It’s now or never. At least that was how Nomura’s Charlie McElligott characterized the potential for a market decline last Thursday for clients.

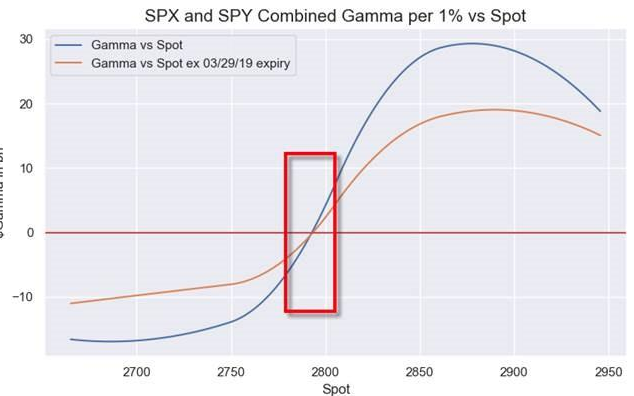

Having previously warned about the “pullback window”, McElligott now specifies the timing of the event, noting that “it has to happen now”, as he currently estimate SPX/SPY consolidated Dealer Gamma to turn “negative” in approximately the same area ~2790 area the bank’s CTA pivot level… “so this next five days is the “PEAK WINDOW” for this “alignment” of Dealer Gamma, Rebalancing flows and CTA sell triggers.”

McElligott had been pounding the table about a market sell-off since the rebound in January, but kicked his analytics into high gear in late February. It was at this time that McElligott’s media outlet of choice headlined his 4-part series and titled it the Ides of March.

And just to revisit his earlier rational for a market decline, here are the main reasons McElligott offered for a March sell-off that never came to pass.

- seasonality of the March Quarterly Options “Quad Witch” Expiry (which historically sees Equities “trade up” into then sell-off thereafter) which is ESPECIALLY notable in light of…

- current “extremes” in $Delta (SPX / SPY / QQQ) and $Gamma (QQQ) which could also align with…

- the commencement of the next Corporate Buyback “blackout” into earnings season, together with

- another “mechanical” function of Systematic Trend / CTA’s over-weighted allocation to the 1Y period model and the “pull higher” of SELL trigger levels—all of which could conspire to create a “gap lower” risk for markets on a “pure” tactical reversal in short-term “supply / demand” dynamics.

So you thought you had a tough job did you? While McElligott’s forecast and/or prediction didn’t quite pan out as his analysis planned for, the markets have flipped the calendar to April and are going to contend with probably the most relevant economic data on Friday. We’d be of the opinion that McElligott is hoping the Nonfarm Payroll (NFP) report serves to find his Ides of March theses just a little premature, with an underwhelming NFP that finds the market under pressure. The NFP report is due out Friday morning ahead of the opening bell. Economists polled by MarketWatch estimate 179,000 jobs were created in the month of March.

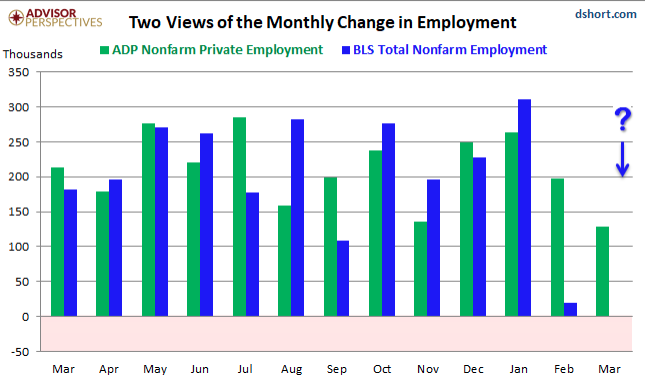

Ahead of the all-important NFP report Friday, the private sector payroll report was released in the form of the ADP payroll report. The following chart depicts the ADP Payroll reports against the same monthly NFP report.

Employers in the private sector hired 129,000 workers in March, payroll processor ADP said Wednesday. That was the weakest showing in 18 months and missed the consensus among economists surveyed by Econoday for job gains of 165,000.

“The job market is weakening,” Moody’s Analytics Chief Economist Mark Zandi said. Still, February figures were raised by 14,000 jobs.

In March, small businesses added just 6,000 jobs, medium-size firms added 63,000, and large employers hired 60,000 workers. All of the gains were in the service sectors: goods-producers lost 6,000 jobs.

“The economy is struggling with fading fiscal stimulus, the trade uncertainty, and the lagged impact of Fed tightening,” Zandi added. “If employment growth weakens much further, unemployment will begin to rise.”

Jim O’Sullivan, chief U.S. economist for High Frequency Economics, said after the ADP release that he was sticking with his original forecast for a 200,000 rise in payrolls to be reported by the Labor Department. O’Sullivan has been MarketWatch’s “Forecaster of the Year” for eight years running.

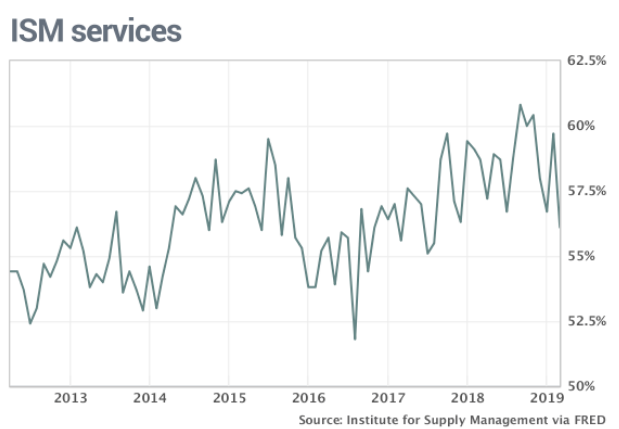

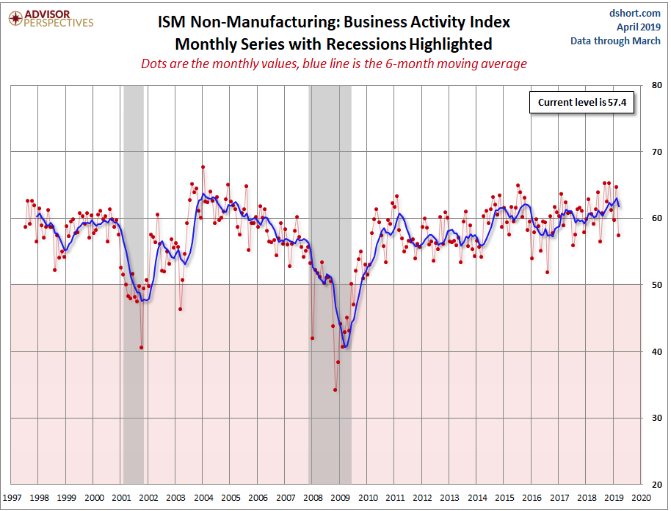

On top of a less than stellar ADP report that underscores the probability of a U.S. economy that is slowing and returning to “trend growth”, the latest ISM nonmanufacturing (service sector) report missed the mark with respect to economists’ expectations. Keep in mind, that the service sector had been running hot throughout 2018.

The ISM non-manufacturing index slipped to 56.1% last month from 59.7% in February, which was among the highest readings in the past decade. The ISM non-manufacturing headline Composite Index only began in 2008 and thus we have little historic data to go on as it pertains to how the Composite Index performs ahead of a recession. With that being said, the most relevant part of the ISM non-manufacturing index is the Business Activity Index portion, which has been around far longer. The latest reading coming in at 57.4% is down 7.3 from a seasonally adjusted 64.7% the previous month.

While both the ADP report and ISM non-manufacturing report throw cold water on some of the better performing segments of the economy from the month of February and March, both are still showing economic growth that is slowing and in keeping with the slowing of the global economy theme.

With an eye and ear on the global economy and geopolitical concerns, Brexit remains a risk to the EU and what fallout may come. The latest headlines do not lend favorably to the region and its trading partners, as an April 12th Brexit deadline looms. The potential for Britain to crash out of the European Union has increased to worrisome levels, said Bank of England Gov. Mark Carney on Wednesday.

“It’s alarmingly high now. We’re in a situation where the expressed will of Parliament is for some form of deal, so to put it in the double negative: Parliament is against no deal. The government, as expressed by the prime minister, is against no deal, the European Union is against no deal, and yet it is a possibility — it is the default option.”

Moreover, while the markets have seemingly brushed aside threats of a no-deal Brexit, the German economy continues with a string of poor economic data results. German factory orders fell 4.2% in February, data showed, marking their sharpest fall since January 2017. The German construction PMI print for March is due to be released later in the morning.

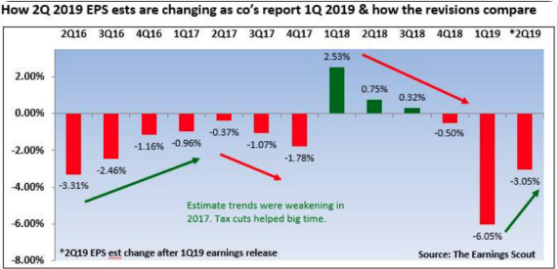

Earnings season is still in the “trickling in” phase and will be until the banks begin reporting in mid-April. Until then, however, some of the results that have been trickling in are less than spectacular, but the guidance for Q2 is also not as poor as it has been for Q1 2019 and with fewer revisions. In other words, estimates for Q2 have fallen much less than Q1 estimates after the first 20 firms have reported results. (See chart below)

Within the chart above, the Q2 revisions were -3.05% which is much better than the 6.05% decline at this point last quarter. The results aren’t as strong as 2018, but those results were spurred by the tax reform enactment.

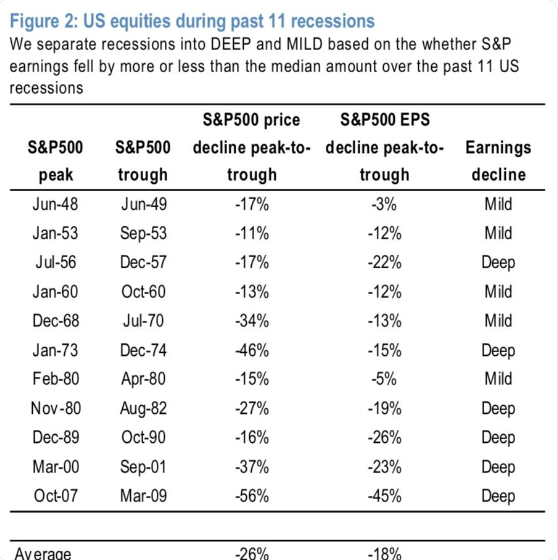

FactSet is currently forecasting an earnings recession in the Q1 2019 period of 3.9% (subject to revisions). Thomson Reuters/Lipper is also forecasting an earnings recession for the same period, but to a lesser degree and with a decline of 1.9% EPS growth. Neither forecast assumes a “deep” earnings recession as characterized historically in the JPM chart below.

Earnings are the key driver of the market over time, but with that being said, the intermediate time frames can find markets whipsawed by headlines that include geopolitics, economic data points and general leveraging/rebalancing exercises amongst portfolio managers and hedge funds alike. Many market participants, investors and traders alike, tend to look forward to hearing what market strategists and analysts say about the future of the market’s trajectory. While Nomura’s Charlie McElligott took a big swing and a miss in March, J.P. Morgan’s quant team, led by Marko Kolanovich has been swinging away since Q4 2018. Back then, he urged clients to stay the course and wade through the market decline as the depth of the decline was more technically and fear-driven than fundamentally driven. To that point, Kolanovich indicated in December 2019 that a market rebound would reshape investor sentiment to align more fundamentally, as sentiment troughs and EPS growth for FY19 is forecasted. And so far Kolanovic’s forecast has been right on target.

Marko Kolanovich, often referred to as “the man who moves markets”, recently updated investors and viewers on CNBC’s Fast Money show Wednesday.

“New highs are ahead for the stock market. It’s possible the S&P 500 could hit his firm’s year-end price target of 3,000 by the end of May. A couple of things would need to happen such as a U.S./China trade deal and a Brexit that is “not too disruptive” or is even pushed back. And of course, if earnings season is not a complete disaster, I think markets will go higher and we could actually see our price target being achieved earlier, maybe even sometime in May or June.”

The stars will need to align favorably around the caveats issued by Kolanovic for sure. A trade deal is the most probable and favorable for the near-term, but Brexit and earnings remain with a degree of doubt. Another piece of kindle to fuel further the S&P 500 rally in 2019 would be re-leveraging. Another factor that could drive the market higher are hedge funds jumping back in, Kolanovic said. Right now, their net exposure to equities is at “all-time lows,” he pointed out.

“The rally so far has been about short covering early in on January, a continuation of buybacks and some of the systematic strategies adding exposure.”

It’s important, as an investor to maintain a disciplined approach when tackling capital allocation. There’s a great deal of information and misinformation offered daily concerning not just individual corporations, but the economy as a whole. Given the size of companies and the economy today, there are many different points of reference and equally numerous opinions on said points of reference. For every piece of good economic data there’s likely a poor performing economic data release.

Media headlines tend to sensationalize the various data and deliver a rational perspective at the same time. It’s a difficult navigation for media outlets and they don’t always get it right. Throughout 2019’s market rally, the FOMC has been the scapegoat for all things favorable or unfavorable with the economy. Kind of a contradiction, but not one that is unique to the time period, as the FOMC is always found to blame and never found for lauding.

Two considerations that still present themself as unresolved for investors, remains the earnings outlook and economic outlook for 2019. With that being said, the FOMC’s dovish stance, with no rate hikes forecast in 2019, has served to add a possible safety net for the economy. Here’s what Finom Group’s chief market strategist has to say in this regard:

“The Fed has been hated since it came into existence, it’s always at fault for recessions and bear markets and yet the economy has done nothing but grow since the Fed came to be in 1933. We’ve got an $18trn economy. If the argument is the debt underlying that economy was partly produced by the Fed, then get out and vote. There’s your problem, government, not the Fed. But I digress…

For all the debate over global PMI’s and stimulus drivers exacting potential economic rebounds if we focus on what’s being done in our domestic economy and if we further focus on what the Fed is doing, if you’re bearish on the outlook then you’re not paying attention to the strength of rates and its rate of change.

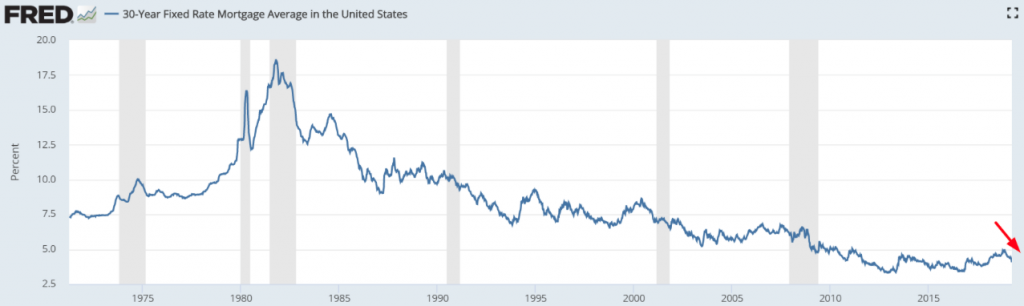

Look at what’s going on in the mortgage markets. We’ve seen a surge, and not a minor one but the equivalent of a Breadth Thrust in mortgage applications. If you were bearish and signaling that the weakness in the housing sector had a pile-on effect back in 2018, how is that the resumption of strength isn’t seen with the same pile-on effect now.

Rates only go in one direction long-term, with the Fed pausing rate hikes until further notice and negative bond yields around the world, where do you think bond investors will go. The U.S. of course! Look at those yields today, look at the 30-year fixed rate mortgage. The Fed knows what it’s doing even if it doesn’t say it very well. Messaging can suck all it wants, but the actions are the key to forecasting the markets and economic slowdown. We’re slowing, certainly we’re slowing! But what’s wrong with trend growth even if it comes with enormous federal deficits and record debt levels if the rest of the world desires that debt above all other. I don’t see anybody stepping up to the plate saying they’re ready to take their sovereign debt medicine today do you? Everyone is morally responsible when it comes to government debt until that government debt has the possibility of knocking at their door.”