The U.S. economy is like a ship trying to navigate its way through difficult waters, JP Morgan Chase (JPM) chief Jamie Dimon said Wednesday. I would tend to agree with Jamie if not for the prolonged government shutdown, which hits its 34th day of being closed and with seemingly no end in sight. And this is not to say that Jamie Dimon isn’t recognizing the adverse affects to the economy that have and will continue to come from the government shutdown.

“The U.S. economy is kind of like a ship that’s going it’s going, ex- the shutdown 2 to 2.5 percent and that’s going to keep going for a while,” Dimon said. “Then you have all this other noise, geopolitical noise, Brexit noise, what’s the Fed going to do, … shutdown, trade. They’re kind of buoys in the water in front of that ship. Eventually that may very well cause a slowdown or a recession.

I don’t know 2020 or 2021, but the range of possibilities is broader and the range of bad outcomes is increasing.

If politicians fix things that are broken, GDP could grow consistently at a 3 percent rate.”

In addition to Jamie Dimon’s comments on the U.S. economy, Dimon also told CNBC he thinks the U.S. and China will reach an interim agreement before the March 2 deadline to end their tariff cease-fire. Other country’s are echoing Dimon’s comments and pleading with both nations to make a deal near-term as it is or could impact their own country.

Germany’s Economy Minister Peter Altmaier underlined the risks to his country’s own economy if a trade conflict between the U.S. and China is left without a resolution. Altmaier noted a recent slip in German growth, but insisted the country was in a “solid, sound condition.” Nonetheless he noted that the “looming conflicts” between China and the U.S. could be damaging for his country and the wider European Union (EU).

The common theme at Davos this year is one of geopolitical tensions bringing about a global economic slowdown. The genesis of the slowdown is blamed, to a great degree, on geopolitical tensions that have resulted in tariffs and other protectionist policies. Piling onto the geopolitical tensions and protectionist policies are individual country/nation politics. The U.S.’ longest government shutdown is just one example of domestic political deterioration that is creating clouds over individual economies across the globe. One might say, the U.S.’s domestic political turmoil is only usurped by that of the United Kingdom’s Brexit situation.

The only benefit from the geopolitical landscape that is littered with strife and tension is that it helps aid the FOMC’s dovish stance in 2019. The Fed has all but stated it will not raise rates for the foreseeable future and with inflation firmly beneath its 2% target objective. While the Fed’s employment mandate has been achieved, that element of the Fed’s mandate is overcome by slowing economic growth, identified with the Fed also lowering its outlook for economic growth at it’s last meeting. GDP is now seen as rising 3% for the full year of 2018, down one-tenth of a percentage point from September, and 2.3% for 2019, a 0.2 percentage point reduction. However, officials took up their long-run estimates, to 1.9% from 1.8% in September.

So why am I discussing the Fed and geopolitics so much this Thursday morning? Well, of course it is due to the first European Central Bank policy meeting of 2019 that will conclude today. The ECB is widely expected to announce no new actions when it concludes its meeting on Thursday. The central bank has already declared that rates won’t be lifted until at least the end of summer. In December it ended its monthly asset purchases, the ECB’s version of quantitative easing, or QE, while committing to maintaining the size of its bulked up balance sheet by reinvesting the proceeds of maturing bonds.

Investors and policy makers around the globe will likely be paying attention to the portion of Draghi’s opening statement dealing with the ECB’s assessment of the risks to the eurozone economic outlook, which in central bank verbiage are described as being either skewed to the upside, balanced, or skewed to the downside. In December, Draghi acknowledged that risks to the economy were moving to the downside but could “still be assessed as broadly balanced.”

When it comes to the eurozone’s economy, it’s no secret that the region has and continues to express a slowdown. Data firm IHS Markit said its composite Purchasing Managers Index, a measure of activity in the manufacturing and services sectors, fell to 50.7 in January from 51.1 in December, its lowest level in five-and-a-half years.

“Speaking [Thursday] — in the shadow of the World Economic Forum, which is obsessed with mounting evidence of a slowing global economy, slowing world trade and other dark subjects — we expect President Draghi to finally mouth the words, ‘The eurozone economy is slowing,’” said Carl Weinberg, chief international economist at High Frequency Economics, in a Wednesday note.”

There is simply so much either negative or uncertain geopolitical conditions looming. And all this as investors struggle through the all-important earnings season. Credit Suisse’s top strategist told CNBC on Wednesday the one thing that he is most concerned about as markets stage a comeback.

“There’s total inconsistency in the underlying earnings data. The revenues are knock-the-lights-out good, and the margins are horrifically bad, based on Wall Street consensus expectations.”

The current market theme, as it pertains to equity markets, is muddied by the geopolitical picture and our own domestic political turmoil said Jonathan Golub. It’s hard to get your hands around the earnings picture with all the geopolitical and domestic turmoil. Earnings are coming in better than expected, but headline risks are elevated given the following:

- U.S./China trade negotiation deadlines edges closer

- Brexit or No Brexit edges closer

- Ongoing U.S. government shutdown is prolonged

With the aforementioned geopolitical risks posed to the global economy, equity markets and investors, let’s round out today’s daily market dispatch with some follow-up thoughts on Brexit and the United Kingdom. Prime Minister May is negotiating with opposition and coalition parties since the failed Brexit vote that was widely anticipated. She is attempting to strike an amended deal. At this point, it seems increasingly difficult to envision a cross-party agreement, a “soft Brexit” and I’m skeptical that any deal will be struck by the March 29 deadline. A more likely second referendum, a hard Brexit (leaving without any deal), or regime change remain options and the path forward.

When we examine the size of the U.K.’s economy, it amounts to a very minute size of the global economy and only a slight piece of the global trade picture. The U.K. constitutes only about 2% of the global economy and 4% of world goods trade; so global ramifications of all realistic scenarios are likely to be limited and manageable. Having said that, like the first Brexit vote back in 2016, markets are likely to react most negatively if a hard Brexit is realized. Economic forecasting firm Capital Economics thinks a disorderly exit could cause a 1–2% hit to British GDP growth, spread over two years.

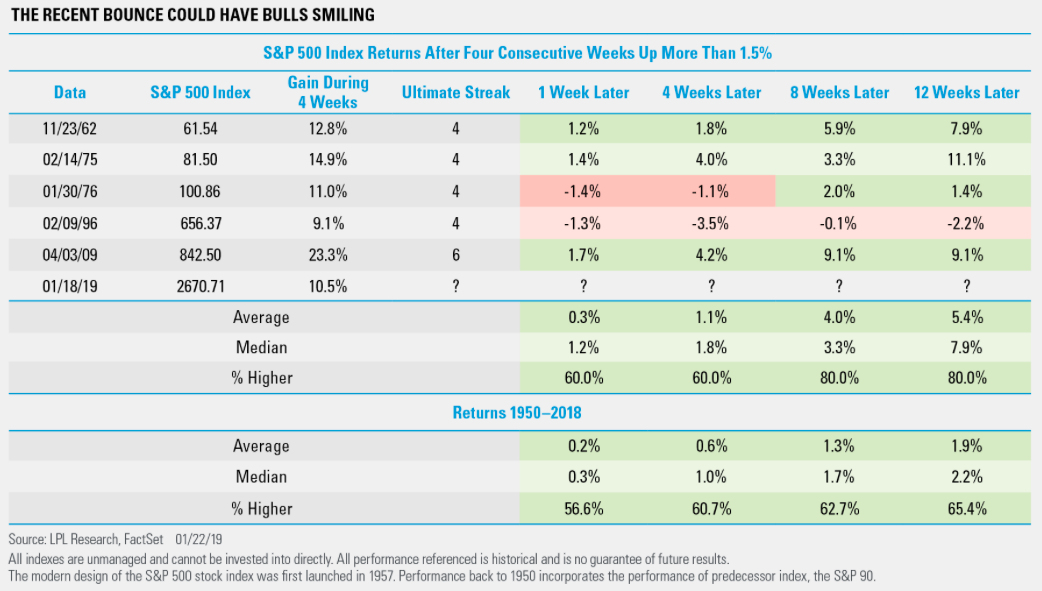

Despite the onslaught, continuous, littering and looming headline risks from around the world, equity markets have rebounded in early 2019 and alongside better than expected earnings reports. After a greater than 1.2% drop in the S&P 500 on Tuesday, markets rebounded a bit on Wednesday on those better than expected earnings. The S&P 500 has gained 2.9%, 1.9%, 2.5%, and 2.9% over the past four weeks for a total gain of 10.5 percent. Given the 4-week performance I wanted to take a look back at historic performances of the same kind to see what followed such results. History also tells us that being up more than 1.5% for four consecutive weeks actually tends to see continued outperformance going out the next three months.

The chart above from LPL Financial suggests a market pullback over the next 1-4 weeks has a 40% chance, but markets could surge higher over the following 8-12 weeks. Since 1962, when the S&P 500 has been up 1.5% or more for 4 consecutive weeks, it has gone higher 8-12 weeks later nearly 80% of the time.

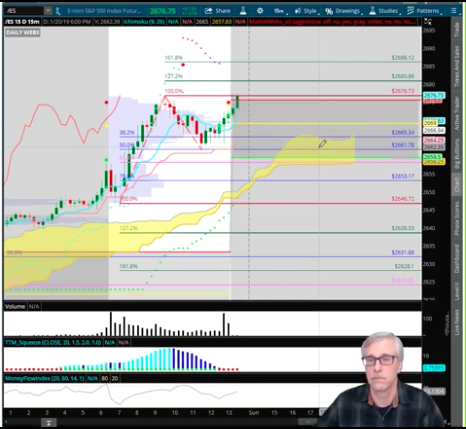

It’s easy to get caught up in the market’s trend, be it to the upside or to the downside. Many investors and/or traders got caught up in the downside momentum during the Q4 2018 period. Some left the market altogether as the seemingly never-ending selling pressure surmounted before culminating on Christmas Eve. Here in 2019 and with market momentum having greatly shifted to the upside, I encourage readers to remain objective and with a long-term view of investing. Traders would benefit more from limiting market exposure and therefore limiting risk as the market has maintained an extended move to the upside and now resides within a zone of resistance. The following chart comes to us from Nigam Arora, MarketWatch columnist and analyst.

- The chart shows that the market is in the resistance zone.

- Volatility in the resistance zone is normal.

- The chart shows that the market has not decisively broken the down trend line.

- The chart shows that an overbought condition has been temporarily relieved and this potentially sets up the market for a rally after a brief pullback.

- Volume has stayed relatively low during the rally. This is a negative.

While the S&P 500 is certainly in the resistance zone, something we’ve called the S&P 500 BOX for the last few months (2,800-2,581), the market can break either way. It can break to the upside or to the downside. Given the consistent reduction in earnings forecasts that have evolved through the present earnings season, the greater likelihood for the market is to express a near-term pullback. To what degree we can not be sure, but this week’s S&P 500 price action may be setting up investors/traders for such a pullback and as the S&P 500 seemingly struggles to move higher entering Thursday’s trading session.

As depicted above, earnings will continue to pour into the market on Thursday. After the closing bell we’ll here from Intel Corp. (INTC) and Starbucks (SBUX). Next week will find the tech sector in the spotlight, as several tech titans will be reporting. Results from the tech sector may prove to define whether the market will continue to trek higher or pullback.

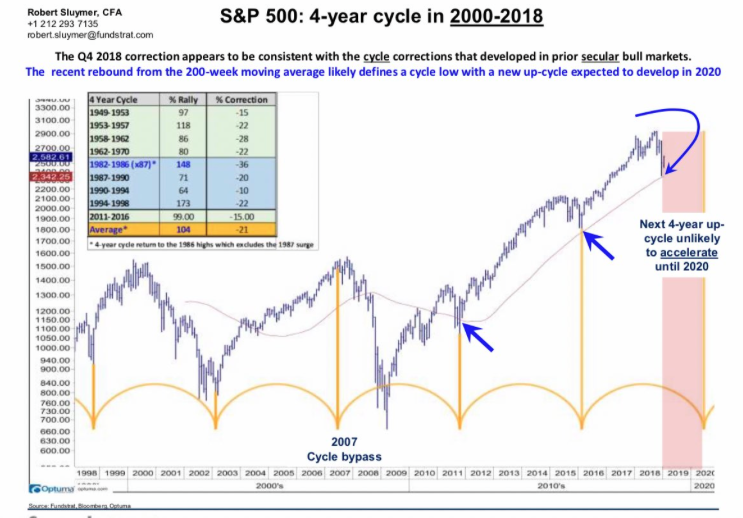

Every cyclical bull market has its version of a secular bear market. With this in mind, our chart of the day comes from Fundstrat’s Robert Sluymer, CFA. He is of the opinion that the recent bear market and corrective phase conditions yet to run their course in 2019 will ultimately set the market in motion and for the next leg higher in 2020.

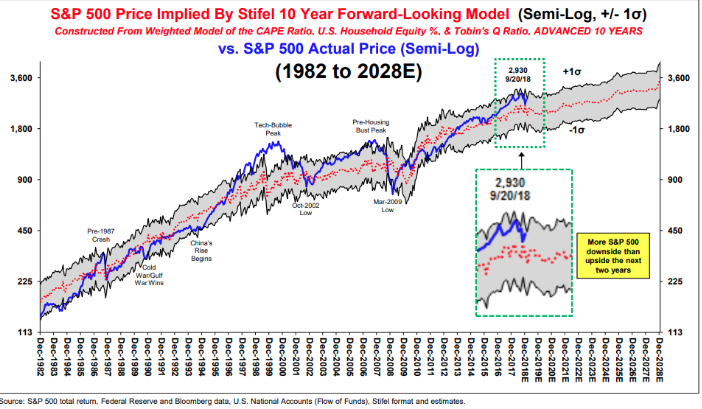

Sticking with what is happening here in 2019, however, earnings will prove to guide the market and through the geopolitical cycle. Until the current earnings season has completed and we have the full scope of what earnings forecasts are for 2019, some analysts remain somber and fearful of what may come for earnings in 2019. Stifel’s Bannister cut 2019 S&P 500 target to 2,750 earlier this month.

“Our 2,750 S&P 500 target is at risk due to the deep EPS ‘valley’ ahead,” said Barry Bannister, head of institutional equity strategy at Stifel, in a note, stressing that the slowdown in earnings growth will be much more acute than investors anticipate.”

Bannister is projecting 2019 earnings per share of $165, below Wall Street’s average of $170, and expects more companies to guide lower in the future due to slowing global economic growth.

The pessimistic tone on Wall Street is rational given the geopolitical and domestic political uncertainties and struggles. But as we’ve said many times before, what man has done, can be undone! And with that, we encourage readers to click the link to view last night’s technical Market Recap brought to you by Finom Group’s Wayne Nelson.

Also stay tuned this evening for our subscriber exclusive, early release of Finom Group’s State of the Market video.