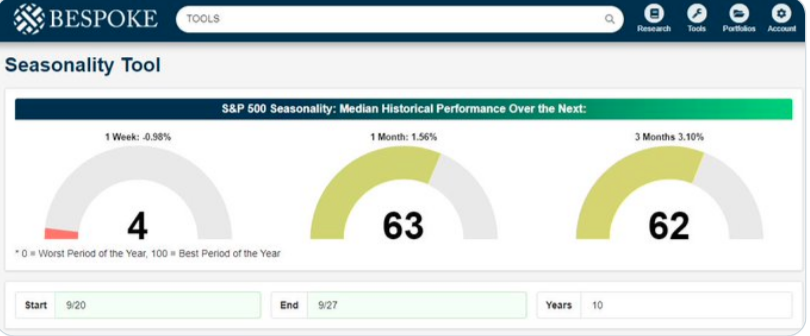

Out with September and in with October. Our recency bias might suggest that September was a rough month, but it was only in the final trading week that the S&P 500 (SPX) faltered a bit. In fact, the seasonality that presides over the indexes performance was quite precise when we look at the Bespoke Investment Seasonality Tool below:

As shown in the seasonality tool, the final week of September is historically met with just under a -1% loss for the S&P 500. That is exactly the loss the benchmark index suffered in the previous week and before Monday’s .50% rally Monday. Talk about getting it right… or maybe that’s just the algorithms being tuned to the seasonal performance. Either way, the market is holding true to trend. As such, we aim to better understand what investors might expect from the S&P 500 in the month of October, according to historical data. Before we get there, however, believe it or not, it’s been 21 years since the S&P 500 was last up 20% YTD in the first 9 months of the year? That streak has come to an end as we enter the month of October.

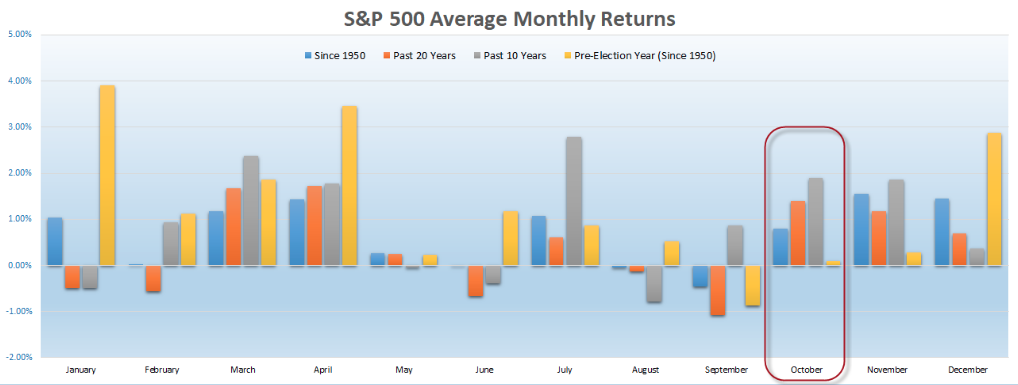

As shown in the LPL Financial chart above, the last 10 and 20-year periods have been kind to investors during the month of October. Having said that, during pre-election years, which is what we characterize 2019 to be, returns have been far less in October.

Since 1950, Octobers have averaged a slight gain of about 0.9% for the S&P 500, according to the Stock Trader’s Almanac. The data also show that during pre-election years dating back to 1950, the market has been flat with the S&P 500 posting a 0.1% return on average. October is also the month when big crashes have occurred, including 1929, 1987 and 2008.

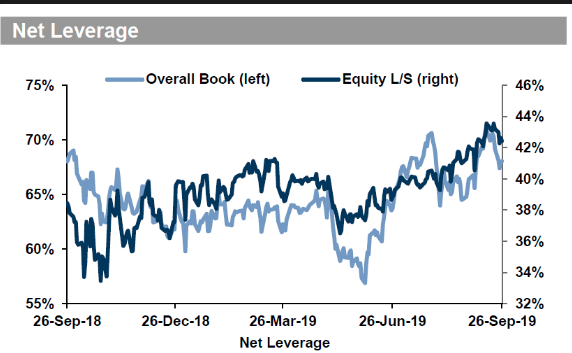

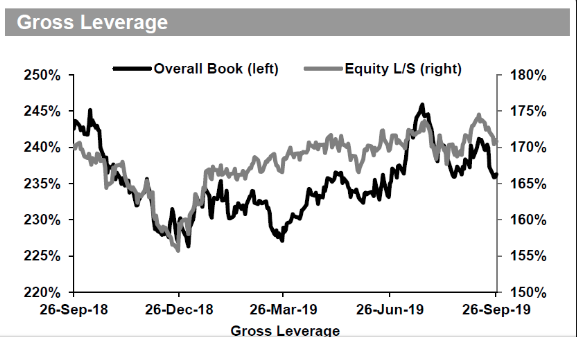

With the S&P 500 rallying 1.7% in September, investors are getting a bit nervous going forward, and reducing leverage heading into October. Both Net and Gross leverage have come down during the final weeks of September and with the S&P 500 taking losses of roughly 1 percent.

The nervousness amongst institutional investors is understandable, given the litany of domestic and geopolitical issues abound. If we were to list the potential market and economic headwinds they might look a little something like…

- Institutions have known about slowing global growth

- Yield curve inversion

- Flat to negative EPS growth

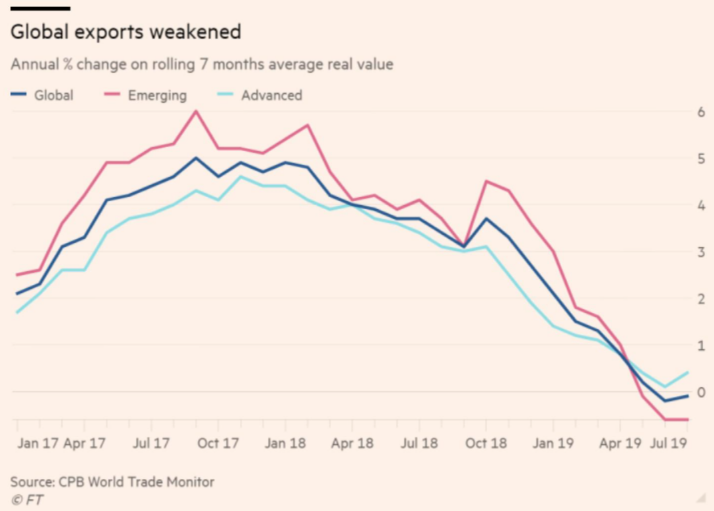

- Global trade falling

- Threat of impeachment

- No-Brexit deal

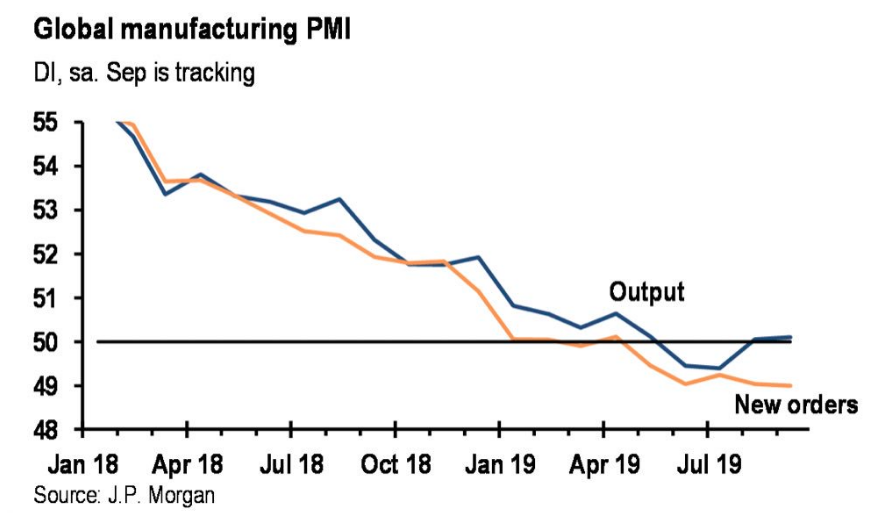

- Global PMIs falling: (JPM) “Our global manufacturing PMI has tracked this pattern of performance in recent months. Data through August point to a pickup in the global output index, but the continued decline in new orders suggests this pickup may prove transitory.”

And we could very easily add to this list of concerns noted above. One of the more pressing issues for investors also grapples with recency bias. In 2018, October is when the S&P 500 began its precipitous year-end decline, with the index finishing lower by just under 5% for the calendar year. That performance and market volatility weighs heavily on investors as we once again enter the month of October and with the S&P 500 up roughly 20 percent. And speaking of volatility…

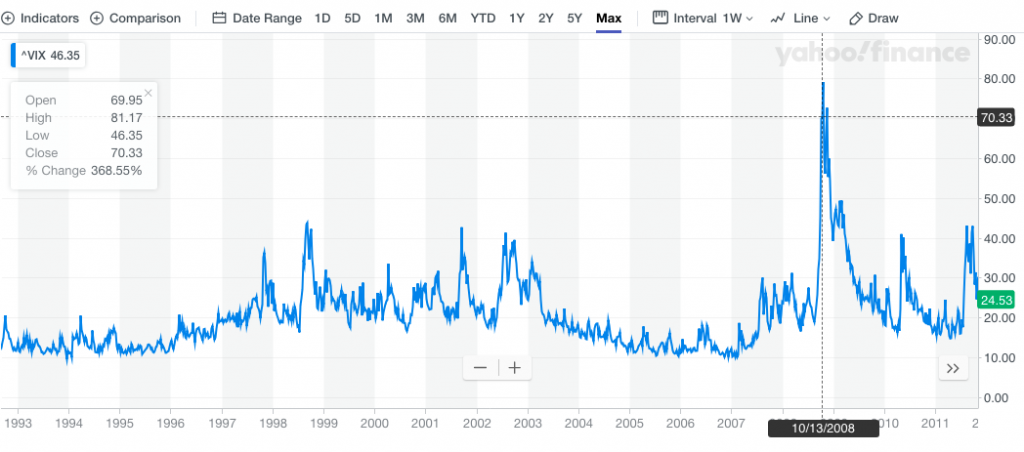

October has historically been the most volatile month of the year, as the Cboe Volatility Index, or the VIX, tends to peak in the month, jumping to more than 21 points on average over the past 30 years, according to Macro Risk Advisors. Having said that, it is important to inject the main reason for this greater than normal market VIX average reading is due to the October 2008 Great Financial Crisis fallout in the markets.

It was on October 13, 2008 that the highest closing price in history was recorded by the VIX, at 70.33 and with an intraday high of 81.17. If we extrapolate this anomaly from the data set, the market would have a much lower VIX average for the month of October.

“We’ve been spoiled by the lack of volatility this month, and it increases the chances of a little more explosive October,” Ryan Detrick, senior market strategist for LPL Financial, told CNBC. “One thing we know is the markets don’t stay calm forever and we’ve seen that multiple times this year.”

With impeachment and trade headlines creating market gyrations daily, we would anticipate this October to be little different than the historic precedence suggests. It should be noted that the all too-critical U.S./China trade talks/negotiations will unfold in early October and will prove either to the benefit or detriment of equity markets. We would also anticipate a higher VIX going into the trade talks, as investors will probably hedge their portfolio, should trade talks breakdown.

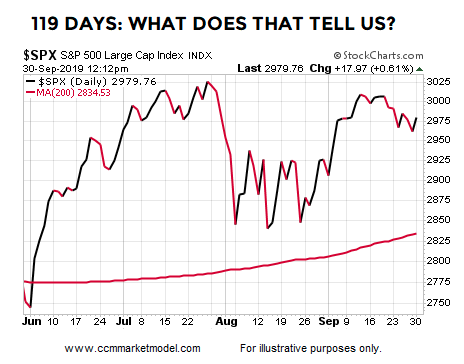

Technically speaking, the market is in pretty good shape as we commence October trading. The S&P 500 is above all of its key moving averages, but with a gap that remains open from 2,957-2,939. Additionally, the benchmark index has not revisited its 200-DMA in 120 days now. (Chris Ciovacco)

Much of September was found with net equity inflows until the final trading week, helping to support the S&P 500 in maintaining the index above the major moving averages. Pension funds began to rebalance at the onset of September and are expected to perform some final quarter rebalancing as October commences. According to Morgan Stanley QDS Pension Rebalancing Model, they estimates that there will be $16bn outflows from equities into bonds from pensions through the first week of October. $16bn outflows from equities is the 39th percentile since 2005. Flows are estimated to be spread over the next two weeks. With such forecasted outflows, investors will have to wait to see if there is an equal or greater offset, as we also enter the all-important Q3 earnings season.

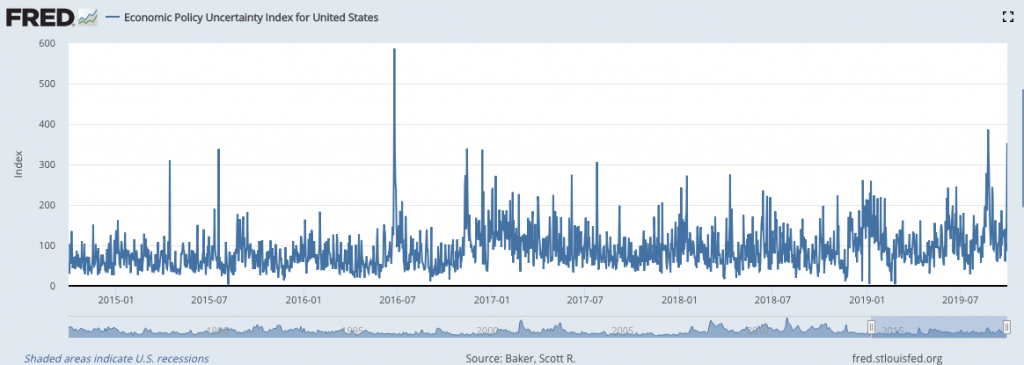

Given everything investors are considering in the way of headwinds for the market entering the Q4 2019 period, it’s no wonder outflows have been persistent throughout 2019, but the reality is that outflows have been present since 2017 and shortly after the Trump Administration came into office. We can rationalize these outflows against the concerns for economic policy. With a 14-month trade feud that has, in part, caused a global economic slowdown and growing Federal deficit, it’s no wonder economic policy uncertainty has achieved highs not seen since the period leading up to the U.S. presidential election.

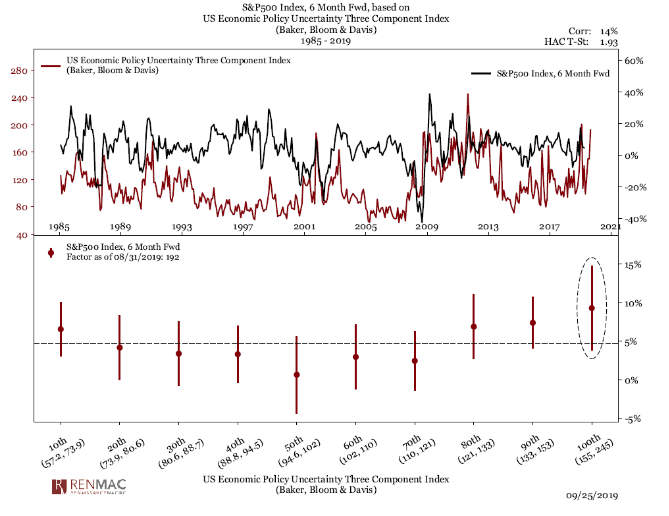

But could economic policy uncertainty be a good thing for investors and S&P 500 returns? That’s the question being answered by Renaissance Macro in the following chart comparison. The firm recognizes this study may be even more relevant today with a looming impeachment process under way.

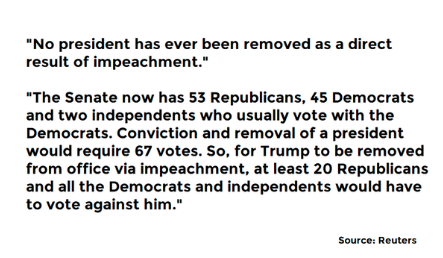

Policy uncertainty is historically bullish for stocks, cites Renaissance Macro. They place the odds of the Senate convicting Trump at just 18 percent. Keep in mind that even if Congress votes in favor of impeachment, for Trump to be removed from office via impeachment, at least 20 Senate Republicans and all the Democrats and independents would have to vote against him. That’s a tall order folks, as outlined in a recent Reuters article:

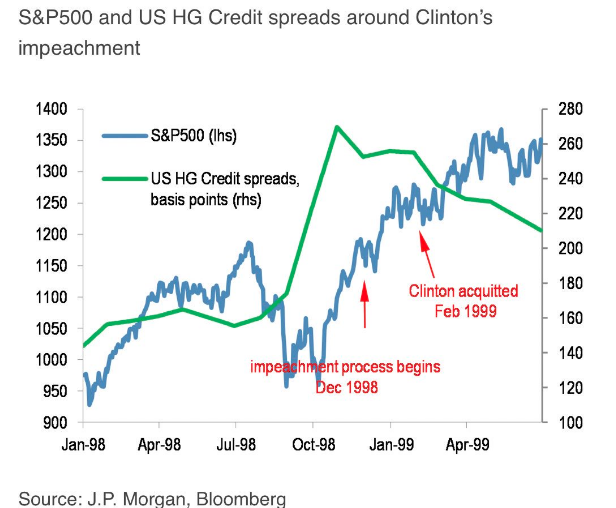

J.P. Morgan Chase isn’t altogether concerned about the impeachment process underway. The firm suspects “that an impeachment that ends without conviction by the Senate and with the president still in office would have only modest effects on .. macroeconomic risks. It would likely require a deeper sense of constitutional crisis to produce a larger .. impact.” The firm also offers the following analysis and charts:

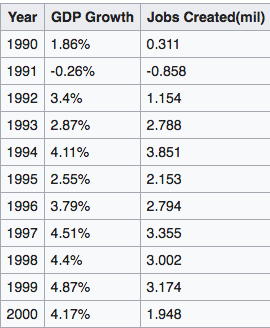

While the more recent Clinton impeachment process doesn’t suggest investors should be overtly concerned about the fallout from the global economy, the economy is at a far different stage than it was back then. During the Clinton impeachment process of 1998, the U.S. economy was growing above 4% and found creating more than 3 million jobs.

That’s just not the case today, and President Trump is not President Clinton, for better or worse and in the eyes of the beholder so-to-speak. With all that being said concerning the macro-concerns heading into October and with earnings season on deck, investors will turn their attention to the daily economic data releases.

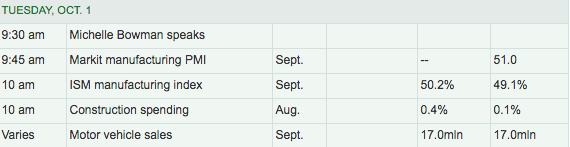

The focus Tuesday will shine a spotlight on U.S. manufacturing and through the ISM Manufacturing Index. After falling into contraction territory in August, economists are looking for a rebound to have taken hold in September. Certain of the regional PMIs have come in better than forecasted during the month of September already, even if order growth has slowed.

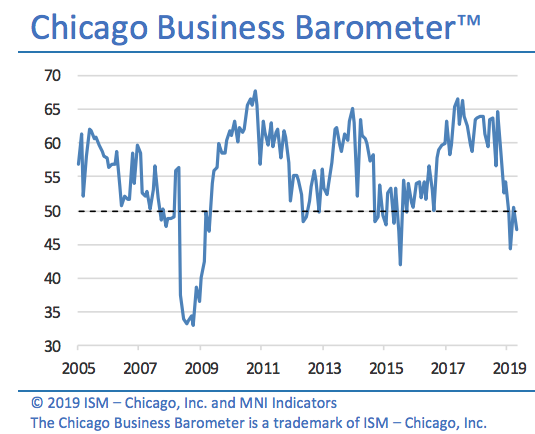

Two regional PMIs were released just yesterday, painting opposing situations. The Dallas regional PMI came in better than anticipated, but that was not the case with the Chicago PMI data.

The Chicago PMI business barometer dropped to 47.1 in September from 50.4 in the prior month, MNI Indicators said Monday. Wall Street had expected a reading of 50. The barometer averaged 47.3 in the third quarter, the lowest level since the U.S. exited recession in the middle of 2009. The weakness in the Chicago PMI is reflecting ongoing struggles by American manufacturers as well as the two-week-old General Motors workers strike.

Finom Group is of the opinion that the upcoming release of the ISM Manufacturing Index will prove market moving. We also remain of the opinion that an uptick in manufacturing will be revealed. If proven wrong, it wouldn’t be the first time, but as a percentage of the U.S. economy manufacturing is not our key concern or focus. The consumer is the focus for us, as the consumer drives some 70%+ of economic activity in the United States.

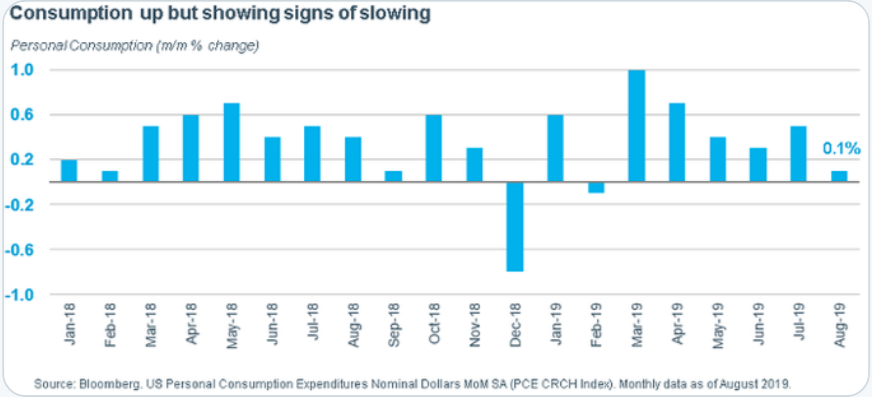

Consumer spending rose just 0.1% last month, the government said last Friday and within the latest Personal Income and Expenditures report (PCE). This marked the smallest gain in six months. Economists polled by MarketWatch had predicted a 0.3% increase. It should be noted, however, that the slowdown in spending came alongside strong income growth for the period.

Incomes rose 0.4% for the fifth time in six months, but most of it ended up in savings. The savings rate climbed three-tenths of a percent to a healthy 8.1 percent. We’re quite okay with a responsible consumer that is better served with improving wages. Keep in mind that July was a strong spending month. Consumers simply pared spending after splurging in July, when Amazon held its massive Prime Day sale and rivals offered their own sales/discounts. Additionally, we suspect that some back-to-school shopping was pulled forward into July due to the retail discounting events. Outlays rose a revised 0.5% in July.

Hurricane Dorian may also have crimped spending in August in parts of the Southeast, which tend to express a large percentage of national retail spending. Another potential depressant was President Trump’s announcement he would raise tariffs on China, which caused a temporary plunge in U.S. stock markets.

Equity futures are on the rise ahead of the key economic data releases for Tuesday, as bond yields are following suit. After investors receive the ISM Manufacturing data, they will likely move on to the next data point to be released Wednesday, the ADP private sector payroll report. From there, the Nonfarm Payroll report comes into question and with a great deal of anticipation, as slowing job growth in 2019 has cast doubt on the duration of the current expansion cycle. And if all go swimmingly from the data this week, next week investors will move to the next worry/concern, trade talks. As usual, Morgan Stanley has nothing but positive things to suggest about those upcoming talks.

Morgan Stanley say tariff increases scheduled to go into effect on Oct. 15 on $250 billion Chinese goods are likely to go ahead. They point out that past meetings at the negotiator level have been followed by tariff increases, not de-escalation.

“It’s hard to know exactly why, but we suspect it’s because meetings have typically not resulted in material progress on the core disagreements between the U.S. and China on enforcement of a deal,” they said in a note to clients.

The analysts don’t expect a full deal anytime soon, though they say a “durable pause” is a possibility, with the two sides formalizing existing areas of agreement but deferring the core unresolved issues to future discussions. The other possibilities are sustained escalation, or another “uncertain pause,” where the two sides make minor concessions and keeping talking.

UBS’ Axel Webber isn’t as sanguine as Morgan Stanley, as it pertains to the upcoming negotiations.

“What we’re interested in is the long term developments and whilst there is a big dispute at the moment, I think there’s also potential for resolution. And the potential for resolution lies in the very fact that trade is really beneficial to both sides. The two countries could reach “an agreement that will sort out certain developments” and leave other sticking points for further negotiations.“

Lance Roberts of Real Investment Advice believes a deal is in the offering at the upcoming meeting. Much of the forecasted deal simply moves the goal posts back to the beginning of the trade war and with China buying U.S. agricultural goods, which is what they had been doing in the past. It’s a deal to recapture the status quo, but still allows for President Trump to propose a win with his voting base.

“The pressure is on the Trump Administration to conclude a “deal,” not China. Trump needs a deal done before the 2020 election cycle; AND he needs the markets and economy to be strong. If the markets and economy weaken because of tariffs, which are a tax on domestic consumers and corporate profits, as they did in 2018, the risk of electoral losses rise.

China knows that Trump needs a way out of the “trade war”he started, but that he needs a something that he can “boast” as a victory to a largely economically ignorant voter base. Here is how a “trade deal”could get done.

Understanding that China has already agreed to 80% of demands for a trade deal, such as buying U.S. goods, opening markets to U.S. investors, and making policy improvements in certain areas, Trump could conclude that “deal”at the October meeting.

“Not surprisingly, as Trump said on Thursday, while he prefers a broad deal, he left open the possibility of a more limited deal to start.” – Reuters

Only time will tell, but with all the impeachment headlines swirling around that pose a personal disgrace to President Donald Trump, the White House Administration indeed needs some type of win. While he might be able to brag about having the better economy on an otherwise bad “global economy block”, it doesn’t appear as though the economy is strengthening on a YoY basis, not yet at least.