this has produced similar market underperformance in the face of a double-digit market rally year-to-date. If you think you’ve missed a rally that everyone else has captured, think again!

As we look forward to the Fed’s announcement on Wednesday afternoon, the economic data calendar remains light and slanted toward the housing sector. With a slight dip in the NAHB homebuilder sentiment index in May, more housing data is set to be released on Tuesday. Housing starts and Building Permits set the stage for Existing home sales data to be released on Friday. Housing starts are expected to tick slightly lower in May.