Heading into Thursday’s market open on Wall Street we’ve got some good news and some bad news. Firstly, the bad news: U.S. equity futures are down across the board by roughly .5% in the 5:00 a.m. EST hour. Crude oil popped above $52 a barrel on Wednesday, but supply/output was higher than expected and the price/barrel is again lower in the early trading hours on Thursday. Adding to the pressure on U.S. equity futures we have all European indices lower on the heels of more bad economic data from China’s economy.

European equity declines came after official Chinese inflation data for December came in below expectations. China’s December consumer inflation (CPI) rose 1.9% on year. That was lower than economists’ expectations of a 2.1% growth, according to a Reuters’ poll. Producer inflation rose 0.9% on-year in December, which was lower than the 1.6% economists were expecting. The latest inflation figures came on the back of poorer-than-expected Chinese manufacturing data for December.

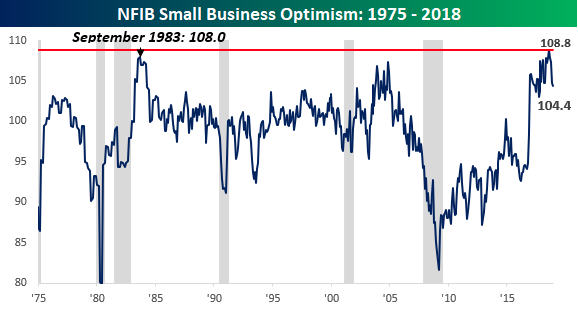

U.S. economic data and business sentiment has been weakening of late in some regard and strengthening in others, like the labor and employment market. But as it pertains to sentiment, there is more lacking than finding favor. Small business sentiment for the month of December was released earlier this week and showed a smaller than expected decline falling from 104.8 down to 104.0 versus expectations for a decline to 103.0. While the decline wasn’t as large as expected, since peaking four months ago in August, small business sentiment has now dropped in each of the last four months for its largest four-month decline since December 2012. That’s not a trend we like to see and it’s likely tied to issues surrounding the global economic slowdown and domestic political strife.

Although the overall decline in small business sentiment was the fourth in a row, the small-business lobby group continues to paint a positive picture of the overall business environment. “Actual hiring strengthened to the highest reading in six months, job openings are at a record high levels, and plans to create new jobs are down only three points from August’s record high,” NFIB said in a release.

Meanwhile, the group said, gauges of business conditions and whether it’s a good time to expand “have both tapered off since the record high index reading in August but still remain well above their historical averages.”

On a lighter note, the S&P 500 hadn’t had a 4-day win streak in nearly four months (78 trading days)… until yesterday’s positive close of course. With Wednesday’s 10-point climb for the S&P 500, the drought ended. However, the recent drought of expressing a 4-day win streak was the longest streak without a 4-day win streak for the benchmark index since the U.S. election in Nov ’16 (83 days). Additionally, with Thursday’s move higher, the S&P 500 completed the weekly expected move of $60 as it touched above 2,591 intraday.

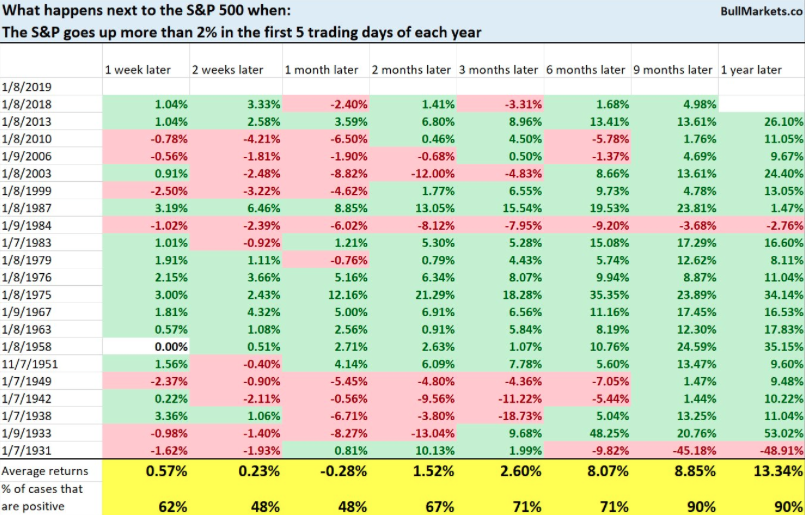

Here’s some more food for thought for the bulls out there. We’ve all heard of the January barometer for the market right? That basically is the foreshadowing of the full year market performance as gauged by the first 5 trading days of January. With the S&P 500 up roughly 3% already in 2019 here’s a study from Troy Bombardia that is based on the January barometer and bodes well for the bulls. Here’s what happened next to the S&P 500 when it went up more than 2% in the first 5 trading days of each year.

Now, we have to recognize that the current economic cycle and bull market are unlike that of any of their predecessors. Nonetheless, 9-12 months later, as shown in the table, the S&P 500 is up 90% of the time. That’s a pretty strong, historic trend.

As it pertains to what may or may not align with the January effect, it’s going to take some easing of domestic political issues i.e. government shutdown ending and global trade feuds easing. On the trade feud front, trade talks/negotiations seem to be moving progressively forward between the U.S. and China. In a Thursday morning statement, China’s Commerce Ministry said the just-concluded round of trade talks with the U.S. were extensive and established a foundation for the resolution of each others’ concerns.

“From Jan. 7 to 9, China and the U.S. held discussions in Beijing at a vice-ministerial level over the issue of trade. Both sides enthusiastically implemented the important agreement of the heads of both countries, and held broad, deep and meticulous discussions on shared observations on trade issues and structural problems, laying the foundation for addressing areas of common concern. Both sides agreed to continue to keep in close contact.”

Gao Feng, a spokesman for China’s Commerce Ministry, said Thursday afternoon that the length of the meeting indicated that both sides were serious and honest. He added that the structural issues that made progress during the talks included forced tech transfers and the protection of intellectual property rights.

The opening up of the Chinese market and IP protection installations have been top list priorities in the negotiations for the U.S. officials and White House Administration. On the surface and based on the released statements from the concluded meetings, it seems as though both parties are on a path toward a mutual agreement and concessions.

“There were several signs of modest progress from these mid-level talks. First, negotiations went a day over the original schedule, indicating enough substantive discussion to at least keep officials at the table. Day three reportedly focused on the more knotty structural issues raised by the US side in detailed demands presented to Beijing in May 2018,” a group of experts from political risk consultancy Eurasia Group wrote in a Wednesday note.”

We have a very binary market presently and the 2019 outcome for the market is likely very dependent on the macro picture. Earnings and the multiple investors place on those earnings are going to be dependent on a couple of issues finding resolution. Finom Group dove into the main 2 issues we believe will guide the global economy in 2019.

- Global trade feuds easing with mutual resolutions

- Central Banks, largely the FOMC, move into and maintain a more dovish stance.

On both of these key issues we are seeing positive movement, as the FOMC turned more dovish and insists it can be patient with regards to future rate hikes. The latest release of the FOMC meeting minutes indicated as such.

Minutes released Wednesday from the FOMC meeting in December showed the rate hike came with reluctance from a few members who thought the lack of inflationary pressures argued against another increase. The minutes noted that the low-inflationary backdrop means the Fed can “afford to be patient about further policy firming.”

“With an increase in the target range at this meeting, the federal funds rate would be at or close to the lower end of the range of estimates of the longer-run neutral interest rate, and participants expressed that recent developments, including the volatility in financial markets and the increased concerns about global growth, made the appropriate extent and timing of future policy firming less clear than earlier.”

It appears very much that the FOMC will not be hiking rates any time soon or at least any time in the first half of 2019. Other analysts and talking heads believe this to be the case as well. In the most recent commentary on the subject matter of market headwinds for 2019, here is what CNBC’s Mad Money host Jim Cramer had to say:

“If you believe the trade war will simmer down, if you believe Fed Chief Jay Powell will hold off on raising interest rates — that he’ll make decisions based on the actual data last week — then the worldwide economic expansion can restart.”

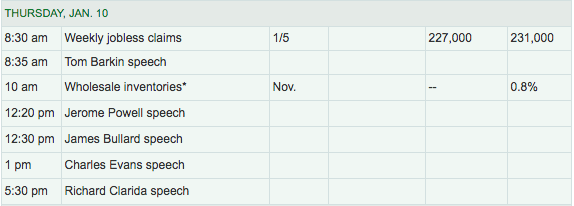

On Thursday, the markets won’t contend with much in the way of economic data, as Initial Jobless Claims are the only piece of key data on the docket set to be released.

As shown in the table above, however, Fed speeches and Q&A sessions are in abundance. Investors may turn their attention to a Q&A session with Federal Reserve Chairman Jerome Powell and Economic Club of Washington President David Rubenstein on Thursday afternoon. Now let’s take a gander, more specifically at where we are in the S&P 500 as the macro picture develops around it.

As Finom Group mentioned ahead of the weekly market trading, the S&P 500 was very likely to trade back up to it’s recent support level of 2,575-2,581 (February 2018 closing low). It did exactly that.

Back in December of 2018, that support level broke and found the S&P 500 cascading lower and through the Christmas Eve trading day. What was formerly support, in technical terminology and analysis, has now become resistance. While the S&P 500 certainly closed above the 2,581 level on Wednesday, we’d like to see a weekly close above this resistance level; that would be far more bullish. Additionally, we’d like to see volume ascending rather than descending, as it has been during this reflex rally in the market.

While market volatility, as gauged by the VIX, has come in from it’s recent highs above 36, the VIX remains elevated at nearly 21 going into Thursday’s trading activity. A VIX reading of 21 insinuates or implies a daily SPX move of roughly 1.3% intraday move. Investors can rationalize that volatility still remains problematic for investors, but to a lesser degree than in December 2018. Speaking more specifically to market volatility and the recent decline in the VIX, the VIX did something recently that it had only done one other time in its history. With Wednesday’s VIX dip below 20, it went from a close over 35.00 to a close under 20.00 within 10 trading days. Remarkable!

In the chart above, identifying the one other time this occurred, Odd Stats charted how the S&P 500 performed over the next month when the VIX went from a close over 35 to a close under 20 within 10 trading days. Obviously, the chart shows a positive 30-day performance for the S&P 500. “Oddly” enough you don’t have to travel back too far in history to find the only other occurrence, February-March of 2018.

While Finom Group believes a pullback from the recent reflex rally in the markets is a high probability (for which we be happy to be proven wrong), it remains to be seen. The government remains shutdown and if it runs through this Saturday it will be the longest government shutdown in U.S. history. Nonetheless, Federated Investor’s top market watcher says that he expects markets to be choppy near term with possible S&P 500 resistance at 2,600 and a retest of the 2,350 lows.

“If the Fed seems to be in place, if we can get this China trade situation resolved, and if we can get some clarity in terms of what’s going on in Europe, then I think we could be off to the races in the back nine months of the year,” said Orlando, who believes the issues will be successfully resolved.”

Stay tuned to Finom Group’s latest State of the Market video, which will be published Friday! Subscribe to Finom Group to access our weekly research reports and trade alerts!