Back when I was in high school, oh soooo many years ago, a top-10 rap song by Ice Cube was popular. The title of the song was “Today was a good day”. What made the song so popular was the melody and the opening verse: Just waking up in the morning gotta thank God, I don’t know but today seems kinda odd.”

That must be what investors around the world are feeling and thinking given the promising headlines reported by several sources on the trade war between the U.S. and China.

“President Donald Trump wants to reach an agreement on trade with Chinese President Xi Jinping at the Group of 20 nations summit in Argentina later this month and has asked key U.S. officials to begin drafting potential terms, according to four people familiar with the matter.

The push for a possible deal with China was prompted by the president’s telephone call with Xi on Thursday, the people said, requesting anonymity to discuss internal deliberations. Afterward, Trump described the conversation as “long and very good” and said in a tweet that their discussions on trade were “moving along nicely.”

Given the remarkable change in tone and activities by the U.S. administration on trade over the last 24 hours, global trading partners, investors and economists must be looking to the heavens. For much of 2018, the escalation of the trade feud between the U.S. and China has remained on a seemingly untenable path that would ultimately end in a full-scale trade war. Over the last 24 hours or so, however, President Donald Trump has given the world reason to believe a trade deal is more possible and probable in the near future. Given months and months of animosity pointed at China’s trade practices by President Trump and the administration, I don’t know, but today seems kinda odd, does it not? And with headlines surrounding the positive developments on trade, equity futures are shrugging off a subdued forecast issued by Apple Inc. (AAPL) last night in favor of trade headlines. Global equities are on the rise with U.S. futures sharply higher in the wee morning hours.

The news prompted stocks to surge in Hong Kong and China, while the offshore yuan jumped as much as 0.31% before paring gains to trade 0.26% higher. The Hang Seng Index rose as much as 4%, headed for its biggest gain since 2015, and the Shanghai Composite Index climbed more than 2%, on track for a fourth day of gains for its longest winning streak since February.

Backtracking to U.S. markets and the economic data on Thursday and ahead of Friday’s key economic data to be released, U.S. equities finished sharply higher for a 3rd consecutive trading day. The Dow Jones Industrial Average (DJIA) and S&P 500 (SPX) were a perfect mirror of performance as they both rose 1.06% on the trading day. The tech-heavy Nasdaq (NDX) was the clear outperformer, up roughly 1.75% on the trading day in anticipation of Apple Inc. earnings after the closing bell. The economic data on Thursday showed, in many respects, that the U.S. economy remained on strong footing.

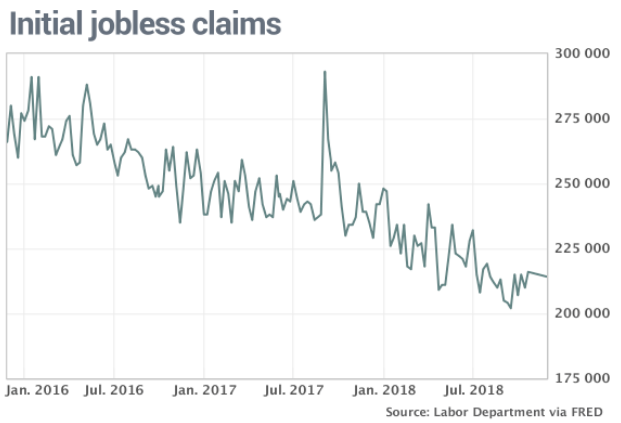

Initial jobless claims, a rough way to measure layoffs, fell by 2,000 to 214,000 in the seven days ended Oct. 27, the government said Thursday.

New jobless claims have totaled fewer than 220,000 since July, an incredibly low number that reflects the healthiest labor market since the late 1990s and perhaps as far back as the early 1970s, depending on which government measure is given more emphasis. Despite the duration of the current economic expansion, spanning some 9 years now, the strength of the labor market looks to prolong the expansion into at least 2019. With more Americans working and incomes rising, households are able to spend enough to keep the economy moving forward at a healthy pace, as demonstrated in the latest GDP results. The government outlined last week that U.S. GDP grew 3.5% in the Q3 2018 period.

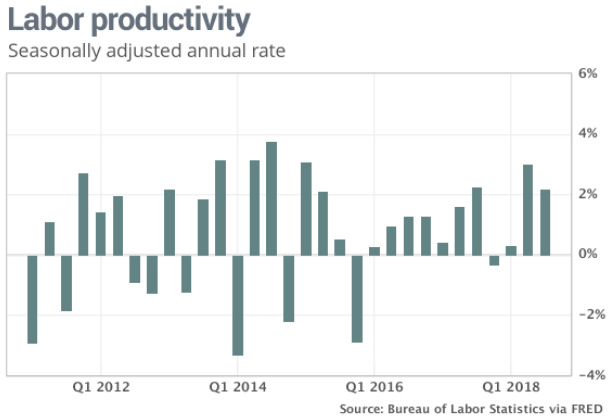

The exhaustive headwind that has been global trade disputes has only been trumped by fears of rising inflation in 2018. With the Fed raising rates, most short and long-end bonds have been on the rising, pushing up bond yields, core CPI and more obviously as it pertains to housing, mortgage rates. As such, it has been a welcome sight in both the Q2 period and Q3 period to see back-to-back productivity gains in the United States.

U.S. productivity rose at 2.2% annual pace in the third quarter after a strong gain in the spring, marking the best back-to-back performance in four years in a good sign for the economy. Companies increased the amount of goods and services they produced, known as output, by 4.1% in the three months stretching from July to September. The hours workers spent on the job rose by a smaller 1.8%, the government said Thursday. Productivity also rose at a revised 3% annual rate in the second quarter. Rising productivity in the long run is the key to a higher standard of living according to many economists and analysts. Hourly compensation rose 3.5% in the third quarter, but just 1.4% once inflation is taken into account.

The bottom line when it comes to productivity is that when workers produce more in the same amount of time, companies can boost wages and maintain healthy profits. Higher productivity also keeps inflation in check. Once again, higher productivity keeps inflation in check. Something permabears don’t frequently want or enable themselves to acknowledge.

“The quarterly gain in productivity kept the year-on-year pace at 1.3% in the third quarter, still a tepid rate by historical standards but today’s encouraging report indicates that the recovery in productivity continues, economists at Oxford Economics wrote in a note to clients.”

Speaking of mortgage rates, the 30-year fixed-rate mortgage averaged 4.83% in the Nov.1 week, down 3 basis points, mortgage finance provider Freddie Mac said Thursday. The 15-year fixed-rate mortgage averaged 4.23%, down from 4.29%. The 5-year Treasury-indexed hybrid adjustable-rate mortgage averaged 4.04%, a 10-basis point drop.

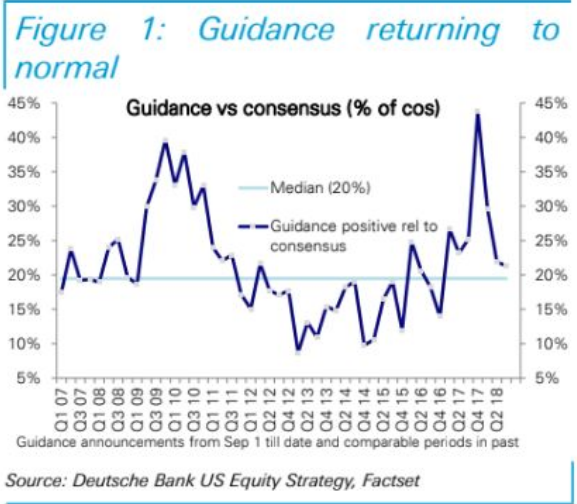

The recent “bounce of the bottom” for equities has been a welcome sight for investors. Much of October’s swoon has given birth to a more pessimistic outlook for equities through year-end, but some of that pessimism has been offset by optimism in recent days and as the S&P has recovered somewhat. The optimism in the last few trading days is being mirrored in Binky Chadha, chief U.S. equity & global strategist at Deutsche Bank, recent notes to clients whereby he addresses the mood of investors. Chadha suggests investors should chill because we are just returning to earnings normality.

The analyst says the fact is that results are returning to historical norms; and as a result, may be lower than in recent quarters, but are still higher than the historical average.

“We see this reversion to normal as typical following unexpected accelerations in growth (such as those coming out of recessions and shocks including the effects of the recent cut in the corporate tax rate.

Corporate margins are climbing to records and adjusted margins are holding steady, and a strong pace of buybacks looks set to carry on.”

Also Heading into November, J.P. Morgan’s chart analyst says if the S&P 500 can consistently stay above a key level, the market has a shot of recovering last month’s losses.

“After a couple failed attempts to rebound from a bullishly developing technical setup last week, this week’s move tentatively has more staying power,” J.P. Morgan technical market strategist Jason Hunter said in a note to clients Thursday. “The technical pieces that helped identify bullish reversals after past late-cycle corrections are all present. We feel strongly that this is a late-cycle correction and not the start of a protracted bear market.

Sustained closes in S&P 500 above the 2,700 area “would add conviction to the medium-term outlook. Should this occur, we’re predicting that the market will “break to new highs into early 2019.”

Now let’s get into the earnings releases after the closing bell on Wall Street Thursday. First up is Starbucks (SBUX). Why, because I own shares of SBUX in the Golden Capital Portfolio and we have it as one of our top picks for 2018.

We didn’t expect wild outperformance from the brand in 2018, but believed tough comps would regulate the stock through much of the year and provide investors with a safe standard of performance once expectations had been reset. It was a comfort stock play so to speak. Moreover, investors get paid to wait with a reasonable dividend and increasing buybacks that have been outlined in 2018.

Starbucks’ revenue hit a fresh record of $6.3 billion, up 10.6 percent from $5.7 billion during the same time last year. Here’s what the company reported compared with what Wall Street was expecting, based on a survey of analysts by Refinitiv:

- Adjusted earnings per share: 62 cents vs. 60 cents

- Revenue: $6.3 billion vs. $6.27 billion

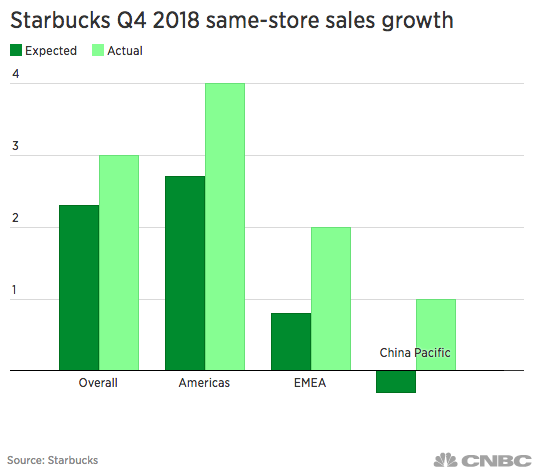

- Global same-store sales: 3 percent vs. 2.3 percent

In the fourth quarter, Starbucks posted better-than-expected same-store sales across all four of its major markets. Global same-store sales during the fiscal fourth quarter rose 3%, up from the 2.3% analysts had expected according to Refinitiv.

After adjusting for some one-time items, the company earned 62 cents a share while analysts expected 60 cents a share. Starbucks said its loyalty program, which accounts for 14% of all its transactions, now has 15.3 million members, a 15% jump from last year. Starbucks Rewards members drove nearly 40% of sales in the United States. As it pertains to the coffee service giants outlook…

2019 outlook. Here’s what Starbucks expects:

- To add around 2,100 net new Starbucks stores globally

- Same-store sales growth near the lower end of its current 3 to 5 percent range

- Consolidated revenue growth of 5 to 7 percent

- Adjusted earnings per share in the range of $2.61 to $2.66

Now let’s get into the Apple Inc. earnings report which seemingly was met with investor disappointment. Shares of AAPL fell sharply in the after hours trading session Thursday and as the company announced it would no longer break out individual unit sales results.

For the quarter, Apple posted iPhone unit sales that were flat YOY, extending the trend of very modest growth it’s seen in recent quarters. To compensate, Apple has increased the price of the iPhone, boosting its ASP and overall profit.

The company reported an ASP of $793, a YOY increase of 28% and well above analyst projections of $750.78, based on FactSet and StreetAccount estimates.

The company reported Services revenue of $9.98 billion. That’s an increase of 27%, accounting for a one-time adjustment in the year-ago period, but just below Wall Street estimates of $10.2 billion, according to FactSet and StreetAccount estimates.

Apple’s Other Product revenue, which includes sales from gadgets like HomePods, AirPods and Apple Watches, rang in at $4.23 billion, an increase of 31% year-over-year. Here’s how Apple did in other key product segments:

- iPad: 9.7 million units and $4.09 billion in revenue

- Mac: 5.3 million units and $7.41 billion in revenue

On a regional basis, Apple Inc. reported double-digit, YOY revenue growth in all geographic regions, led by a 34% revenue upside in Japan and a 22% revenue upside in the rest of Asia Pacific. In the following video, Loup Ventures analyst Gene Munster discusses his thoughts on the Apple Inc. Q4 earnings report. He believes despite the early reaction to Apple Inc.’s reporting metrics and Q1 2019 guidance, investors and analysts will find results and actions around discontinuing reporting individual product unit sales favorable in the future.

Apple’s forecast for the December period calls for revenue of $89 billion to $93 billion. Those are staggering numbers that would beat Apple’s quarterly record of $88.5 billion set last year in the holiday quarter. But it also represents sales growth of less than 5% from that performance last year, when the $1,000 iPhone X helped juice sales.

While the early reaction to Apple’s latest metric results hasn’t born fruits in the way of share price appreciation, I believe long-term share price appreciation is probable. Given this sentiment and the discounted share price action on Thursday and into Friday’s trading session, I acquired shares of AAPL.

With a 6-12 month outlook, I believe the present pullback in shares of AAPL warrants investor exposure. For more details on all Finom Group’s trade alerts and long-term market outlook, subscribe today! Now let’s take a look at what’s ahead.

If it’s the first Friday of a new month that means it’s jobs Friday. At 8:30 a.m. EST, the government will release the latest labor market data in the way of Nonfarm Payrolls. Economists expect the headline jobless rate to hold at 3.7 percent, a near 50-year low. Total nonfarm payroll growth is projected at 190,000, after September’s disappointing 134,000.

The positive headlines surrounding trade are providing further optimism in global equity markets prior to the opening bell on Wall Street. Regardless of how or what develops in the market on any given trading day, Finom Group will be looking for ways to capture the volatile moves in the market. On Thursday, the market proved to deliver further trading opportunities as identified in our trade alerts noted below, which we captured.

Have a great trading day and do subscribe today for access to our weekly research report delivered each and every Sunday morning to subscribers.