After two consecutive days of losses for the major indices, first back-to-back loss of the New Year, equity futures are looking flat on Tuesday. The losses for the U.S. equities have been minor compared to that of the Q4 2018 period and with volatility somewhat tempered. More importantly, the losses come as earnings season has commenced and ahead of today’s all-important Brexit vote. Although the Brexit vote has been languishing overhead for several months, the vote itself is largely expected to fail and has carried such sentiment for some time now. So let’s quickly look at the Brexit vote details before moving forward.

On Tuesday, Parliament will vote on May’s Brexit deal. The vote was initially scheduled for December but was delayed as May expected to be defeated. For Tuesday’s vote, many market participants also expect May to lose. Labor Party leader Jeremy Corbyn meanwhile said last week that the handling of Brexit demanded fresh elections. This basically means that upon a failed Brexit vote, a vote of no-confidence will commence, seeking a government overhaul and ousting of Theresa May.

“Are we going to see a no-confidence vote in the government? Or another attempt by Theresa May to secure concessions from the EU? Will there be an Extension of Article 50? Or even extreme scenarios such as a new general election and a second referendum? Each of these scenarios will have a different impact on the pound,” said Hussein Sayed, chief market strategist at FXTM.”

For U.S. investors, the impact of the vote will likely be felt later in the trading day. Parliament will vote in the 2:00 p.m. EST hour and when the headlines break, we would expect to see at least a temporary reaction from U.S. markets.

As previously mentioned, U.S. equities are looking to snap a 2-day losing streak and with the financials kicking-off earnings season. For a review of Monday’s trading activity, do review Finom Group’s latest synopsis from Wayne Nelson in the link provided

Citigroup (C) was the first major bank to report results on Monday and will be followed by reports from J.P. Morgan Chase (JPM) and Wells Fargo (WFC).

Shares of Citigroup initially fell upon reporting a bottom line beat, but a top line miss for Q4 2018. The bank made $1.61 in profit per share excluding one-time impacts of the U.S. tax overhaul, beating analysts’ expectations for $1.55 per share. Operating expenses fell 4% to $9.89 billion in the quarter, driven in part by lower compensation costs. Earnings of $4.2 billion rose 14% in the quarter, thanks to lower expenses, credit costs and a lower corporate tax rate.

The bank said fixed-income revenue dropped 21 percent to $1.94 billion from a year earlier as trading conditions deteriorated after the company gave guidance in early December. That miss accounted for the lion’s share of the firm’s revenue shortfall: Citigroup said it produced $17.1 billion in company-wide revenue, below the $17.6 billion average estimate of analysts surveyed by Refinitiv.

“A volatile fourth quarter impacted some of our market-sensitive businesses,” CEO Michael Corbat said in the earnings release. He added that management “remain committed” to delivering on their 2019 targets.

Although shares of C initially fell following the revenue miss announced, once the market opened for the trading day on Wall Street, shares quickly rebounded and finished 4% higher on the day. Here’s what CNBC’s Jim Cramer had to say about Citigroup’s results and why the share price surged through the day:

“When I listened to Citigroup’s terrific conference call this morning, the one that sent the stock soaring 4 percent, I sure got the sense that we have a lot less to fear than we think.”

Cramer pointed to some of Citigroup CEO Michael Corbat’s remarks on the conference call. Corbat said management “clearly” saw “a disconnect between what we see in our business and what the markets are saying,” adding that they found no evidence of a significant slowdown.

“The biggest risk in the global economy is one of talking ourselves into the next recession as opposed to the underlying fundamentals taking us there,” the CEO said.”

The 21-percent year-over-year decline in Citi’s trading volume, the “only meaningful negative” in the bank’s report, only gave the quarter “the appearance of weakness”, said Cramer. Trading activity has nothing to do with the economy.

Mirroring the comments from Citigroup’s CEO about a the nonexistence of a recession near term was J.P. Morgan Chase’s CEO only a month ago.

“Markets from equities to high-yield bonds that have been flashing warning signs are probably an overreaction to slowing growth rather than a precursor of imminent recession.”

Finom Group remains of the opinion that investors will see gyrations in the market and through the earnings season. With a reasonably favorable reaction to Citigroup’s results, we’ll see what Wells Fargo and J.P. Morgan have to say ahead of the opening bell. Analysts’ views on what J.P. Morgan will report are mixed and Jefferies downgraded shares just last week.

J.P. Morgan Chase was downgraded to Hold from Buy by analyst Ken Usdin at Jefferies, who said revenue could miss high expectations following “excellent” results last year. With Citigroup already missing revenue expectations, it seems as though Usdin may not be too far off with his downgrade and thesis. Usdin said net interest income could fall shy of forecasts, given potential for fewer interest rate increases by the Federal Reserve this year. He said fees could miss expectations, given lower trading and investment banking, asset management and mortgage fees.

Quickly, and I do mean quickly because we want to move on to the market outlook but remain with the growing threat of a global economic slowdown. Overnight, China outlined more stimulus plans are to come as a means of contending with its own economic slowdown. Some analysts believe China could deliver 2 trillion yuan ($296.21 billion) worth of cuts in taxes and fees, and allow local governments to issue another 2 trillion yuan in special bonds largely used to fund key projects. Most, however, expect the fresh stimulus will take months to start feeding into the economy.

Monetary policy will be made more forward-looking, flexible and targeted, the People’s Bank of China (PBOC) said. “A prudent monetary policy does not mean that there will be no changes”, PBOC Deputy Governor Zhu Hexin said at the press conference.

As we look at the current state of the market and how equities are performing, we can’t help but to feel reassured by the trend of upward motility. Having said that, it is increasingly apparent that the market is struggling to break-out of current resistance levels. Catalysts to move the market higher range from a deal that would reopen the U.S. government to improved earnings outlook. Headwinds to the market remain a prolonged U.S. government shutdown to global economic slowdown and recession fears. With so much to consider in the way of market momentum, analysts also have polarizing views.

Morgan Stanley’s chief equity strategist Michael Wilson, best known for his “rolling bear market” call that proved most accurate in 2018 is out with his recent notes on where the market is likely heading. Furthermore, while his near-term outlook proves bearish, it’s what investors should be doing with the bearish outlook should it come to pass. With regards to the present market conditions and levels here is what Wilson offered in his recent notes to clients:

“The issues we still need to deal with include the fact that we are in the midst of a fairly steep and broad negative earnings revision cycle, and there is significant technical resistance/overhead not far above current prices.”

Wilson is once again leaning short-term bearish, because “as we deal with these issues during 4Q earnings season and perhaps see some further deterioration in U.S. economic data, we think the S&P 500 will suffer a re-test of the lows we experienced in December, but on less negative momentum and better breadth.”

It’s important to reflect for a moment on the comments related to “negative momentum” and “better breadth”. Finom Group made recognition of the more positive market breadth over the weekend and within its weekly research report to subscribers. Subscribe today to read our weekly research report.

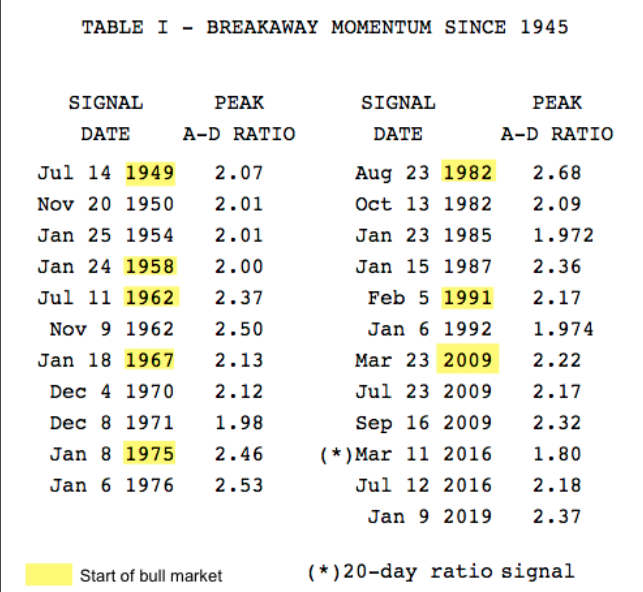

We reported on the fact that two significant market breadth moves occurred last week. On Tuesday this past week, the NYSE experienced a “Zweig breadth thrust. This is quite a significant breadth move for markets to achieve. But in addition to a Zweig breadth thrust, another market breadth move was achieved.

On Wednesday of this past week, a “breakaway breadth thrust” occurred. As explained by Walter Deemer, this occurs when 10-day advancers are twice 10-day decliners. In order for this to occur, it requires persistent strength without any intervening weakness over a 2-week period. In the past 70 years, this has occurred only 21 times.

What is noteworthy about both the Zweig and Breakaway breadth thrusts is that none took place within the context of a bear market. This might suggest there is evidence that the current technical bear market is more of a deeper correction within a still ongoing bull market.

To be clear, Wilson is of the opinion that the market should retest it’s December lows if not break the December lows if only for a short period. Should that happen, and should the S&P slide back to Wilson’s bear case support level of 2,400, the strategist says he would be an “aggressive buyer” and “if we actually suffer the re-test we are expecting, we would be buyers of that almost regardless of what is going on, assuming it happens on less momentum and better breadth.”

Wilson believes that analysts’ forecasts will soon re-price to reality, and in fact, will soon forecast an earnings recession, the first one since the 2016 commodity collapse episode.

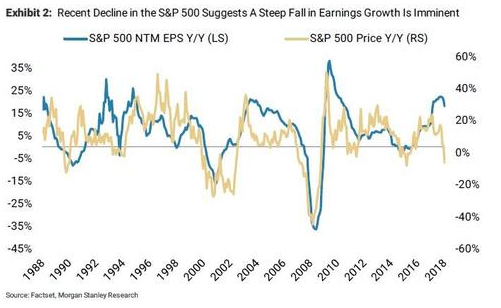

As shown in the chart below, the recent YOY decline in the S&P 500 is close to what we observed in 1990; and if we get a full re-test and break as Wilson expects in the next few months, it will likely be equivalent. In other words, between here and there, the S&P 500 would be pricing in an earnings recession and perhaps a shallow economic recession. Consistent with Morgan Stanley’s 2019 earnings call, the strategist now expects the blue line in Exhibit 2 (NTM EPS growth) to rapidly catch-down to the yellow line (price change) as markets lead the fundamentals. Wilson suspects “such a rapid decline in forward earnings will provide a reason for stocks to revisit the December lows” but as he adds, “that’s the trap and the time to buy, not sell.”

Wilson advises clients that “2600-2650 on the S&P 500 is a good level to start lightening up as we enter what is likely to be a period of negative news flow on earnings and the economy.”

Wilson’s commentary and analysis has proven prescient in the more recent past and gives investors/traders reason to pause around the levels offered, if not outright lighten up on market exposure. There is however a caveat that could be offered in the way of earnings season as we’ve already seen within the reaction to Citigroup’s earnings release. The question is whether or not an earnings recession, as Wilson has forecasted, is or isn’t already priced into the market and as multiples have already contracted beyond their 10-year average? Additionally, are such valuations at levels where even modest Q4 earnings beats and innocuous guidance/commentary find the market trending beyond overhead resistance? If the answer to both questions posed is a resounding NO and Wilson’s forecast and recommendation come into play then… so what? This might simply be the difference between a trading period and the art of investing. While there may be downside yet to be realized, according to Wilson it will present a buying opportunity that has duration and upside from that point. If all we are really forced to consider is the formation of a double bottom with modest and expected slower growth fundamentals, this should be rationalized as an opportunity and not found with increased fearfulness and concerns. Stay rational if choosing to trade in the short-term folks, stay rational, as the longer term outlook remains favorable. With this in mind we now turn our attention to UBS’ latest advisement.

UBS, the world’s largest wealth manager, said investors should keep their money in the stock market this year regardless of their risk appetite.

“You have to stay invested, whatever your risk tolerance can bear,” Mark Haefele, global chief investment officer at UBS Global Wealth Management.

Investors would have missed out on a 10-percent rally if they had sold their holdings on Christmas Eve — when U.S. stocks experienced a massive sell-off — and re-entered the market this month. In addition, a recession is not likely to happen this year, so corporate earnings have room to grow, although at a slower pace than before.”

Finom Group will deliver its weekly State of the Market snapshot video on Friday, but between now and then we expect headwinds and tailwinds for the market to produce market gyrations. Our perceived headwinds remain as follows:

- Strong U.S. Dollar

- China/U.S. trade policy (likely resolution soon)

- Government shutdown potential to curtail economic output if prolonged

- Global economic slowdown

- Stable crude oil prices

With our headwinds outlined, now let’s take a look at the tailwinds as follows:

- Shifting Fed from hawkish to dovish with rate hikes paused and possible further action on curtailing the amount of balance sheet run-off

- Government shutdown ends

- China/U.S. trade deal brings about more certainty, stimulates capital spending

- Valuations compelling as recession seemingly unlikely

- Dampened market volatility

- Fund flows have turned positive for equity markets