After the worst December since 1931 and the worst year since the financial crisis, stocks enter 2019 hobbled. The S&P 500 (SPX) will begin trading at 2,505 in 2019 after finishing down 6.2% in 2018, and down 9.6% in December alone.

Some strategists and analysts are of the opinion that the disconnect between the economy and stock market set up for a more favorable outcome for equity investors in 2019, even with the expectation for slower growth.

Most Wall Street strategists in a CNBC survey maintain a rosy view for the bull market, and see it extending its run for another year, for an average year-end target of 3,000, a 20% gain.

“Based on fundamentals, I don’t think the pullback we had in this market was ever justified. Markets will do what they’ll do. I think you have significant upside here. Therefore, we would think that the bottom has been put in this market,” said Jonathan Golub, chief U.S. equities strategist at Credit Suisse.”

While U.S. economic fundamentals have proven stable and strong throughout 2018, it’s counterparts and trading partners’ economies haven’t performed as well. China’s latest economic release on manufacturing is already sending a chill throughout the global equity markets.

Results of a private survey on China’s manufacturing for the month of December showed factory activity contracted for the first time in 19 months amid a trade dispute with the U.S.

The Caixin/Markit Manufacturing Purchasing Managers’ index (PMI), a private survey, fell to 49.7 in December from 50.2 in November. Analysts’ in a Reuter’s poll predicted the PMI to come in at 50.1 in December.

With a slew of underperforming economic data from China released in the Q4 2018 period, the government has in recent months unveiled a slew of policy measures, including cuts in banks’ reserve requirement ratio (RRR) to boost lending, tax cuts and steps to fast-track infrastructure projects. Beijing has particularly focused its attention on small firms and private enterprises, which are vital for economic growth and employment, as tight liquidity conditions and trade frictions. More policy support is expected in coming months.

“We expect a total of 250 basis points of RRR cuts in 2019, with 100 bps RRR cut likely ahead of the lunar New Year starting on Feb. 5,” Nomura economists wrote in a note.

In the shadows of the most recent Chinese manufacturing data, U.S. equity futures are pointing to a 400-point loss on the Dow Jones Industrial Average (DJIA). European markets are also sharply lower across the board. It remains to be seen whether or not markets can shrug off the Chinese data in favor of domestic economic data. U.S. investors are awaiting labor data due ahead on Thursday and Friday.

After a disappointing Nonfarm Payroll report for November, showing job growth of just 155,000, the labor department is expected to show the economy had grown the number of jobs to 185,000 in December. Additionally, average hourly earnings are expected to tick up slightly, from .2% in November to up .3% in December, according to economists polled by MarketWatch.

While 2018 proved to be a rocky year for investors, blame passive, sticking money in an index fund, and momentum, buying the winners, selling the losers, investors for these market swings, David Kelly, J.P. Morgan Asset Management’s chief global strategist, said on a call Thursday.

“Unless the swings are “validated by actual weakness in earnings or increases in interest rates…then they will fade,” and it’s probably time to buy.

Other market strategists are singing the same tune as Kelly. Northman Trader’s Sven Henrich suggests, “Earnings coming in January will likely not show the crisis markets appear to have priced in. If anything, in the short term, valuation excess has been removed by this correction.

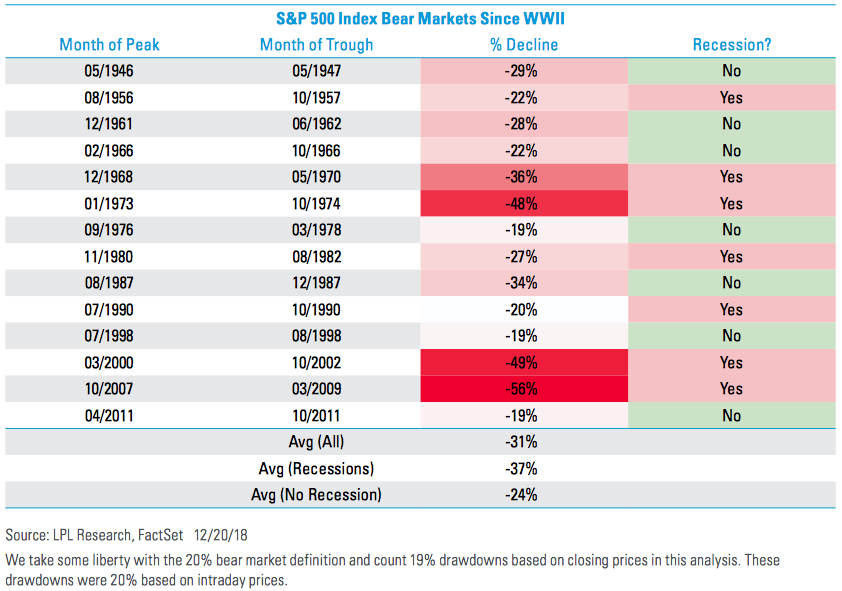

For equity investors, 2018 certainly felt like a bear market. While the S&P 500 did indeed fall just over 20% from its market highs, it failed to close in bear market territory for any trading day during the year. Nonetheless, the vast majority of S&P 500 stocks did indeed fall into a bear market during the 4th quarter of 2018.

Since World War II, there have been 14 bear markets, with 7 of them accompanied by a U.S. economic recession and 7 without an accompanying recession. As shown in table below, the recessionary bear markets were painful for stock investors, with an average S&P 500 decline of 37 percent. (Table provided by LPL Financial)

Three of the past four non- recessionary bears ended at 19% corrections (reaching the 20% threshold during intraday trading).

“The fourth, the 34% decline in 1987, occurred under very different conditions. The S&P 500 was up more than 40% year to date in August 1987, compared to just below 10% through the September 20, 2018, high, while long-term interest rates shot up from 6% to 9% in 1987. So while bear markets can occur without a recession, if the economy is still growing, market declines tend to stop at around a 20% decline.”

In the past four bear markets without recessions, the S&P 500 has taken an average of about 11 months to recover its prior peak. In the last two bear markets without recessions, the S&P 500 recovered in 3 months (1998) and 5 months (2011).

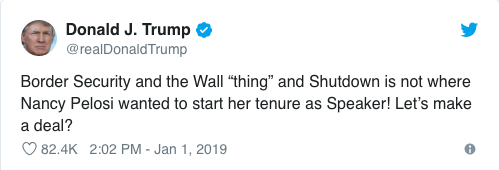

Another likely temporary factor that may weigh on investor sentiment is the continuation of the U.S. government shutdown, which enters 2019 and with seemingly no deal in sight. Democrats will take control over Congress on Thursday January 3rd and issue 2 proposals to reopen the government; neither includes funding for the proposed border wall that is desired as part of a President Trump approval.

President Donald Trump has invited eight top lawmakers to sit down Wednesday afternoon and discuss the partial government shutdown and border funding.

This would mark the first time Trump has met with democratic and republican leaders since the shutdown started Dec. 22. As reported by Politico, Trump tweeted Tuesday afternoon about the possibility of making a deal with incoming House Speaker Nancy Pelosi.

Aside from the partial government shutdown and economic data to be reported later this week, investors will be watching Friday’s panel with Powell and former Fed chairs Janet Yellen and Ben Bernanke for clues on policy moves regarding both the balance sheet and rate hike expectations. But the forum at an economists’ conference may result in very little news. In the following week, Fed minutes from the last meeting could be more informative although even the recent Fed messaging has been walked back after the negative market reaction to suggestions the balance sheet run-off was on autopilot.

Finom Group is not of the opinion a recession will take form in 2019, although permabears will give rise to this economic condition with the backdrop of the equity markets still being hobbled by the December route. The fact remains that even as economic data is expected to soften and growth is expected to slow from roughly 3% GDP to 2.5%ish GDP in 2019, this is still an economy growing right around potential. Moreover, when we look at a vast array of economic data, the data suggests expansion throughout 2019 and into early 2020.

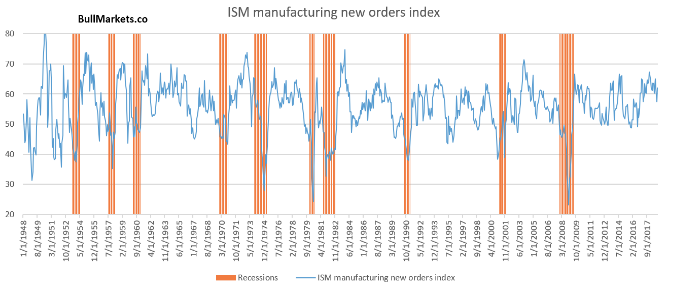

The ISM manufacturing new orders index is still relatively high, at 62.1. In the past, bear markets and recessions started when the ISM manufacturing new orders index was at 50-55, or lower.

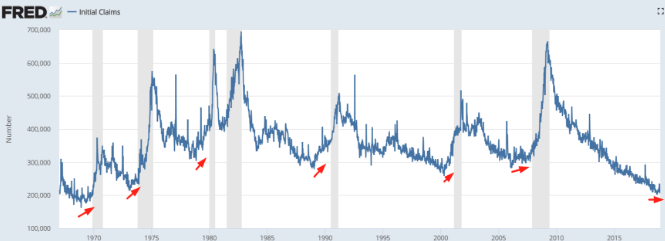

Initial Jobless Claims are very low right now (near 50-year lows), and are trending sideways. If this trends upwards in the first half of 2019, then this will be a long -term bearish sign for the stock market at that time. We emphasize long-term, not immediate and especially given a 3.7% unemployment rate, which takes time to unwind.

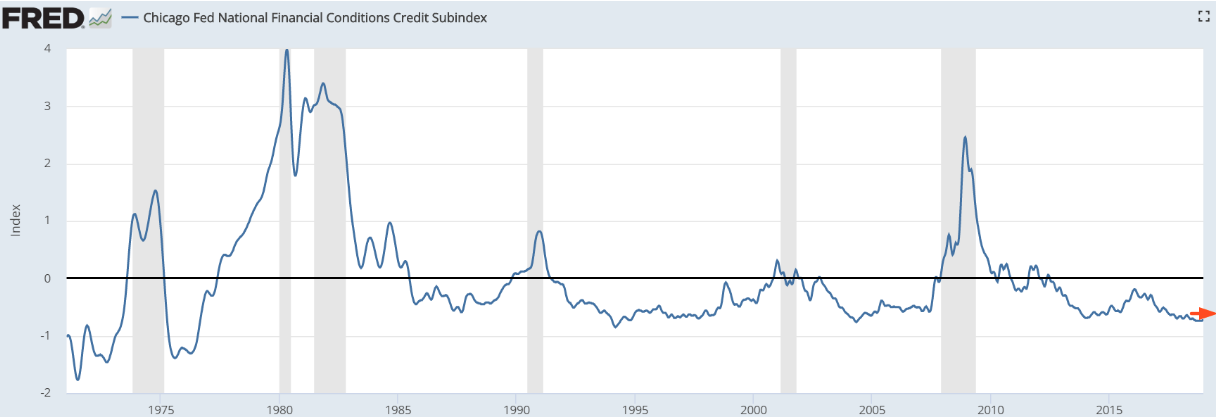

Moreover, credit has tightened. What tends to lead economic recessions is a tightening in the credit markets, lending slows. This hasn’t occurred even as equity markets have fallen. A look at the Chicago Fed’s Financial Conditions Credit Subindex has not tightened (increased) at all, even after a 20% equity market correction.

The bottom line is that there is nothing imminently pointing to a recession and as such the market will take further cues from macro-headlines and earnings, which are set to kick-off in mid-late January. Cash is king right now, but that may not last long if earnings don’t deliver the fearful results investors have baked into the current market valuation.