The major indexes posted slight weekly losses last week. The Dow and S&P 500 both fell 0.5% for the week, while the Nasdaq pulled back 0.7 percent. The move lower this week took place after the averages jumped more than 2% last week, kicking the S&P 500 above its 50-DMA and out of consolidation territory. It is rather unfortunate to witness markets having no follow through last week, even as volatility continued to decline. The S&P 500 index (SPX) had a $33 expected move last week, which is slightly lower than the expected move in the SPX this coming week.

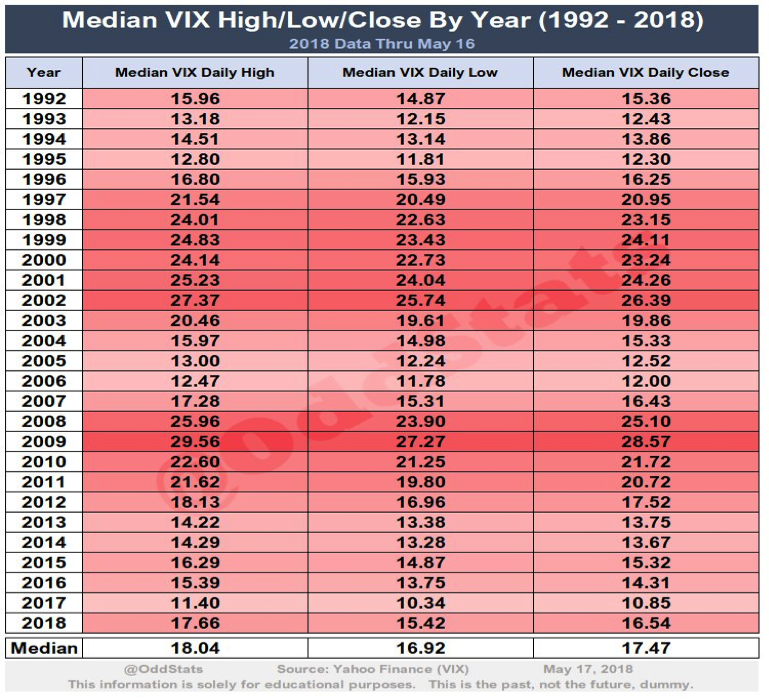

The volatility crunch in the markets over the last month or so has been a welcome sight for many investors. One could easily argue the lack of market volume is due to the outsized volatility we’ve witnessed since the February 5 VIX event. The crosscurrents of macro-factors have given reason to pause for a great many fund managers since the markets torrid, January rise. Volatility is unlikely to rest at current levels for very long or sustain the current level on average for the year. Review the table of Median daily VIX prices below.

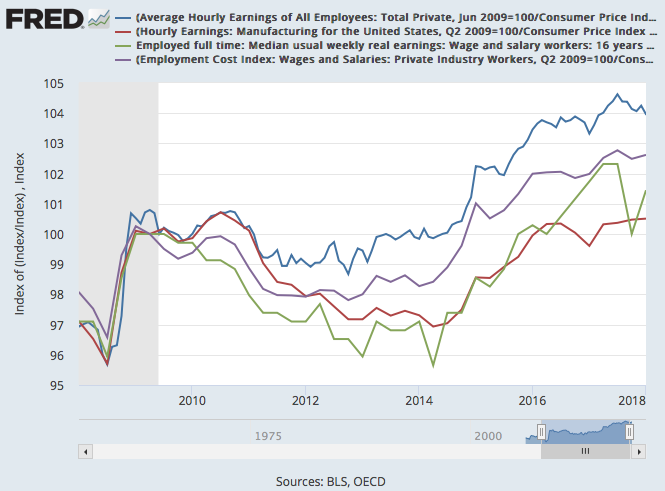

As mentioned earlier, the crosscurrents in the market are likely to plague investors through much of 2018 and with fits and starts. Having offered that subjective stance, the fundamental backdrop of the economy and corporate earnings remain quite positive. Consumer sentiment and spending remain positive and growing. Wages are growing once again despite popular belief and even when compensating for consumer price increases as shown in the wage chart below:

Even with a positive economic condition and outlook for the year, it has been a difficult investing period. Most down days in the market don’t end at their lows and most up days don’t end at their highs. This is a clear indication that conviction has been lost, at least for now.

The Dow Jones industrial average has not closed below its 200-DMA for 472 sessions, its longest stretch since its streak from 1984 to 1987 and its seventh-best on record. In recent weeks the DOW did test the 200-DMA on an intra-day basis, only to finish above the key level. Ari Wald, head of technical analysis at Oppenheimer suggests the Blue Chip index is signaling strength in the months to come.

“Since that successful test, which created a higher low, we’ve now reversed this trend of lower highs that we’ve been in since January,” Wald said. “When you add it all up, we think this correction that we’ve been in since January is coming to an end and we think we’re now set up for the inflection higher.”

Highlighting last weeks slight decline in the broader SPX index were headlines surrounding the 10-year yield rising steadily over 3 percent. Some investors and fund managers fear that the dramatic rise in the 10-year defines an economy that might be accelerating too quickly, and that the Fed might have to step up its pace of interest-rate hikes. The notion that higher rates signal the end of an economic cycle isn’t presently in the data. The various high and low frequency credit measures that suggest a credit event is coming are not showing increased signs of stress. So while there are a great many historical charts and data that show the adverse affects of past rate hike cycles on the economy, they simply aren’t in the data at present and haven’t been since the Fed began tightening.

There is a significant issue of government debt supply coming to the market in 2018. The Treasury will issue more than $500 billion in notes and bonds from the second to the fourth quarter, pushing the total to around $650 billion for the year. Last year, the total came to just $420 billion. That’s an increase of more than 50 percent. Michael Schumacher, head of rate strategy at Wells Fargo offered the following sentiment on the subject of higher rates and yields:

“If the economic data are decent and if the Fed is not getting too crazy in terms of being hawkish, rates going up shouldn’t be that scary,” said Schumacher. “It’s just that we’ve had a pretty calm market for a couple of years, barring the last few months. I think anything that’s really a signal rate gets people a bit nervous.”

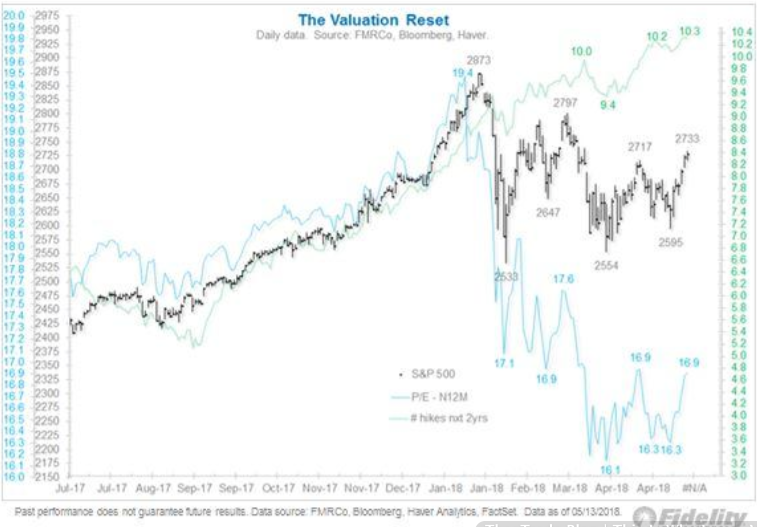

The bottom line is that the economy warrants higher rates and yields. The pace of rate and yields increasing, however, has been the cause of some consternation more so than the level. One thing is for sure; rates/yields can rise together and often do. The chart below reflects the 1-year move in the 10-year yield overlay with the S&P 500.

It’s only been in recent months that the divergence between the two has manifested and largely due to yields rising to levels not seen in several years. It has allowed for a rather significant reset in the price-to-earnings multiple of the S&P 500. As Q1 2018 corporate earnings have proven to grow roughly 26% YOY, the S&P 500 has gone sideways to lower. The chart below identifies this great reset of the clock and/or PE of the S&P 500:

Let’s now take a look at the latest Q1 2018 S&P 500 earnings forecast from Thomson Reuters. Recall that in the previous forecast, Reuters forecasted earnings to grow 26% during Q1 2018. To date, 93% of the companies in the S&P 500 have reported actual results for Q1 2018. The new forecast, reflected below, shows a slight positive revision to this forecast:

Aggregate Estimates and Revisions

- First quarter earnings are expected to increase 26.2% from Q1 2017. Excluding the energy sector, the earnings growth estimate declines to 24.2%.

- Of the 465 companies in the S&P 500 that have reported earnings to date for Q1 2018, 78.9% have reported earnings above analyst expectations. This is above the long-term average of 64% and above the average over the past four quarters of 75%.

- First quarter revenue is expected to increase 8.2% from Q1 2017. Excluding the energy sector, the revenue growth estimate declines to 7.8%.

- 2% of companies have reported Q1 2018 revenue above analyst expectations. This is above the long-term average of 60% and above the average over the past four quarters of 69%.

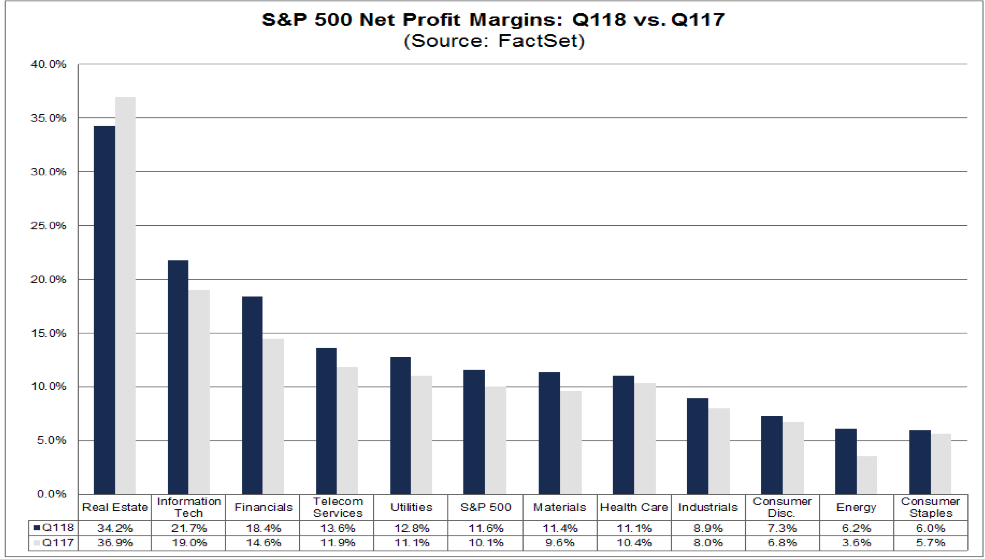

While the earnings growth outlook continues to strengthen, the mantra of rising rates eating into profits also carries forward. An offset to this belief is the organic revenue growth that aligns with consumer spending rising, wages rising et cetera. Additionally, even as rates have actually been rising from low levels for some time now, corporate net operating profits have been rising since last year.

Even with energy prices having risen significantly in 2018 when compared to a year ago, the affects on corporate earnings and consumer spending hasn’t been negatively impactful. Prices at the pump for a gallon of gas are nearly $.50 higher than they were last year, but still lower yet than the $3.50-$4.00 seen during periods from 2012-1014. When prices are low, consumers spend and when prices are high consumer still spend. Most consumers view higher gasoline prices as temporary and forgo active saving plans to offset the higher energy prices. In a note to clients, Chief Investment Strategist at LPL Research, John Lynch pointed out, “while consumers will feel the impact of higher oil prices, even in the worst case scenario we would expect the impact to be half that of the benefit of recent tax cuts.”

Lastly, but certainly not least, on Saturday evening headlines broke that read positively regarding the U.S./China trade talks.

“To meet the growing consumption needs of the Chinese people and the need for high-quality economic development, China will significantly increase purchases of United States goods and services. This will help support growth and employment in the United States.”

The news might find a great deal of angst evaporating from the markets early next week due to the headlines over the weekend and serve to boost the major averages initially. More retail earnings are due to come this week. The economic data calendar is rather light during the trading week and is highlighted by the release of the FOMC minutes on Wednesday, which could deliver more market gyrations.