Can it do it? Can the markets really shrug off the FOMC rate hike, the ECB’s scheduling of an end to its QE program and the declaration of $50bn in tariffs on Chinese goods? It’s not looking like U.S. equities will perform such a herculean accomplishment at the moment, with futures lower by less than .50% across the major indices.

This morning, President Trump is expected to announce tariffs on Chinese goods worth around $50 billion, Reuters reported. Secretary of State Mike Pompeo is in Beijing to discuss the next steps in getting North Korea to denuclearize. But Reuters, citing an unnamed administration official, said “Trump no longer thought of China’s influence over North Korea as a compelling reason not to impose tariffs now that the United States had a direct line of communication with Pyongyang.”

“China has said that it’s prepared to retaliate should the U.S. proceed with the additional tariffs on Friday. Beijing could back off from an earlier promise to buy more American products including soybeans and natural gas, and announce tariffs against U.S. products that would hit Trump’s key base of political support, said Laura Baughman, president of The Trade Partnership and Trade Partnership Worldwide.”

For much of the year, a trade spat has been developing and now appears to be in full swing. But with a strengthening economy and limited tariffs being announced without details on how the administration plans to implement the tariffs, the total impact on the economy is lacking. Furthermore, in such a tit-for-tat trade war, with the impact being so limited, it is likely to serve minimal purpose…that is, if you’re not the President of the United States. Pushing forward with these tariffs on China allows the President to check a campaign promise box. Given the limited affects of these tariffs, it’s possible that post the implementation, there’s little follow through and interest in waging an all-out trade war. As absurd as suggesting trade deficits are a security risk to the U.S. and as innocuous as these proposed tariffs are on the surface, it begs of the average person to deny the understanding that this is anything more than the art of fulfilling campaign promises more so than “the art of the deal”.

“I think it’s so-called noise,” Frank C.H. Lee, senior investment strategist at DBS Bank in Hong Kong, told CNBC on Friday, stressing that the tariffs are a small percentage of the global giants’ overall annual bilateral trade volume of more than $5 trillion.

The Chinese economy is growing some 6.8 according to its recent reports. It would take even greater imposed tariffs to knock that figure down to possibly 6.6%, hardly anything that would raise concerns in the region. It’s the difference between fear and facts.

So while rates are rising as the FOMC is now expected to raise rates 2 more times in 2018 and the trade spat with China, EU and North American allies is being pushed forward, U.S. equity markets have remained extremely buoyant. Despite the concerns over central bank announcements this week, Finom Group did believe that any pullbacks in the equity markets would present a “buy the dip” opportunity. Here’s what we offered in yesterday’s market outlook report:

“When it’s all said and done, rates rising from where they are today and where the Fed defines the neutral rate remains quite benign with respect to its affect on the economy. As such, any near term pullbacks in the equity market are likely to be viewed as a “buying opportunity”. The Fed has made it a little harder to own stocks, but there’s no need to panic.”

Outside of the geopolitical realm finding headlines this week, yesterday was also highlighted by extremely strong economic data in the way of monthly retail sales. And wow, the data showed just how strong the consumer has been behaving in the Q2 2018 period.

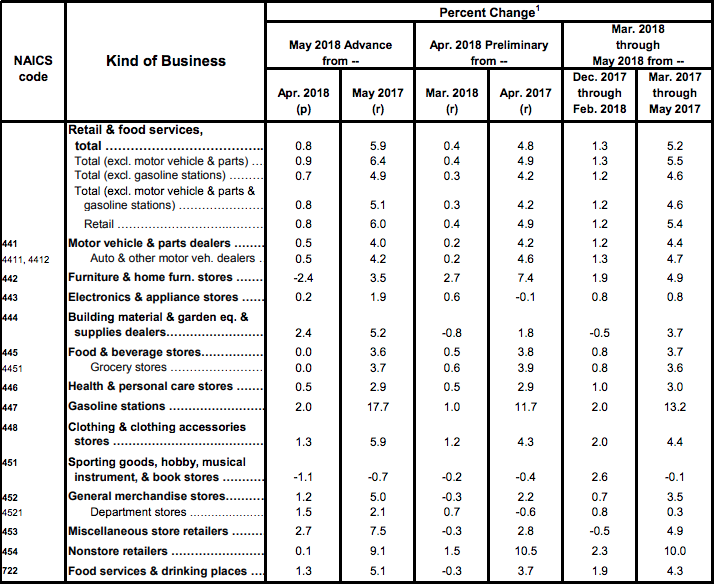

Retail sales jumped by 0.8% in May, twice as high as many economists had forecast. Sales growth in April and March were also revised up sharply, partly reflecting changes in how the government calculates the numbers. Retail sales in April, meanwhile, were raised to show a 0.4% gain from an initial 0.2% reading. Sales in March grew 0.7% instead of being unchanged. Retail sales have risen 5.9% over the past 12 months, the government said Thursday. Sales are rising at a more than 5% yearly pace even if gas is excluded. Below is the categorical breakdown of retail sales on a month-2-month and year-over-year basis.

There were some surprises in the latest bout of retail sales, mainly coming from department store sales. Restaurants and clothing stores posted strong sales, and in a bit of a surprise, traditional brick-and-mortar department stores easily outpaced their Internet rivals. Auto sales also rose 0.5% even the industry reported lower sales figures. Sales fell at stores that sell sporting goods, books, music and home furnishings.

Overall and inclusive of the prior monthly revisions, the latest report on retail sales show just how effective the tax cuts have been and likely point to strong Q2 2018 economic activity. Since the release of the reported retail sales data, economists are now of the opinion that GDP could tip 4% during the 2nd quarter.

CNBC/Moody’s Analytics Rapid GDP Update reported economists’ estimates of tracking GDP show average growth at 3.8 percent, following Thursday’s retail sales report. Their actual forecasts, which take into account economic reports yet to be released, is running at an average 3.6 percent.

JP Morgan’s chief U.S. economist Michael Feroli offered the following notes with regards to the economy and the consumer following yesterday’s economic data:

“On the heels of this data we now estimate real GDP is expanding at a 4.0% annual rate in Q2, up from our prior estimate of 2.75% and almost twice the 2.2% growth rate experienced in Q1,” wrote JP Morgan chief U.S. economist Michael Feroli. If the economy hits that growth rate, it would be the best since the third quarter of 2014.

“The primary source of the acceleration in growth this quarter is the consumer, which looks to be expanding real outlays at a 3.7% rate in Q2 following an anemic 1.0% pace last quarter,” Feroli added. “We had looked for a rebound in Q2, as some temporary drags waned and the tax cut boosted disposable incomes. In any event, consumers wasted no time enjoying their tax windfall, as the Q2 saving rate looks like it will revisit the lows for the cycle.”

Finom Group has believed there would be a more appreciable environment for the retail sector after last year’s exaggerated sector slow down. It had been the main driving force behind our recommendation earlier this year to invest in the Retail Sector Spiders ETF (XRT) as noted below in our e-mail alert to subscribers.

At present and with the current retail sector profit taking at hand, we expect a bit more of a pullback in the sector and individual names to come. Should this outlook become realized, Finom Group would look to redeploy capital in the sector or specific retail names, given the lasting effects from tax cuts that will serve the sector and economy beneficially into 2019. So while the market tonality of the day may prove disappointing in some regards and due to trade spats, it may also provide lasting investor opportunity.

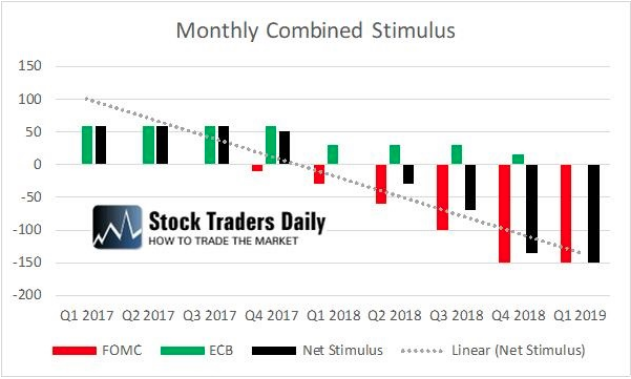

It’s been quite the busy week for headlines and the majority of those headlines surround global central banks. Stimulus officially came to an end in the first quarter of 2018, but after the FOMC and ECB press conferences this week, we know that this combined effort will now become a material drain on liquidity.

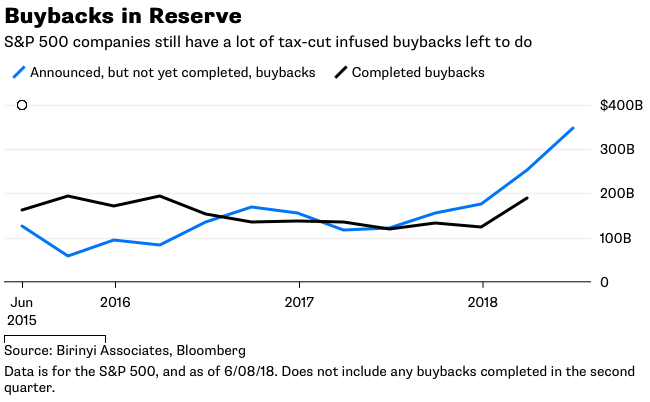

The activity of the central banks to remove liquidity from the financial system has been a longstanding cause for concern. The belief being that central banks boosting liquidity through monetary policies over the last 7-9 years has boosted asset prices, now fosters the belief that removing of such liquidity would reduce asset values. But stimulus by any other name or entity is still stimulus nonetheless. Where the FOMC is draining liquidity/stimulus, the tax cuts and deregulation provide stimulus. It’s the proverbial “fly in the ointment” of bear market participants and even economists who narrowly focus on the central bank influence, blocking out potential offsets. Such stimulus now provided by the U.S. government is serving to not only strengthen the economy, but elongate the economic expansion, serving to further boost asset prices. If we consider more specifically equity prices which follow the path of corporate earnings, we also have to factor in the record level share repurchase programs as boosting earnings and thus boosting asset prices.

While it sounds like there is an “offset” for the FOMC liquidity drain, that doesn’t mean equity markets will realize and rationalize such offsets in equity prices instantly. Sometimes, given the nuances being relatively unique in this economic cycle, the market takes a wait and see approach. What the market/investors are waiting for is results, earnings and the news cycle to turn.

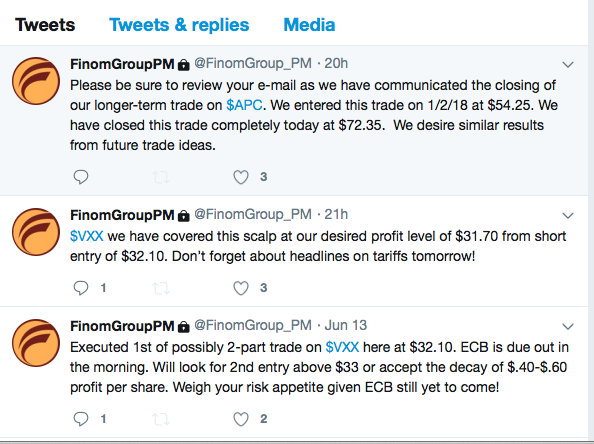

Either way Finom Group’s chief market strategist Seth Golden always suggests to trade what the market gives one to trade. Golden’s outlook for the current trading week was one that suggested bouts of volatility and thus far that’s exactly what we’ve seen: Minor blips in the VIX that ultimately subsided. Such a blip may present itself today, once again. Wednesday’s blip in the VIX turned into another trading opportunity that was delivered to subscribers as depicted in Finom Group’s real time, private Twitter feed.

Finom Group expects to see the market and the VIX express some concerns and indigestion ahead of the tariff announcement and likely through the morning trading hours. Cash may prove advantageous for those seeking to “buy the dip” in the markets. Longer term, the headlines of the day don’t presently change our outlook for the S&P 500 in 2018. Earnings are expected to grow alongside these daily headlines. Under the current forecast for economic growth and corporate earnings, we expect our S&P 50o target of 2,900-3,000 to be hit in the Q4 2018 period.