U.S. equity markets bounced back yesterday with modest gains across the major indices. Standing out this Thursday, the small-cap benchmark Russell 2000 index hit an all-time high of 1,620.64. The index also closed at a record, ending at 1,616.37, a gain of 16.03 points, or 1 percent. This while the 10-yr T-bill continued its sell-off, producing a higher yield. The short-dated two-year note yield, meanwhile, erased an earlier decline to eke out a rise of 0.4 basis points to 2.589% yesterday. The yield curve, as measured by the spread between the two- and 10-year yields, continued to reverse some of its recent flattening. The spread currently rests at about .50 bps.

The economic data calendar remains rather light and innocuous through the remainder of the week. With that, earnings from retailers have come into focus. Yesterday before the opening bell, Macy’s reported a much stronger Q1 2018 than analysts had anticipated. Macy’s net income totaled $139 million, or 45 cents per share, up from $78 million, or 26 cents per share, for the same period last year. EPS was 48 cents excluding impairment and other costs, and 42 cents per share excluding asset sale gains. Sales totaled $5.54 billion, up from $5.35 billion last year. The FactSet consensus was for EPS of 36 cents and sales of $5.43 billion. The company said it experienced double-digit growth in its digital business. Same-store sales on an owned basis grew 3.9%, and were up 4.2% on an owned-plus-licensed basis. The FactSet consensus was for a same-store sales increase of 0.7 percent. Macy’s said it is ending its joint venture with Fung Retailing Limited in China, but will remain active on Alibaba Group Holding Ltd.’s Tmall platform and social media channels. Macy’s e-commerce team in San Francisco will manage the China business with help from Fung Omni in Shanghai. Macy’s now expects fiscal 2018 EPS of $3.75 to $3.95, excluding the anticipated settlement of charges tied to benefit plans and other charges. This is 20 cents higher than previous guidance and ahead of the $3.61 FactSet consensus. Sales are expected to range from a 1% decline to a 0.5% increase from $24.8 billion last year. And same-store sales on an owned-plus-licensed are expected to be up 1% to 2 percent. The FactSet guidance is for sales of $24.8 billion and same-store sales are expected to grow 0.4 percent.

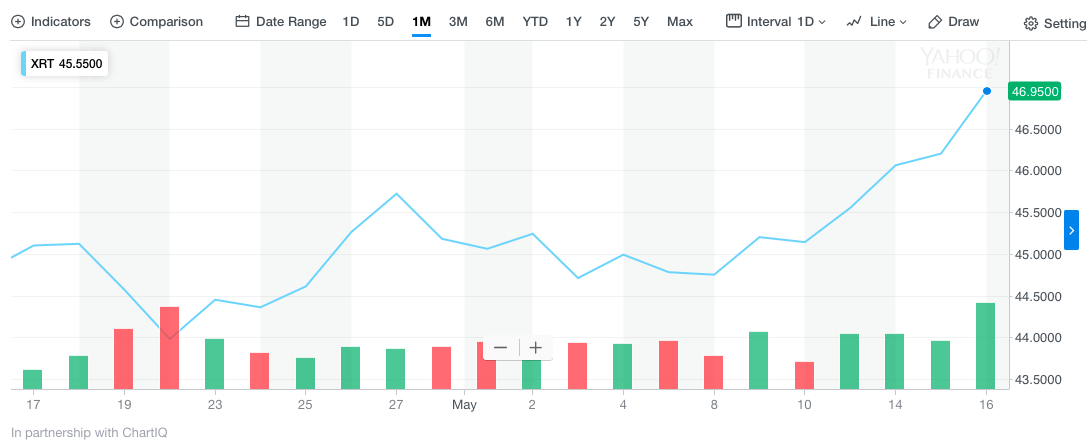

Also reporting Thursday, Wal-Mart Inc., Childrens Place Inc. and J.C. Penney Co. Inc. ahead of the bell, with Applied Materials Inc. and Nordstrom Inc. due after the close. All eyes will be on the retailers as proven yesterday with the retail index soaring in yesterday’s trade, on the heels of a strong Macy’s report that followed with strong guidance. The SPDR S&P Retail ETF (XRT) is trading at its highest levels in the last several months and surged above $47 a share in yesterday’s trading session.

Finom Group’s Chief Market Strategist, Seth Golden, highlighted the opportunity to be found in XRT a few weeks ago. Golden noted that retailers, by and large, had much easier comps in 2018 and after a dismal performance in 2017. Finom Group’s e-mail notes to clients is depicted in the screen shot below:

With a rather even distribution of holdings in the XRT, the chart was showing the possibility of a strong breakout in the ETF. Golden does not believe the current rally in shares of XRT won’t be met with a near-term pullback, but ultimately the expectation is for the XRT to achieve higher prices than where the ETF opens today.

As rates are expected to rise for the foreseeable future, investor sentiment seems to be waning. The reality is that both rates/yields and equities can and often do rise in tandem. But by how much can equities rise remains in question, especially for the major indices. Investors will find that much of the easy-market money has likely been made and stock picking may be where the future lay for greater returns.

With that being said, Morgan Stanley is becoming one of the most cautious major U.S. investment banks and calculating that potential returns for the U.S. stock market are at their lowest level since before the financial crisis.

“The firm’s view, that it “expects a choppy, range-bound equity market at the index level,” suggests that investors are in “an environment in which stock picking becomes key,” it wrote to clients.

With that backdrop, the investment bank named what it called its “30 for 2021,” a group of stocks that it recommended holding for three years. They are “our best long-term picks based on sustainability and quality of business model,” analysts wrote.

The 30 stocks on Morgan Stanley’s list are as follows:

- Accenture, Amazon, Alphabet, Activision Blizzard, BlackRock BNY Mellon, Charles Schwab, Constellation Brands, Dollar General, Dominos Pizza, Estee Lauder, First Republic Bank, Gartner, Intuitive Surgical, IQVIA Holdings, J.P. Morgan Chase, Marsh & McLennan, Microsoft, Nextera Energy, Northrop Grumman, Phillip Morris, Prologis, Raytheon, Salesforce.com, SBA Communications, Sherwin-Williams, Thermo Fisher Scientific, UnitedHealth, Visa and Walt Disney.

Another list of stocks that may prove interesting considers rising yields and dividend paying stocks from the S&P 500 stocks and these stocks all have dividend yields of 4% or higher. Here are 15 S&P 500 companies with dividend yields of 4% or higher that have not cut regular payouts since the beginning of 2007. Some may have started paying dividends more recently, but none have cut them, according to data provided by FactSet. Most of the stocks on this list have very much underperformed during this period of rising rates.

| Company | Ticker | Industry | Dividend yield | Free cash flow yield – past four quarters | ‘Headroom’ based on past four quarters | Total return – 2018 through May 15 |

| L Brands Inc. | LB, +2.64% | Apparel/ Footwear Retail | 7.21% | 7.68% | 0.48% | -44% |

| Welltower Inc. | WELL, +0.00% | Real Estate Investment Trusts | 6.35% | 7.57% | 1.22% | -11% |

| AT&T Inc. | T, +0.65% | Major Telecommunications | 6.23% | 8.69% | 2.45% | -15% |

| Philip Morris International Inc. | PM, +1.20% | Tobacco | 5.35% | 6.30% | 0.95% | -24% |

| Realty Income Corp. | O, +0.35% | Real Estate Investment Trusts | 5.09% | 5.65% | 0.55% | -8% |

| Verizon Communications Inc. | VZ, +0.15% | Major Telecommunications | 4.94% | 5.88% | 0.94% | -8% |

| Navient Corp | NAVI, +1.14% | Finance/ Rental/ Leasing | 4.58% | 28.85% | 24.27% | 6% |

| General Mills Inc. | GIS, +1.32% | Food: Major Diversified | 4.61% | 9.22% | 4.61% | -27% |

| Nielsen Holdings Plc | NLSN, +1.66% | Advertising/ Marketing Services | 4.55% | 9.33% | 4.78% | -15% |

| Qualcomm Inc. | QCOM, +1.91% | Telecommunications Equipment | 4.46% | 4.72% | 0.27% | -12% |

| International Business Machines Corp. | IBM, +0.62% | Information Technology Services | 4.37% | 10.53% | 6.16% | -4% |

| Crown Castle International Corp. | CCI, -0.28% | Real Estate Investment Trusts | 4.07% | 4.81% | 0.75% | -6% |

| Mid-America Apartment Communities Inc. | MAA, -0.37% | Real Estate Investment Trusts | 4.14% | 6.63% | 2.50% | -9% |

| Exxon Mobil Corp. | XOM, +0.28% | Integrated Oil | 4.01% | 4.17% | 0.16% | 0% |

| Source: FactSet | ||||||

With the major indices lacking true directional clarity thus far for the week, investors will look for some restabalization today. Wal-Mart’s results, due ahead of the opening bell may go a long way toward providing such stability for investors. After missing estimates for online sales in their most recently reported quarter, investors desire to see a reacceleration of online sales growth for the Q1 2018 period. Wal-Mart is expected to report earnings of $1.12 per share, according to FactSet consensus, up from $1.00 last year. FactSet analysts expect sales of $120.49 billion, up from $117.54 billion last year. According to Capital I.Q., Wal-Mart is expected to report earnings of $1.13 per share on revenues of $120.51bn.

Subscribe to Finomgroup.com and trade with us today! We’d like to hear from you, feel free to comment in the comment section below!