After 8-straight positive closing sessions, the Dow fell a little more than half a percent yesterday. Much of the blame for the near 200-point decline was attributed to the 10-yr. T-bill. The yield on the benchmark 10-yr. T-bill note early Tuesday climbed to match its highest levels since 2011 after a strong retail sales number. Retail sales climbed 0.3% in April, while the March sales figures were revised to show an 0.8% increase. Despite the positive economic data that showed continued consumer strength, investors gave more attention to the 10-yr. T-bill nearly hitting 3.10% intraday.

Fear doesn’t last terribly long on Wall Street. What may grip investors for a week or a month, generally subsides in favor of the next market-moving story. Bond yields on the rise and a threatening inverting of the yield curve has been an investor consideration for much of this year. In part, it manifested itself into a market correction and period of consolidation. A period of consolidation: This essentially means a period to digest those higher rates/yields. The digestion period simply resets the price-to-earnings clock on the S&P 500 in a period where S&P 500 earnings growth is expected to be nearly 18% for the whole of 2018. Here’s what a couple of Wall-Street veterans had to say about yesterday’s climb in the 10-yr. T-bill:

“You get up to 4 percent and we think that starts to be punitive for stocks,” Azzarello, global market strategist at J.P. Morgan Asset Management, said on “Closing Bell.”

“If you look at history, if rates go up we’re OK as long as we have economic growth, which we do right now,” he told “Closing Bell. It’s all about how steep that increase is. At this point it’s nothing to be concerned about, but certainly something to monitor.”

While some believe that rising rates at this stage of the economic cycle are justified, others think that’s a lesser consideration for equity investors. It’s always about returns on capital invested for equity investors. As such, that could prove more challenging in a higher rate regime where yields tip 3.25% at some point in 2018 or beyond. But the bottom line for Wall Street is going to center on one question: “Can bond yields and equities rise together?”

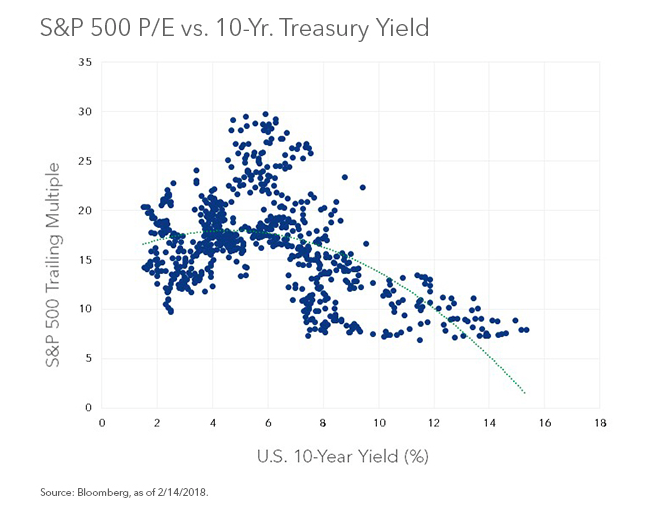

The reality is that history shows the multiple on the S&P 500 contracts for every 1% rise in rates. But history also suggests that there is a nonlinear explanation as well. Rather than a straight line, a better description of the relationship between rates and multiples is nonlinear, i.e. the relationship changes depending on the level of rates. We are definitively and inarguable in a different, all-time low-level rate paradigm. There’s at least a 30% variation in S&P 500 earnings multiples as shown in the chart below.

“Rates and multiples are more likely to rise in tandem when interest rates are rising from unusually low levels, as is the case today. Under these circumstances, faster growth is treated as a positive as it alleviates recession and deflation fears. In addition, faster nominal growth is also associated with faster earnings growth.

Unfortunately, there is a caveat. Rates and valuations can rise together—to a point. At some point the negative relationship between rates and valuations reasserts itself. In other words, at a certain level higher bond yields create real competition for stocks, particularly dividend stocks, and put downward pressure on multiples.”

It is not likely that equities will come under sustained pressure in 2018, solely due to rising yields. And if it does, it will be a confluence of issues related to the geopolitical and macro-economic picture. The key words are sustained pressure. Investors are more likely to side with a strong economic backdrop that produces double-digit earnings growth and revenue growth around 8% in favor of bonds yielding even 3.25% on average for the year. Having said that, 2019 looks more ominous for investors should yields invert and the 10-yr T-bill achieves a 4% yield. That could prove highly competitive for equities.

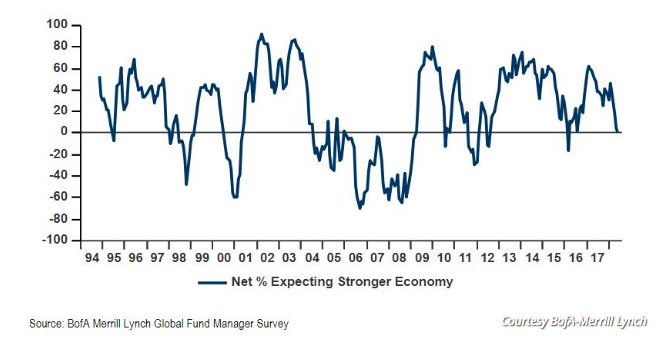

Equity markets follow earnings over time, always have and likely always will. But even with that historic and factual precedence, investors remain concerned about the economic outlook as rates and yields indeed tick higher. According to the latest BofA Merrill Lynch survey of fund managers, just 1% of those polled expect the global economy to be stronger a year from now. That is the lowest reading since February 2016. Roughly 40% of respondents said the economy would be stronger at the start of 2018, identifying a very steep drop since that period.

“Investors now are facing headlines about tariffs and sanctions, escalating Middle East tensions, equity market volatility, concerns over interest rates rising too quickly (after being subdued for years), and a few economic report disappointments. These developments seemingly have dampened the optimistic global growth outlook, said Wells Fargo in a report last week.”

In spite of the economic outlook in the BofA survey, investors don’t broadly believe the bull market is over.

More than 3/4 of surveyed investors said that equities had yet to peak. Only 19% said that late January, the most recent record for both the Dow Jones Industrial Average and the S&P 500 represented the peak of the cycle. About 42% said the peak would come in 2019 or beyond. And what is driving this particular positive sentiment concerning equities…earnings!

In earnings news, Macy’s is due to announce its Q1 2018 results ahead of the market open and will likely prove to move retail sector stocks. The median analyst estimate shows the company is expected to report $.35 in earnings on $5.39bn in revenue for the period. Both estimates are expected to show growth on a YOY basis. All eyes and ears will be focused on the retailer’s same-store-sales and gross margins. Futures are looking lower in the pre-market at 6:00 a.m. EST with limited economic data due out today.

Other than the continued rhetoric that will likely dominate media headlines near-term, investors will also listen for any new details on U.S./China trade, NAFTA insights as well as N. Korea’s possible redaction of a U.S. led summit in June. In Fed speeches, Dallas Fed President Robert Kaplan suggested yesterday that the Fed should avoid trying to invert the yield curve, and that a steeper yield curve gave the central bank more “operating room.” San Francisco Fed President John Williams said the long-term neutral interest rate was 2.5%, the rate at which monetary policy neither stimulates nor slows growth.