After a bond market panic that pervaded equity markets on Friday, the rather flat performance for U.S. equity markets on Monday was a welcome site to many on Wall Street. The Dow Jones Industrial Average (DJIA) finished slightly higher on Monday while the S&P 500 (SPX) and Nasdaq (NDX) finished slightly lower on the day. The pressure on bond yields continued Monday also and with the 3-mont/10-yr. Treasury remaining further inverted. More importantly and with no stress being indicated in the credit markets, the 2-yr/10-yr Treasury spread widened from 12 bps to 15.5 bps Monday.

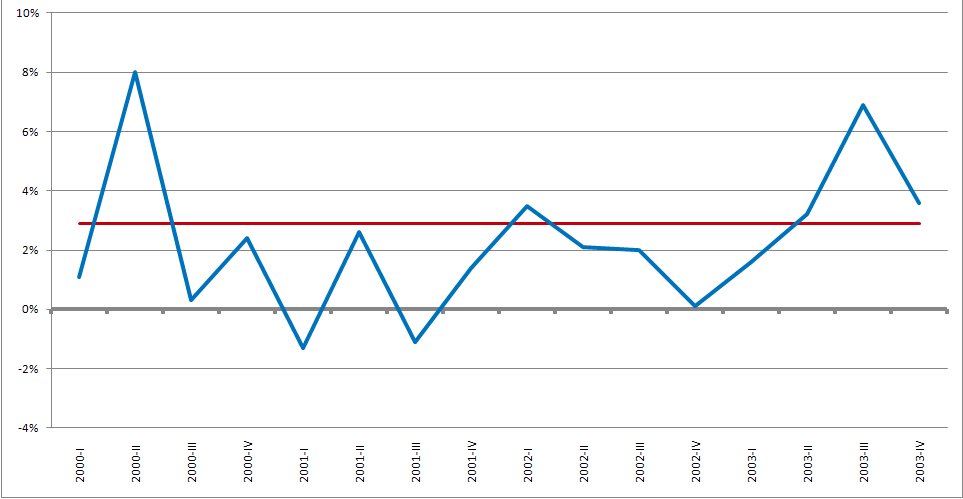

The narrative that continues to grab headlines since the front end of the bond yield curve has inverted suggests that every time the 3-month/10-yr Treasury yields invert, a recession occurs on average within 19 months. The reality, however, is that this inversion occurs even without a recession, as was the case in 2001. Many market participants make the mistake of assuming that a recession, 2 consecutive quarters of negative GDP growth, occurred in 2001, but that wasn’t the case. (See chart below)

“From 2000 to 2001, the Federal Reserve, in a move to protect the economy from the overvalued stock market, made successive interest rate increases; while this may have initiated the readjustment, it is starkly contrasted with the severe, prolonged recession that would have occurred had the unsustainable growth continued unabated. Using the stock market as an unofficial benchmark, a recession would have begun in March 2000 when the NASDAQ crashed following the collapse of the dot-com bubble. The Dow Jones Industrial Average was relatively unscathed by the NASDAQ’s crash until the September 11, 2001 attacks, after which the DJIA suffered its worst one-day point loss and biggest one-week losses in history up to that point. The market rebounded, only to crash once more in the final two quarters of 2002. In the final three quarters of 2003, the market finally rebounded permanently, agreeing with the unemployment statistics that a recession defined in this way would have lasted from 2001 through 2003.”

“According to the National Bureau of Economic Research (NBER), which is the private, nonprofit, nonpartisan organization charged with determining economic recessions, the U.S. economy was in recession from March 2001 to November 2001, a period of eight months at the beginning of President George W. Bush’s term of office. However, economic conditions did not satisfy the common shorthand definition of recession, which is “a fall of a country’s real gross domestic product in two or more successive quarters.”

Although we have concrete evidence there was no recession in 2001, charts like the following pervade social media.

The reality is that most yield curve inversions are not the cause of recessions but rather excesses and imbalances in the market or economy are generally found to be the causation. Bond yields falling in the U.S., as they are today, is less an expression of economic weakness than it is a referendum on the Federal Reserve or simply the hunt for yield that can’t be found in overseas debt markets. And it’s for these reasons that we continue to see high concentrations among certain sectors even in the stock market. CNBC’s Michael Santolli discusses the rationale behind some investor behaviors that continue to put a bid in very large companies, including FANG stocks and with bond yields falling around the world.

“Big, dominant tech platforms and global branded-goods companies also get credit in the market’s unspoken logic as bond surrogates. Their cash flows are seen as durable and are expected to continue for many years to come.

This is why the FANG club and other popularly anointed growth stocks in its orbit do well when the market is clinging to “quality” and “defensive growth.” This also means the stocks that appear more expensive have been more in demand — making them more expensive. (Utilities, real estate, tech and staples — the strongest groups lately — are also the only ones with a premium valuation to the S&P 500.)

It’s worth noting, there is another tier of nontech (or, those not labeled as tech) companies that fit into this privileged class. Nike and Starbucks have been nudging up to record highs in recent weeks, and both trade at fat 50 percent premium to the market. These are elite brands that travel well globally and don’t rely on every extra point of world GDP growth to succeed.

With respect to the equity market and what actions investors are taking and what the bond market is signaling, another reality of current market angst is derived from the notion that history is repetitive. While this is often true, it is just as often found untrue. As we mentioned in Finom Group’s weekly Research Report, this time is different and in fact every time is different. We’re not interested in whether or not people like hearing that phrase, it’s a very simple fact; every economic cycle is different and every recession has a different causation and correlation. But in keeping with the theme of the bond yield curve inverting, we aim to identify why this time is different.

In the years that followed the Great Financial Crisis, new financial regulations (i.e., Dodd-Frank & Basel III-IV) were enacted to ensure a more stable and resilient banking system during times of significant market stress. One of the many byproducts of this new regulation is the liquidity coverage requirement (LCR), which requires financial institutions to hold a certain amount of high-quality liquid assets (HQLA) that’s sufficient enough to withstand a significant stress scenario.

What this means in practice is that banks have to hold a higher level of HQLAs (i.e., sovereign bonds) than before. When you couple this with the need for duration matched assets from pension funds and insurance companies in a world where there’s $10trn+ in negative yielding developed market debt, we get price blind buyers for bonds. And when you have price-insensitive buyers (institutions who buy because they have to), the impact on that market’s signaling value should be obviously negatively impacted. This has never been the case before in past cycles. This is just one reason as to why the yield curve may not serve as much of a valuable recessionary signal as it used to in the past. Need another reason; why certainly…

In Finom Group’s weekly Research Report we offered the following with respect to why spreads never achieved their typical levels during expansion cycles.

“As it pertains to the yield curve inverting, we can’t help but to reiterate that when a new and significantly behemoth player in the bond market comes along, it creates distortions. The long-end of the yield curve (10-year Treasury) has been bid up over the last several years as part of global quantitative easing programs. As such, it never had the ability to find sustainable sellers of bonds, thus suppressing yields. Under this dynamic, longer dated maturities/bonds have been within arms reach of shorter dated maturities/bonds for a prolonged period. This increases the odds of inversion once QE ends and as expansion cycles become extended. As many view a 10-year expansion cycle to be long in the tooth, they naturally diversify out of risky assets and into safer assets such as bonds, thus forcing yields lower, even if a recession isn’t at-hand.”

Ok, one more reason as to why a yield curve inversion this time around is not akin to occurrences from previous economic cycles as outlined by Tim Duyer. Fed Watch Tim Duy wrote in Bloomberg about the Fed’s recent and total about-face, writing:

It is hard to understate the importance of this shift. The Fed’s models haven’t worked this way in the past. In previous iterations of the forecasts, the expectation of unemployment remaining below its natural rate would trigger inflationary pressures. To stave off those pressures, the Fed perceived the need to raise rates above neutral to slow the economy enough to nudge unemployment upwards. Now the Fed believes it can let unemployment hold persistently below the natural rate without triggering inflation and without Fed policy becoming restrictive.

Duy goes on to note that, “The Fed apparently has finally realized that persistently low inflation remains a problem.” And “to avoid the problems of the zero lower bound for as long as possible, the Fed needs to ensure that inflation stays sufficiently high to hold expectations at its target and that they act to avoid a recession. The policy implication is that they need to err on the dovish side.”

While all this talk and discussion about why “this time is different” sounds very logical and is with substantial factual evidence; sometimes the market has a mind of its own and is found without logic. As such, don’t find yourself of the mindset as an investor taking actions solely on the basis of facts. In an algo-triggered market lacking fund inflows and limited CTA positioning year-to-date, anything can move markets rather sizably and swiftly.

As bond yields maintain in focus, Monday’s discussion about an inverted yield curve took another step toward greater focus on the probability of a rate cut in 2019.

“The 10-year is inverted versus the current fed funds. It should signal expectations that rates are going to be lower in the future, which would be consistent with notable risk of a recession,” said Jon Hill, U.S. fixed income strategist at BMO. “One of the fascinating things is the stock market is taking this in stride. The Fed is trying to extend this cycle as long as it can. Whether it will be enough is difficult to say.”

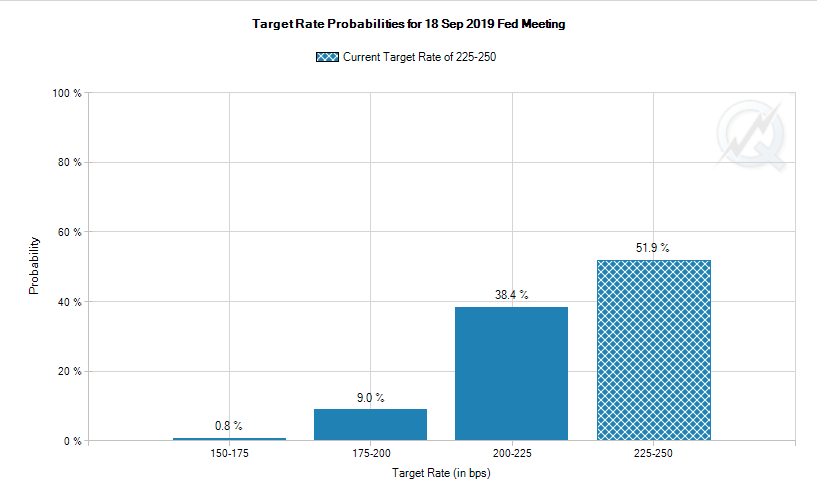

According to the CME FedWatch Tool, there is now a 49% probability of the Fed cutting rates by 25 bps come September 2019. Given what is taking place in the bond market, at the end of the month, the end of the quarter and with some $350bn in new issuance coming this week, it’s actually kind of telling as to why equity markets are brushing off the so-called inversion/recession rhetoric.

“As far as recession goes, our economist feels quite optimistic that a recession will be avoided, at least this year. The market is focused not only on U.S. fundamentals, but also on what’s happening in China, what’s happening in the rest of the world and how likely it is that political uncertainty, whether through trade policy or whatever, how likely is that to persist and beget a recession,” said Mark Cabana, head of short U.S. rate strategy at Bank of America Merrill Lynch.

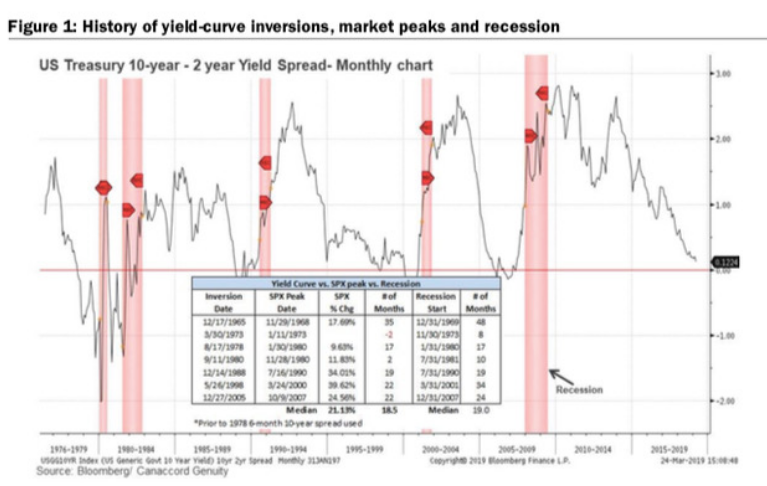

Canaccord Genuity chief market strategist Tony Dwyer weighed in on the yield curve inversion subject on Monday, issuing the following chart:

Dwyer went further to say, “Even if the YC (yield curve) inverts tomorrow, over the past seven economic cycles, the median SPX gain from the initial inversion to the cycle peak is 21%, with a recession a median 19 months after the initial inversion.”

The strategist also stressed that other recession identifiers, including the Fed’s Senior Loan Officer Survey, household debt service and financial obligation ratios, and consumer delinquency rates, have yet to set off alarms.

“Investors should wait for further signs of trouble in the credit market before turning defensive on stocks. The history of our favored credit metrics and what follows the inversion of the YC still suggests any weakness should prove limited and temporary.”

As mentioned already, there are a good many reasons, logical reasons, to believe “this time is different”. Nonetheless, that doesn’t suggest taking more risk in the market. Uncertainty can lead to self-fulfilling prophecies within the economy and the equity market. Being nimble, active and with light positioning can make for strong returns in a sideways trending market that is found with fits and starts. To this point, Finom Group daily/weekly trade alerts are found a great tool for building portfolio gains annually. Below are two of our trade alerts from Monday, as volatility was once again in play. The VIX rose to nearly 18 intraday before finishing slightly in the red on Monday.

While the equity market is seemingly taking the decline in bond yields in stride, to some degree and with equity futures pointing to a strong rally Tuesday, some analysts/strategists are urging caution and defensive positioning. Morgan Stanley’s Mike Stanley suggest defensive posturing is the optional strategy after a strong YTD market rally and ahead of a Q1 earnings recession that might also demand more insights into forward looking guidance.

“On today’s TOTM, Chief Investment Officer Mike Wilson says playing defensive may sound boring but in the face of ebbing growth and falling bond yields, that’s where the returns could be.”

Wilson has been suggesting investors “get off the bull” since January 29, 2019 and he hasn’t been wrong as the sideways market action persists. Certainly the S&P 500 has trended higher since Wilson’s earlier warnings, but after a 2-day decline in the S&P 500, the market is basically right where it has been since the end of January.

As an investor, we are forced to recognize there are a multitude of forces pushing and pulling at the economy and market at all times. With earnings season still a few weeks away, the market has an equal weighted opportunity to drift higher, lower or simply “chop around”. Headlines can and likely will determine daily direction. Some headlines will be more relevant than others; some will be stock specific such as the news out of Apple Inc. (AAPL) on Monday.

Ahead of Apple’s big new services reveal Monday afternoon, BTIG offered its expectations for the event and share price going forward. BTIG analyst Walt Piecyk wrote Monday that Apple Inc.’s upcoming launch of its streaming-media service “could trigger a sell-off in the stock.” The company is scheduled to make an announcement on Monday at 1 p.m. ET, which is widely expected to concern the company’s efforts in streaming video. “We believe there is little that Apple can say at its event today that will satisfy media skeptics,” Piecyk wrote. He said that sell-offs have become typical following Apple events. “Most of today’s criticism will probably be accurate but viewed through a short term lens,” Piecyk wrote, including that it’s difficult and expensive to become a formidable media player. He argued that the company shouldn’t look toward a big acquisition as a way to bolster its content ambitions. Nonetheless, he boosted his price target to $220 from $189 in his Monday note, writing that the outlook for Apple’s 2020 earnings looks favorable relative to the S&P 500.

Apple deepened its push into services on Monday, announcing a credit card launched in partnership with Goldman Sachs (GS) as well as new streaming services centered on news, videos and gaming.

Video streaming

Apple’s efforts with video programming are twofold: The company intends to make it easier for users to purchase subscriptions to services like HBO and Showtime through its new Apple TV offering, and the smartphone maker will also provide original content with big-name stars on a Netflix-like (NFLX) streaming service called Apple TV+.

Game streaming

Apple also plans to launch a streaming service for videogames, though the product seems mainly focused on independent studios. Arcade, the new service, will feature “over 100 new and exclusive games” and will be free of both ads and in-game purchases. Participating publishers include Bossa Studios, Klei Entertainment, Mistwalker Corp. and Snowman.

News bundling

Apple will bundle subscriptions to more than 300 magazines as well as certain content from The Wall Street Journal and the Los Angeles Times in a new offering, which will cost $9.99 a month. Vogue, The Atlantic, National Geographic and Golf are among the participating magazines. Apple will allow subscribers to share the new Apple News+ service with their family members.

An Apple credit card

After experimenting with peer-to-peer payments and other forms of mobile payments, Apple is trying its hand at physical cards. The company announced the Apple Card, a titanium credit card with digital components, which users can apply for via their iPhones.

The Apple Card offers a cash-back rewards program, giving cardholders 1% back on general purchases, 2% back on Apple Pay purchases and 3% back on purchases made within the Apple ecosystem. Rewards will be transferred to the Cash Card, a digital card that’s part of the Apple Wallet and that can be used wherever Apple Pay is accepted.

Users will get a titanium card once they are approved. Apple partnered with Goldman Sachs and MasterCard Inc. on the card, which will be available this summer. Big picture takeaway according to Finom Group and as it pertains to the new Apple Card… go take a look at Visa’s annual sales and market cap. If you don’t see the opportunity and fail to juxtapose that opportunity with the loyal Apple user base size…

Corporate headlines will likely flow through the market as we head into a critical earnings season, where S&P 500 EPS estimates show a decline of 3.7% is in the cards, according to FactSet.

Until then, economic data will also lend itself favorably or negatively toward investor sentiment. While the slowdown in the Eurozone continues and Brexit concerns persist, the negative yielding German Bund is held culprit with respect to the latest flight to bonds. German PMI data released last Friday spurred the bid in bonds and consequential drop in bond yields With German PMI data found wanting for expansion, oddly enough, the German Ifo Business Climate Index, a survey of roughly 7k firms, topped consensus estimates and prior month readings in both the current conditions and future expectations components.

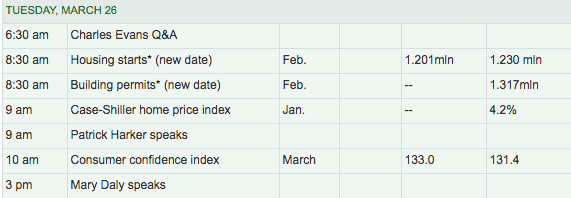

With respect to U.S. economic data, the focus will turn to the housing sector and consumer confidence on Tuesday.

Subscribe today and receive our weekly Research Reports, daily/weekly trade alerts and access to our live daily Trading Room where many of our trade alerts are formulated.