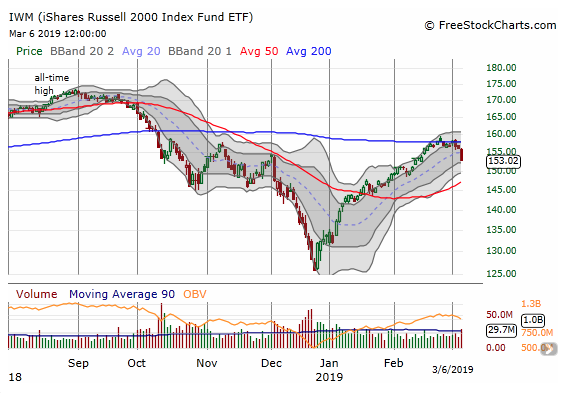

Wall Street is in the midst of shedding some of its overbought conditions that have persisted in the prior two weeks. The major averages have been lower for the totality of the trading week leading up to Thursday. Small Cap stocks expressed the largest decline on Wednesday and post the release of the ADP private payroll data. The Russell 2000 Index fell 2% followed by the Nasdaq (NDX) that fell nearly 1% on the day. The Dow Jones Industrial Average (DJIA) and S&P 500 (SPX) fell a little more than .50% on the day. The selling pressure seems set to resume with equity futures lower ahead of the opening bell Thursday.

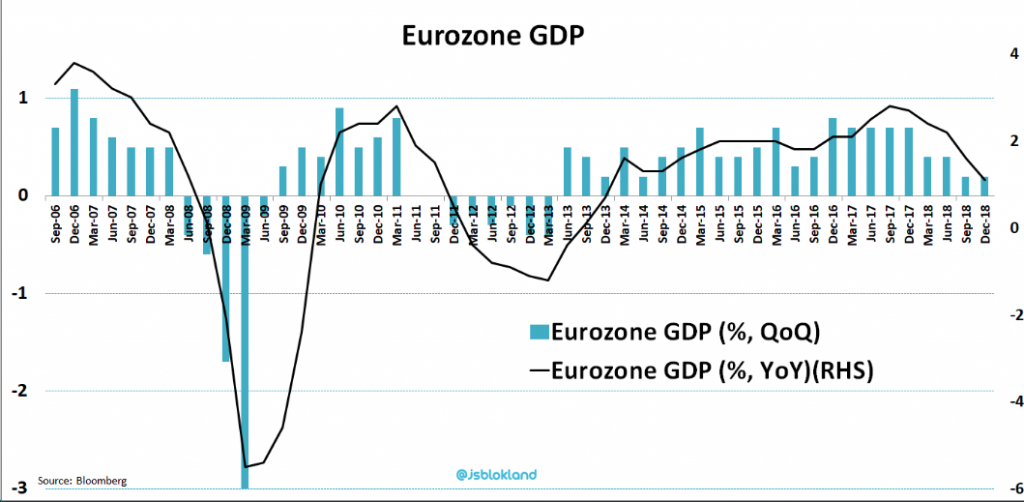

The U.S. equity future weakness mirrors the weakness in European indices and comes ahead of the European Central Bank Meeting this morning. Additionally, headlines surrounding Eurozone economic growth for Q4 2018 are breaking. The Eurozone economy grew 0.2% in the final quarter of 2018. Year-over-year growth has fallen to 1.1%, the slowest pace in five years.

As we revert to the U.S. market conversation and the easing of overbought conditions, we can’t help but realize that Wednesday’s 2% dive in the Russell 2000 found the index breaking below its 200-DMA. Not a good sign!

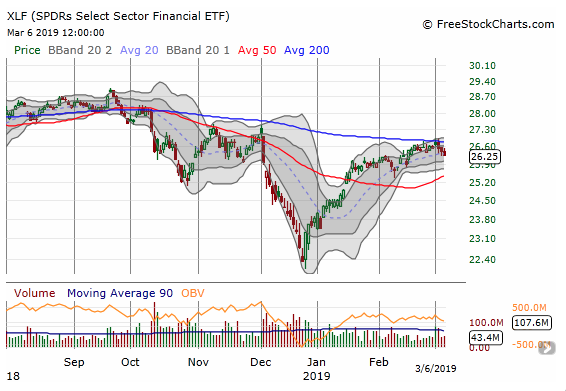

In addition to the Russell’s weakness, the financials have come under pressure. While the financials sector has rallied significantly off its December 2018 lows, it never truly broke-out. As one can see from the chart below, The Financial Select Sector SPDR ETF (XLF) is now breaking its uptrend.

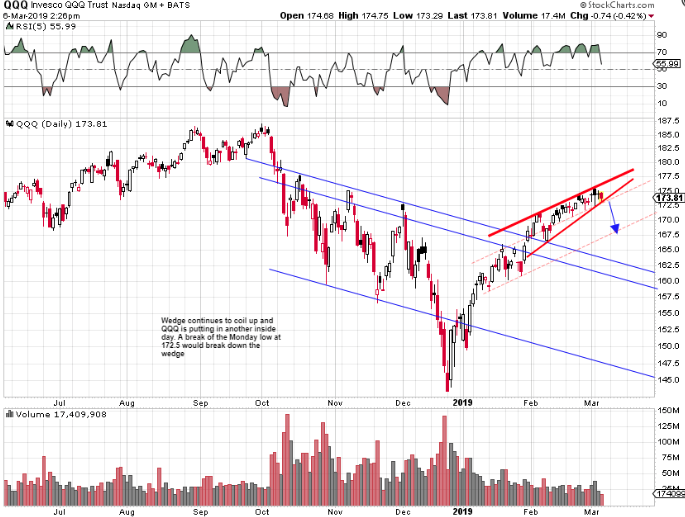

The tech sector heavy Nasdaq has been holding up well and, as usual, has outperformed its peer indices during the 10-week rally. With Facebook (FB) shares also rallying hard of late (last 2-trading sessions), the social media stock still hasn’t proven enough to rally the tech sector as a whole. Tech stocks are holding up relative to the S&P 500 or even the Russell 2000, but the rising wedge that’s been coiling up for a month now suggests it may not last, says Adam Mancini, a full-time trader closely followed on Twitter. Mancini offers the following chart that indicates a possible decline is ahead for the tech sector ETF (QQQ).

“The tightening price action combined with declining volume is an attractive setup for a drop to 167 – trigger would be a break of 172.5.”

Alongside the markets working off some of their respective overbought conditions, volatility is making a comeback. While the VIX doesn’t lend itself to predictive or actionable technical analysis, it is somewhat useful as an indication of market hedging activity that can be applied for long portfolio managers. With that being said, with yesterday’s sharp rally, the VIX is back over the 20-Day SMA for first time since December 2018.

In addition to the VIX breaking above its 20-DMA recently, Monday marked only the 2nd time ever that the VIX had its low penetrate the lower Bollinger Band and its high break above its upper Bollinger Band on the same day. When combined we believe the market is uncertain of the next leg higher or lower and that uncertainty is cause for increased hedging activity, finding a more positive SPX-VIX relationship when the two indexes tend to have an inverse correlation. As such, the VIX may be signaling greater volatility is ahead, with the fear gauge possibly pointing toward 19 near-term. But as we’ve seen before, a big Nonfarm Payroll number can settle investor fears and find short-term forecasting with greater error than efficacy.

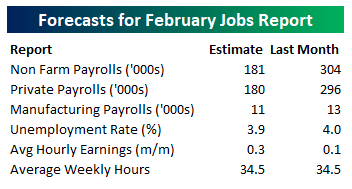

Speaking of economic data, heading into Friday’s Non-Farm Payrolls (NFP) report for February, economists are expecting an increase in payrolls of 181K, which would be a decline from January’s monster report which came in above expectations at 304K. Below is a table from Bespoke Investment Group that offers both the previous NFP results and the estimates for this Friday’s release.

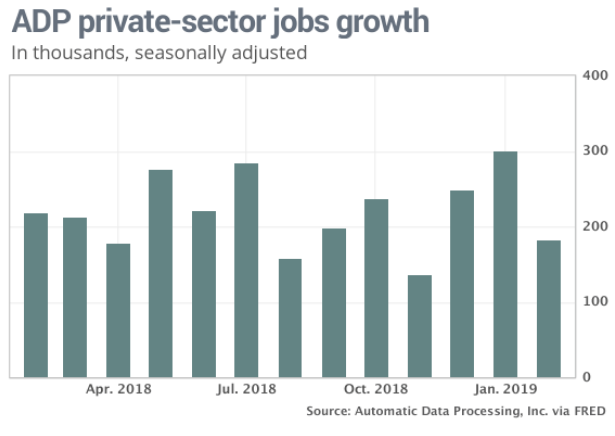

The preview to the NFP release comes by way of the ADP private sector payroll report, which was released Wednesday. Private-sector employment has “throttled back” in February, according to the economist who prepared the data released Wednesday. Employers added 183,000 jobs in February, compared with a revised 300,000 in January, ADP reported. The gain in February was close to forecasts from economists who expected a gain of 180,000.

“Job gains are still strong, but they have likely seen their high-water mark for this expansion,” said Mark Zandi, chief economist at Moody’s Analytics, in a statement. In an interview on CNBC, Zandi said he now sees gross domestic product running at a 0.3% annual rate in the first quarter, much slower than the 2.6% rate reported for the final three months of last year. This slowdown “will start to show in payroll data.

The economy has throttled back, and so too has job growth,” Mark Zandi, chief economist at Moody’s Analytics, said in a statement. “Job gains are still strong, but they have likely seen their high watermark for this expansion.”

In addition to the economic data that continues to roll in daily, the Fed’s Beige Book was released on Wednesday. Ten of the Federal Reserve’s 12 districts saw “slight-to-moderate” growth in late January and February, while St. Louis and Philadelphia reported “flat economic conditions,” according to the Fed’s Beige Book report released Wednesday.

The partial government shutdown led to slower activity in about six Fed districts. The impact hit a wide range of sectors, including retail, auto sales, tourism, real estate, restaurants, manufacturing and staffing services. Consumer spending was “mixed” and several districts said retail and auto sales were lower due to harsh winter weather and higher costs of credit.

Manufacturing activity strengthened but firms conveyed a wall of worry about weakening global demand, higher costs due to tariffs, and ongoing trade policy uncertainty.

With the Fed’s Beige Book released, Fed speakers carried forward with their individual speeches and messaging on Wednesday. In a speech to the Economic Club of New York, New York Fed President John Williams said the economy is currently “about as good as it gets: very low unemployment, sustainable growth and inflation just about at our 2% goal.”

“Given this favorable situation, when you look at monetary policy, things are looking pretty normal as well,” said Williams, who is the only regional president that gets a vote at all Federal Open Market Committee meetings. My current estimate for r-star is 0.5%, so when you adjust for inflation that’s near 2%, the current federal funds rate of 2.4% puts us right at neutral.”

In his speech, Williams said he expected the economy to slow “considerably” this year to a 2% annual growth rate, close to the Fed’s estimate of the trend rate of growth. This is in line with projections of other top Fed officials.

“I’ve said it before and no doubt, I’ll say it as long as I work for a central bank. But in the current conditions the phrase takes on even more importance. Our response will always be ‘data dependent. We can afford to be flexible and wait for the data to guide our approach.”

The market is teetering, that’s probably the best way to describe present market conditions, sentiment and trend. The trend could breakdown, find stability and malaise or it could slowly track higher until Q1 earnings season. We’d be of the opinion, that a limited breakdown is the more probable outcome for a variety of reasons. One of the main reasons is something that we wrote about on Monday and centers on CTA positioning.

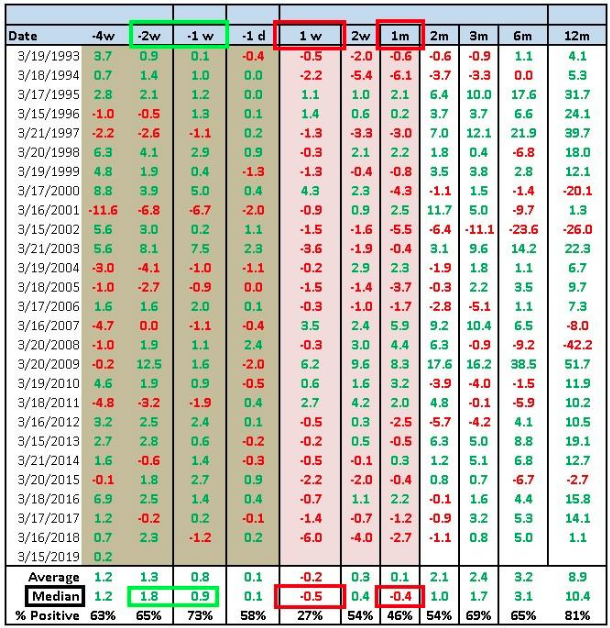

The punch line for a potential “Ides of March” moment is this: if we see the seasonal post-serial options expiration / quad-witch rally-then-pullback phenomenon occur (as has been the median outcome over the past 25 years), which this year could look even more exaggerated on account of the extreme $Delta / $Gamma currently seen in SPX / SPY / QQQ (Consolidated SPX / SPY $Delta is currently 96th %ile and crowded “Growth” proxy QQQ $Delta is currently 97th %ile while $Gamma is 89th %ile), it would then converge with the “demand vacuum” of the onset of the “corporate blackout” window (75% into blackout by 3/19/19) at the same time alongside a mechanically-driver “higher sell pivot” levels in the 1Y CTA model for both SPX and NDX which could potentially dictate outright SELL flows—thus, we could have the makings of a “March Surprise.”

The specific SPX seasonal pattern over the past 25 years surrounding the March serial options expiration, or the “trade up” into, “trade down” out of pattern, is shown below:

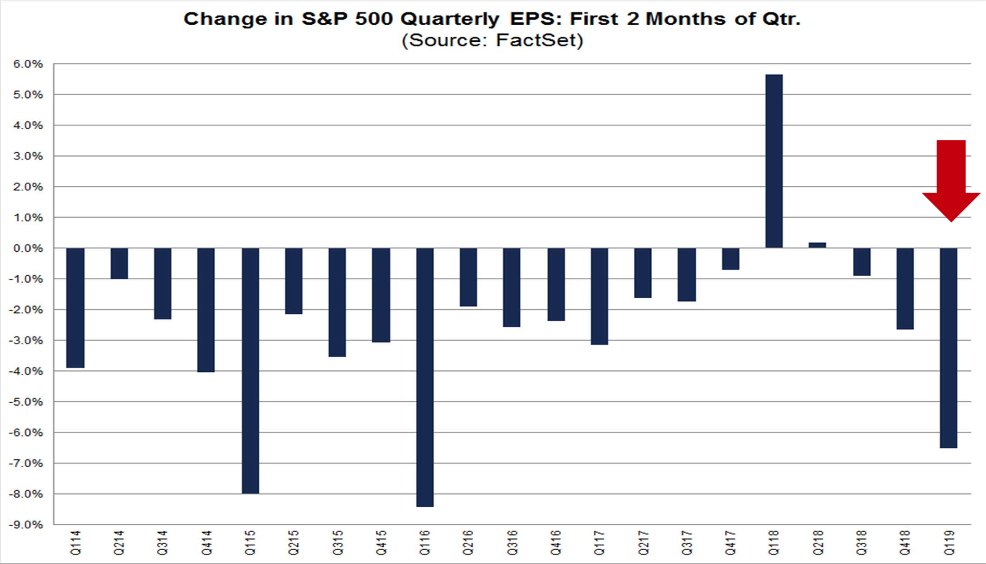

Additionally, markets like a pause that refreshes, especially one that finds the current valuation possibly stretched. The forward 12-month P/E ratio for the S&P 500 is 16.2. This P/E ratio is below the 5-year average (16.4) but above the 10-year average (14.7). We only suggest the valuation might prove a bit stretched with respect to the change in Q1 2019 quarterly EPS estimates. (See Chart below from FactSet Data)

The argument could be made that at present levels there simply isn’t reason enough to buy the market up. With recent GDP results from the Eurozone, the recent lowered GDP outlook from China concerning its economy and the likelihood of a U.S. economic slowdown expected in 2019, investors may find themselves in a holding period ahead of Q1 2019 corporate earnings results. That likely leaves the biggest buyer of U.S. equities being corporate share repurchase programs. Now is likely a better time to create a shopping list of equities/ETFs that one would like to acquire over the next 30-60 days while reflecting on a spectacular 10-year market rally.

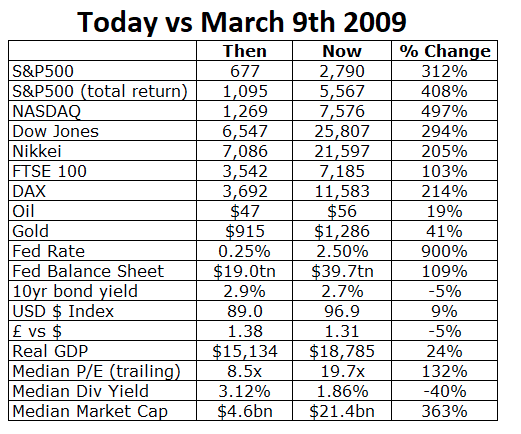

It’s been exactly a decade since the low set on Mar 6, 2009. Let’s look at what’s changed since then! We can recall when QE first began it was assumed to create inflation in the economy. With that said, check out the “then and now” with regards to the 10-year Treasury Yield.

Stay tuned for our latest State of the Markets (SOTM). Our subscribers will be able to review the video this evening and our visitors will be able to review it tomorrow morning. In addition to our weekly SOTM, please review our daily Technical Market Recap with Wayne Wilson.

Our Premium Members are also welcome to visit our Trading Room, newly opened this week and moderated.