Yesterday’s inflation data was not received well by equity investors with the core CPI data coming in a little hotter than expected. Having said that, the 10-year yield didn’t respond with a sharp move in either direction, finishing the day at under 2.8% again. The consumer price index fell slightly in March to mark the first drop in 10 months. The CPI dipped 0.1% last month, the government said Wednesday. After stripping out gas and food, the more closely followed core rate of inflation advanced 0.2% in March. And the 12-month rate of core inflation jumped to 2.1% from 1.8%, the highest level in more than a year. The cost of gasoline fell almost 5% in March. The drop in energy prices alone is what turned the CPI negative for the first time since last May. Adjusted for inflation, hourly wages jumped 0.4% in March. They’ve risen just 0.4% in the past 12 months, however.

Surging employment and inflation data in the U.S. earlier this year had prompted some analysts and economists to predict that prices were picking up at a faster pace than markets were expecting. This caused the yield on the 10-year Treasury note to hit new multi-year highs. In February, it rose above 2.9% to a four-year high, which was partially responsible for equity markets correcting for the first time in over a year. Generally speaking, a higher yield is deemed negative for stocks, as companies have to pay more to finance their debts and investors hunt for the greatest yield with the least amount of risk.

In spite of the former surge in bond yields, the 10-year has remained stubbornly below the 3% watermark all year and since the sell-off in bonds back in February. To all of those investors fearing inflation and rising yields though Seth Carpenter, chief U.S. economist at UBS, there is no reason for concern. We are not going to break through 3% on the 10-year this year or even next year,” he told CNBC’s “Squawk Box Europe.”

“The (Federal Reserve) is now hiking interest rates,” he noted. “They want inflation to get to their target but not much above, and they’re on the case. The Fed really seems it’s going to be containing inflation, so there’s not a whole lot of need for the 10-year to sell-off.”

Yesterday’s released Fed minutes did strike a more hawkish tone than expected, but inline with the reasoning expected, economic growth. Minutes of the March 20-21 FOMC meeting showed “all” participants saw some more interest-rate hikes as likely. The minutes expressed the greatest concern on not just raising rates, but by how much and how many times in 2018. “Several” Fed officials thought the Fed might have to raise interest rates to a level that would act as a restraining factor for economic activity. Some argued that it might become necessary to signal this possibility in an upcoming statement. The minutes show a Fed that was confident in its outlook that the economy would recover from the sluggish first quarter and that inflation would move up toward the 2% target. There was a debate about the benefits of letting inflation modestly overshoot the 2% inflation target, but also about the possible risks of an overheated economy. It’s important to understand the considerations come ahead of the final Q1 2018 GDP results, which would indicate the strength or weakness of the economy. Moreover, the minutes and rate hike consideration come ahead of the all too important March PCE data, the most closely watched inflation data by the FOMC members.

As it pertains to rising rates and fear of bonds detracting investor capital from equities, there still is great consideration on the part of investors that suggests fear of geopolitical risks heightening. Investors are contending with trade war rhetoric between the U.S. and China as well as a White House with high turnover and a President increasingly in the limelight. That concern over President Trump has only elevated this week with headlines surrounding the raid on his personal attorney’s offices.

Moreover, investors will likely be glued to their televisions and streaming devices this Sunday night. James Comey will hold a featured interview on the show 20/20 with George Stephanopolus. A source told Axios that what the former FBI director had to say during that interview is “going to shock the president and his team” and “certainly add more meat to the charges swirling around Trump.” The source added that the interview included information that’s never been divulged before and left people in the room “stunned.” Comey is about to go on a promotional media blitz, according to Politico, including a live interview with CNN on April 19, a visit to MSNBC the same day, an interview on Fox News on April 26 and one with PBS NewsHour on April 30.

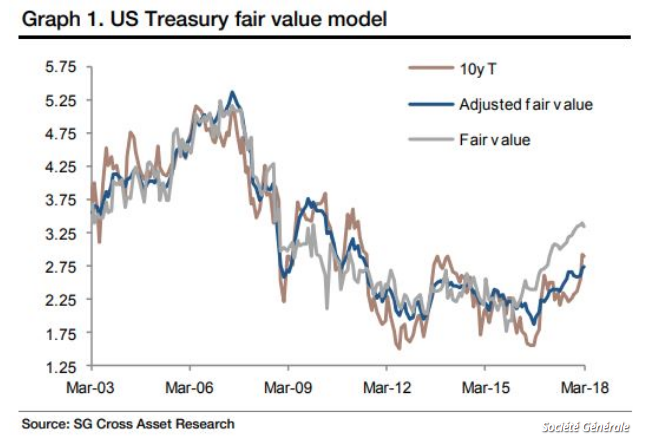

Regardless of the geopolitical headwinds that are suppressing bond yields presently, which may give way to yields surging again in the near future and as proposed by Société Générale. Analysts at Société Générale think the 10-year Treasury yield should be heading higher.

They determined that the fair value of the 10-year Treasury yield based on the U.S. economy’s current trajectory was currently around 3.30%, highlighted by the gray line, though that fell to 2.75% once the estimates accounted for the way unconventional monetary policies depressed bond yields across the world.

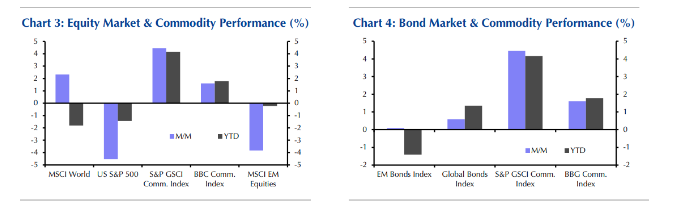

While some analysts and economists have focused on bond yields recently, others correlate the geopolitical risks with commodity outperformance. In fact, the return of geopolitical turmoil has led commodities to largely outperform equities and bonds over the last month and since the start of the year, the analysts at Capital Economics observed, pointing to the chart below:

The Bloomberg Commodity Index is up 2% in April and 1.2% for the year to date, while the S&P 500 is up 0.2% in April and off more than 1% since the end of 2017.

As we switch focus to the world of Bitcoin and cyrptocurrencies for a moment, one strategist is suggesting that Bitcoin may have seen its ultimate valuation. A strategist at Barclays speculates that demand, which pushed the value of Bitcoin and its ilk to all-time highs last year, has cooled greatly.

“Combined with the results of our theoretical modeling, survey findings suggest that, unlike the peaks in Bitcoin prices in 2011 and 2013, the most recent peak may have been the ultimate top and that speculative interest could decrease from here,” writes Barclays in a research note dated Tuesday. Past peaks in Bitcoin in 2011, early 2013 and late 2013 were followed by collapses in price of 93%, 70% and 86%, respectively, before recovering and advancing to new highs. But in each of those cases, awareness was relatively low and the potential for new entrants consequently was high. As a result, we believe the speculative froth phase of cryptocurrency investment—and perhaps peak prices—may have passed.”

Some of the issues Finom Group contend with regarding Bitcoin or cryptocurrencies valuation in general is the use case and intellectual properties. The price at which a product is sold depends on the cost to manufacture it. A product can be priced at a premium only if it requires specialized knowledge or intellectual property that prevents other market participants from manufacturing and selling an identical product. That doesn’t exist in the crypto-world. With limited technical knowledge, anyone can mine bitcoins. The real concern, however, is that if the price of Bitcoin continues to fall, mining will become infeasible, and without enough participants providing the computing power to record the transactions, the transactions will be infeasible and Bitcoin will become worthless.

In corporate earnings news, Bed Bath & Beyond shares plunged yesterday after delivering quarterly results. The retailer beat on both top and bottom-line but guidance proved to be the nail in the coffin for the share price. The home goods retailer said it expects earnings per share to be in the low-to-mid $2 range in fiscal 2018. Analysts polled by Thomson Reuters were expecting $2.73 a share, or $2.76 on an adjusted basis. Bed Bath & Beyond reported a rise in fourth-quarter net sales, overcoming a decline in comparable-store sales. The retailer earned a profit of $194 million, or $1.41 a share, in the quarter, down from $268.7 million, or $1.84 a share, a year earlier. Net sales jumped 5.2% to $3.7 billion, helped by e-commerce growth. Comparable sales fell 0.6%, beating the FactSet estimate that sales would decrease 2.3%.

Excluding the tax impact, the company earned $1.48 a share. Analysts had forecast adjusted earnings of $1.39 a share on $3.68 billion in revenue. Gross margin for the quarter was approximately 35.9% of net sales, as compared to approximately 38% in the fourth quarter of last year. Gross margins have been declining for the retailer for over 4 years now, without signs of abating. Bed Bath & Beyond shares are down 45% in the last year.

Equity Futures in the U.S. are largely higher ahead of bank earnings this morning and some economic data. Economic data and auction news will keep investors busy today. At 8:30 a.m. ET, jobless claims and import prices are both due out. On the central banking front, Minneapolis Fed President Neel Kashkari is expected to take part in a Q&A in Minneapolis with Tim Worke, who is the CEO of Associated General Contractors of Minnesota.