April 20, 2020

Bill Miller 1Q 2020 Market Letter

There have been 4 great stock market buying opportunities in my lifetime. The coronavirus has given us the 5th. The first was in 1973-74. The Vietnam War was still underway. Then war broke out in the Middle East in October of 1973. Oil prices soared, inflation hit double digits and so did interest rates. The economy went into recession and a constitutional crisis culminated in the resignation of President Nixon. I was a young first lieutenant in the Army making around $400 per month and putting $25 per month into the Templeton Growth Fund. In the fall of 1974, I went into the Merrill Lynch office in Munich, Germany and bought shares near the market bottom. The second was in the summer of 1982. We had started our value strategy in the spring of 1982 and kept it mostly in cash as the market continued a decline that had begun a year earlier. Mexico then defaulted on its debt, the market fell sharply, and we got fully invested in July. In August, Paul Volcker cut rates and the great bull market was underway. The third was in October of 1987 when the market crashed 22.6% on October 19th, nearly twice the previous biggest single day decline in 1929. We had raised cash in the summer, as the market got very expensive relative to bonds. Stocks peaked in August and began to fall. By the end of September, 30-year bonds yielded over 9%, a cash return roughly equal to the average annual return of stocks since 1926. The market collapsed and we put all of our 25% cash position into stocks. Our value strategy was the single best performing fund of 1988 as most others maintained high cash positions due to fears about the health of the economy. The fourth was 2008-09. We did not navigate that period well. The strategies I then managed all went down much more than the market. We made changes to our positions that we thought would provide the best upside in the inevitable recovery. We stayed fully invested throughout the 10-year bull market and Opportunity Equity was one of the best performing of all US equity strategies since the market low in March 2009 through calendar year 2019.

We have been hit about as hard as anyone in this decline because we have been overweight in higher beta names (i.e., those that are more volatile than the S&P 500) believing (correctly) that since the financial crisis people have been risk- and volatility-phobic and that perceived risk has consistently been greater than real risk. Going into 2020, I thought that economic risk was low and that if the market was going to decline it would be because of either geopolitical events or some exogenous shock to global aggregate demand or aggregate supply. We got that exogenous event in the form of a global pandemic that took stocks from all-time highs to a bear market decline of over 30% in the shortest time in history. As is typical in these sorts of egregious declines, we are down a lot more than the market.

In times such as this, I am reminded of what Keynes wrote to his board when he was managing money during the 1937 market collapse. As you may know, in addition to being the most influential economist of the 20th century, Keynes was also an outstanding investor. The board had been urging him to sell as the market went down and he refused. He told them that it was “the duty of every serious investor to suffer grievous losses with great equanimity.” He went on to note that their advice to increase his selling as stocks went down, if practiced by everyone, would be economically disastrous for the country. It would also mean, he went on to point out, that he would own little or no stock when the market bottomed, whereas his strategy involved being fully invested when stocks were cheap and the market was at its lows.

The market’s behavior since the current low of 2191 on March 23 gives a good indication that this recovery from the inevitable recession now underway will follow the pattern of every other recovery since at least 1973-74. The stocks that have led since the bottom have been low PE/cyclical names with operating or financial leverage, viz., the exact names that were clobbered the most in the decline. Those names were also the worst performers when recession fears were high — fall of 2018, first six weeks of 2016 — yet where no recession materialized. And they gained the most when those fears proved unfounded. The reason why is fairly straightforward: Prices and valuations are highly sensitive to the marginal return on invested capital and to business risk. When the economy is declining, or there are fears that it will, valuations on those companies whose return on invested capital (ROIC) is most sensitive to economic change (mostly traditional cyclicals) will decline more than those that are more resistant such as consumer staples, utilities, bond proxies, and many recurring revenue businesses. Companies with high debt leverage and economic sensitivity fare the worst as the market discounts the possibility they will experience financial distress. When the market sees a recovery, the exact reverse occurs, which is what we saw in the week ending April 10, one of strongest weeks in market history.

It appears that most equity strategists think that the March 23 low may be “retested” in the coming weeks as the global economic shutdown drags on. If so, last week’s leaders, and our Strategies, will also likely lag, although perhaps not as much as they did during the initial collapse. I am agnostic on that as my ability to forecast the market’s short-term path rounds to zero. So does everyone else’s, by the way.

Listening to the financial commentators on CNBC and elsewhere, I hear many, if not most, of them advising investors to use the decline to “upgrade” their portfolios. They say to “buy quality names on sale,” but avoid or reduce exposure to names that are riskier. Typical issues in the quality bucket include companies such as Alphabet, Disney, Nike, Amazon, Facebook, Procter & Gamble, and Clorox. Now these are all very fine companies and we own several of them. I think, though, that a portfolio comprised of all “quality” names, names that have been among the best performers in this dramatic decline, will almost certainly be a portfolio that underperforms the market as the economy and the market recover. In big market declines, the prices of stocks fall more rapidly than long-term business values. We try to use these opportunities to “upgrade” our portfolios as well, by which we mean replace names that have held up reasonably well with those whose price declines now offer much greater long-term upside when the economy comes back.

Sir John Templeton advocated buying at the point of maximum pessimism. The problem is that point is only known in retrospect. There is much pessimism and little optimism evident now, and it is impossible to tell if stocks have declined enough to discount what the future holds with regard to the economic damage that the pandemic will inflict. In October 2008, Warren Buffett wrote an op-edsaying he was buying US stocks and urging others to do so as well. A few years later he was asked how he knew that was the time to buy. He said he did not know the time, but he did know the price at which stocks were a bargain. They were a bargain then and, in my opinion, they are a bargain now, albeit not as great a bargain as they were a few weeks ago. The market may have bottomed at an intraday low of 2191 on March 23 or it may not have. I do believe that shares bought at these prices will prove to be quite rewarding over the next few years, and perhaps a lot sooner. If you missed the other 4 great buying opportunities, the 5th one is now front and center.

Bill Miller, CFA

By Russell Rhoads: APR 20, 2020 11:28AM EDT

There has been nothing normal about 2020 and we are just a bit over 25% of the way through the year. Before the Covid-19 pandemic began to turn our world upside down we got earnings announcements covering 2019 that did not take what was on the horizon into account. In the next couple of weeks many of the biggest components of the Nasdaq-100 will report earnings covering the first three months of 2020. Many market watchers felt like the upcoming earnings season would be a non-event. However, the option market is now bracing for higher individual stock volatility and the Nasdaq-100 is showing a little bump in volatility expectations during the last week of April.

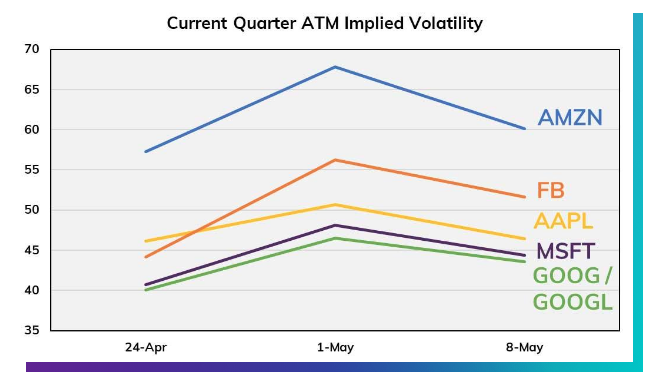

The five largest components of the NDX are Microsoft (MSFT), Apple (AAPL), Amazon (AMZN), Facebook (FB) and Alphabet (GOOG / GOOGL). All five companies are set to report the week ending May 1 and the option market appears to have adjusted in a manner similar to previous earnings seasons.

Using the weekly options expiring April 24, May 1, and May 8, the implied volatility for at-the-money options was determined by averaging the two nearest call and put strikes expiring on each day. As expected in normal times, there is a bump in the implied volatility priced in by the options expiring the Friday after earnings. The implied volatility levels used in the chart below was recorded at midday on Friday April 17.

To get an idea of what the market is expecting out of earnings relative to a more normal time period, the same numbers for each of these companies was used to calculate the same comparison going into earnings three months ago. Unfortunately, GOOG/GOOGL, reported a different week than the other four companies so the various implied volatility charts do not cover the same dates, instead on the Friday two weeks before earnings the at-the-money implied volatility was calculated. This was Jan. 17 for all companies except for Alphabet which was Jan. 24.

The week before implied volatility for all five companies is very low. FB, AAPL, AMZN and MSFT reported their earnings the week after a four-day week which likely put some pressure on the “Week Before” volatility. However, there is no holiday in the mix for the GOOG/GOOGL numbers and that curve is very similar to the other four curves.

Option pricing this quarter is similar to what we expect around earnings with elevated implied volatilities priced in by options that expire just after an earnings announcement. However, this quarter the options expiring the week before earnings have implied volatilities that are more in line with the pricing of options that expire just after earnings. There may be some calendar spread opportunities to take advantage of this unique situation and we will be keeping an eye out for any trades that appear to take advantage of elevated volatility the week before earnings.

Generally broad-based index options do not adjust pricing in anticipation of earnings announcements. However, the five companies that report the same week this quarter represent about 45% of the weighting in the NDX. There is some slight earnings seasonality that shows up in NDX option pricing with slightly elevated implied volatility priced into the non-standard NDX options expiring just after a large portion of the indices’ membership is reporting earnings. This shows up somewhat in the options expiring on May 1 this year.

Both the Friday April 24 and May 1 options are pricing in some elevated volatility expectations. About 10% of the NDX reports the week ending April 24, but near-term market volatility expectations remain elevated as day to day reactions to news continue to be fairly extreme relative to the past few years. The peak on May 1 compares to the final data point (May 8) in a similar manner as the option volatility expectations for the five big NDX companies reporting just before May 1 expiration.

The April 24 and May 1 relationship may offer calendar spread opportunities if there is an expectation that the NDX will continue to experience less extreme day-to-day moves over the course of the week of April 24 and then see a potential pick up in price action associated with earnings announcements. This is something else worth keeping an eye on and any interesting trades will be highlighted in a timely manner.

Nothing about 2020 has been normal and the volatility expectations for both individual stock options as well as broad-based index options continues to be elevated, despite a rebound in stocks and a little less realized volatility. Earnings season is impacting both May 1 individual stock option prices as well as NDX option prices. This higher volatility may offer option traders more alternatives to trade around earnings than in a normal quarter.