Market jitters cooled yesterday with the major averages in rally mode. The Dow rose nearly 240 points or .99% to 24,322 and the S&P 500 was up 27.54 points or 1.04% to 2,666. The Nasdaq outperformed, rallying 115 points or 1.64% on the heels of better than expected tech sector earnings. But even with a sharp move higher on Thursday, the major indices are all looking at losses for the week coming into the final trading day of the week. For the week, the Dow was looking at a loss of 0.6%, the S&P 500 a drop of 0.1% and the Nasdaq a loss of 0.4 percent. Those would be the first fall in three weeks for all those gauges.

With this week representing the greatest volume for reporting companies, Friday is a light earnings day. Investors are expecting earnings from Colgate-Palmolive Co., Phillips 66, Exxon Mobil Corp. and Chevron Corp. among those expected to report.

Shares of Starbucks Corp. fell in the after hours trading session yesterday and after the company reported Q2 2018 results. Starbucks said it earned $660 million, or 47 cents a share, in the quarter, compared with $653 million, or 45 cents a share, in the year-ago period. Adjusted for one-time items, the company earned 53 cents a share, compared with 45 cents a share a year ago. Sales rose 14% to $6.03 billion, from $5.29 billion a year ago, the company said. Analysts polled by FactSet had expected GAAP and adjusted earnings of 53 cents a share on sales of $5.93 billion. Same-store sales rose 2.2%, the company said. Starbucks reiterated its 2018 outlook but said the guidance excludes the yet-to-be determined impact on its previously announced plan to close more than 8,000 company-owned stores for half a day to conduct racial-bias training for its employees in the U.S. Comparable-store sales are seen up 3% to 5% globally for the year, and revenue growth is seen in the high single digits, Starbucks said. Per-share earnings are seen in a range between $3.32 and $3.36 in 2018, with adjusted EPS in a range between $2.48 and $2.53. The analysts surveyed by FactSet expect an adjusted 2018 EPS around $2.49. In terms of the share price reaction to the results, this was the smallest sell-off post earnings release in the last two quarters. Finom Group maintains ownership of SBUX shares and a Buy rating.

Of course the big report after hours yesterday came from Amazon. The retail giant reported net income of $1.6 billion, or $3.27 a share, up from $724 million, or $1.48 a share, a year ago. Revenue jumped 43% from last year, to $51 billion from $35.7 billion. The report blew away expectations: Analysts on average projected Amazon to report earnings of $1.24 a share on sales of $49.9 billion, according to FactSet. Amazon profit increased 221% year-over-year and the 43% gain in revenue foreshadows another increase in revenue growth this year. To assist the revenue growth, Chief Financial Officer Brian Olsavsky announced that Amazon will increase the annual price for Prime subscriptions to $119 from $99 for new subscribers on May 11, with current subscribers paying the higher price when renewing after June 16. The company’s subscription services segment, which includes Prime as well as other subscriptions, such as an e-books offering and Amazon Music, grew 60% year-over-year to $3.1 billion in sales. Amazon said AWS had operating income of $1.4 billion, up from $890 million, as revenue topped $5 billion for the second consecutive quarter, at $5.44 billion. AWS revenue grew 48.6% from the year before, while operating income increased 57.3 percent. Amazon has also moved into brick-and-mortar retail, acquiring the grocer Whole Foods and recently striking a deal with Best Buy Co. Inc.. Amazon’s physical-store sales recorded $4.26 billion in sales, down slightly from $4.52 billion in the holiday shopping quarter.

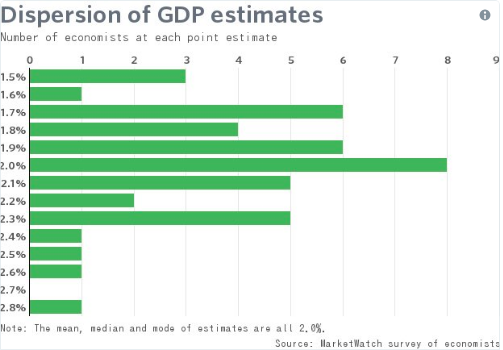

With strong earnings being reported and the expectation for the totality of the Q1 reporting cycle expected to show S&P 500 earnings growing 18%-20% YOY, investors will be focused on Q1 2018 GDP results Friday. A reading on the GDP is expected at 8:30 a.m. Eastern Time, alongside the release of the employment cost index. Economists polled by MarketWatch are expecting economic growth to come in at 2%, down from 2.9% in the fourth quarter. The Atlanta Federal Reserve’s GDPNow tool predicts gross domestic product will slow to 2% from 2.9% in the fourth quarter. Some economists see an even weaker reading to be reported.

As far as the segment breakdown for Q1 2018 GDP results, consumer spending remains the largest segment. After a strong Q4 2017 period for consumption where consumer spending grew 4%, the measure likely slowed to around 1% in the first-quarter of 2018. Investment in new homes probably fell early in the year and that will also curtail GDP growth. Businesses appear to have spent less on equipment in the first quarter as well.

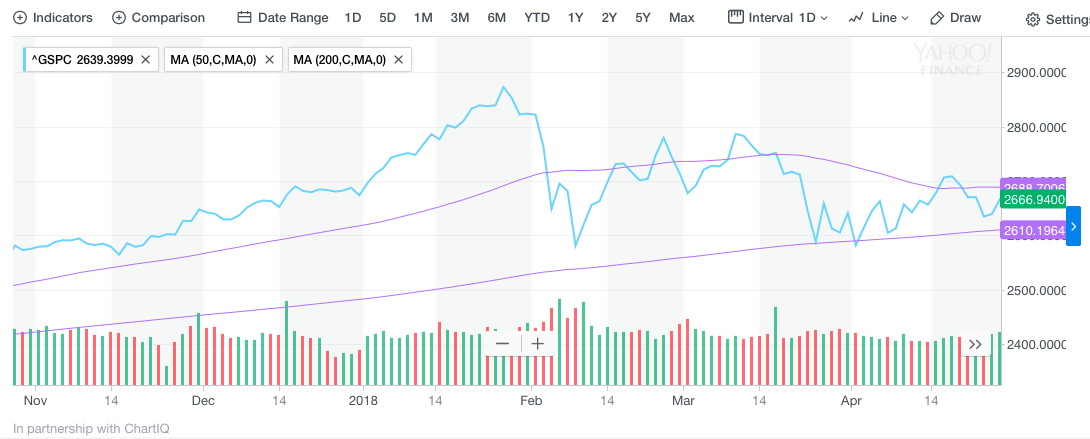

The S&P 500 has been range bound ever since correcting in February 2018. Yesterday’s rally, however, put it closer to the 50-DMA than the less desirable 200-DMA as depicted in the chart below.

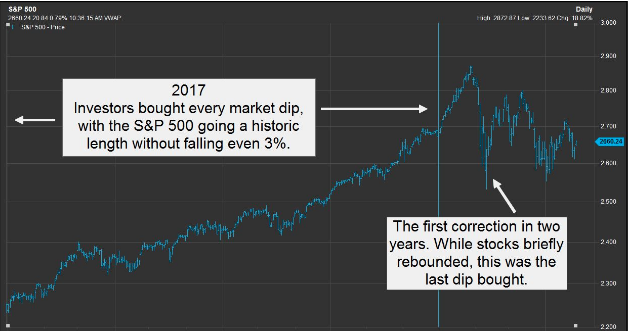

But even with outsized strength in earnings, investors haven’t “bought the dip” as they did with great frequency in 2017. In fact, in 2017 investors bought every single dip (BTD) in the market. The following chart shows this new era of market volatility that has also done away with the BTD mentality, at least for now.

“What really killed the ‘buy the dip’ mentality was the second pullback we saw. That’s when it all changed, and people realized we weren’t looking at a temporary period of high volatility, but a new volatility regime,” said Randy Frederick, vice president of trading and derivatives for Charles Schwab. They might have gotten burned buying the correction, and now they’re more hesitant. Volatility has been sustained for weeks now, and it’s become too darn stressful to think about jumping in. People are trickling out of the market.”

Low bond yields, the prospects for Tax Reform and the Fed’s dovish stance all lent themselves to the low volatility regime and BTD mentality that defined the markets in 2017. But with Tax Reform in the rear view window, yields now rising and a more hawkish Fed unwinding its balance sheet at a pace of $10 billion a month this year, a “sell the rip” investor mentality seems to have taken hold.

“We don’t have the Fed at our backs like we had for several years, which means the ‘buy the dip’ mentality is waning. You have to be more wary than you used to be, and reevaluate how attractive stocks look relative to other assets,” said Michael Mullaney, director of global market research at Boston Partners.

Possibly the most significant news of the day and what the media will focus on through much of Friday have little to do with equity markets. The leaders of North and South Korea have pledged to jointly eliminate the risk of war and work together to achieve complete denuclearization of the Korean Peninsula. The joint statement concluded a historic, bilateral summit aimed at achieving peace between the two conflicted nations for the first time in more than sixty years. The meeting of the Korean leaders was the first in more than a decade. The two Korean nations promised to ease military tensions, work together to achieve a peace regime, and work toward a nuclear-free region. They also pledged to improve inter-Korean relations and work toward co-prosperity and achieve a future of unification. Both nation’s leaders praised President Donald Trump and his administration for facilitating the talks and peace accord between the two Koreas.

Wall Street definitively has a good deal of positives to feed off of be they fundamentally driven corporate profits or geopolitically via the historic Korean developments. Will that prove enough to carry the major averages positively through Friday’s trading session? GDP results may be the determining factor as equity futures are largely flat to lower presently and with the Nasdaq being the outlier, up nearly 1.25% on the heels of AMZN Q1 2018 results.

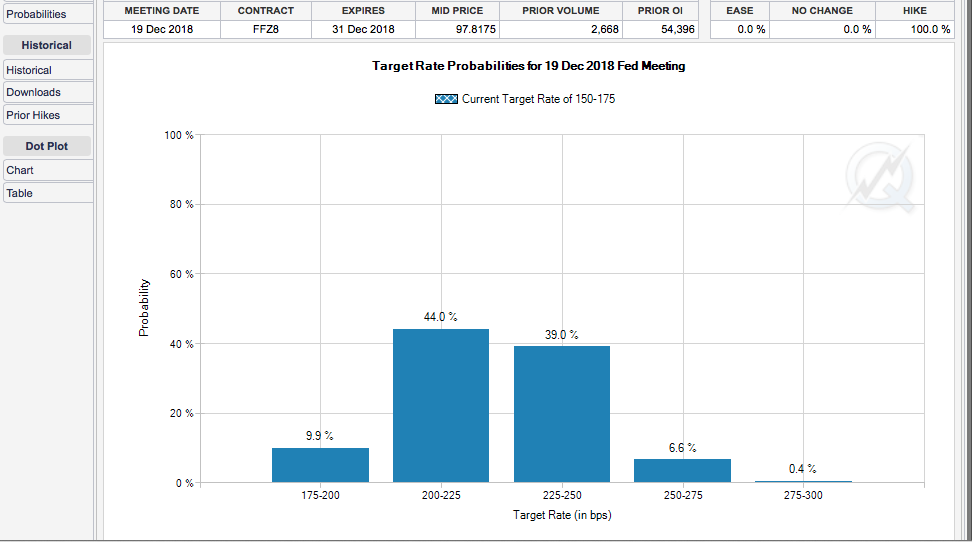

GDP pending results comes at a time when rates and bond yields are both on the rise. A Q1 GDP reading that comes in better than expected may give economists reason enough to boost the probability of a 4th rate hike this year on the grounds the economy is performing at a faster/hotter pace than anticipated. Already this week the CME’s Fed Fund Futures show an uptick in the probability of a 4th rate hike in December by nearly a half percent when compared to last week.

A GDP reading that comes in lighter or weaker than expected may prove equally negative for equity investors who fear rising rates and bond yields at a time when the economy doesn’t support such measures and inflation. The days of the goldilocks economy and market may have gone the way of 2017… out with the old!

Lastly, but not least in our trade of the day yesterday we highlighted and alerted to the dip in shares of SODA at the market open.

Subscribe to finomgroup.com today and trade with us by using our private Twitter feed alerts!