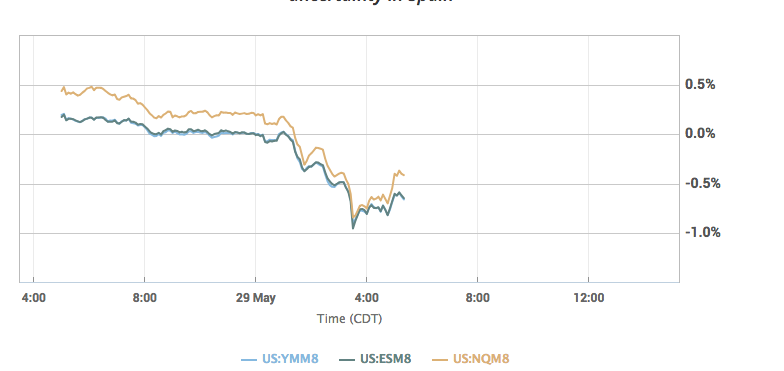

If you just waking up after a long Memorial Day weekend and seeing U.S. equity futures sharply lower, it’s time to get to work. U.S. equity futures are down almost ¾ of a percent on concerns about the potential for another Italian election within a few months.

In particular, they’re worried a win for populist parties could lead to the euro zone’s third-biggest economy leaving the shared currency, which would represent quite a shakeup to Europe’s status quo. Here is how the 5 Star and League leader Matteo Salvini is framing the political situation in Italy

“It won’t be an election,” Salvini said Sunday, according to a Wall Street Journal report. “It will be a referendum between Italy and those on the outside who want us to be a servile, enslaved nation on our knees.”

Opinions vary concerning the Italian political situation and whether or not risks are currently priced into the global equity markets. Investors desire clarity on the situation as Italy represents a large European economy with soaring bond yields.

“Even an Italian populist government’s failed attempt to ditch the euro would bring a halt to not only the ‘euroboom,’ but also the process of U.S. monetary normalization, with the market reaction comparable to the eurozone debt crisis,” Oxford Economics analysts Jamie Thomson and Nicola Nobile said in a recent note.

“Personally, I don’t think Italy will leave the euro,” said Marshall Gittler, chief strategist at ACLS Global, in a note Tuesday. “According to the European Commission’s Eurobarometer survey, support for the euro in Italy has never been below 58%, and most recently was 59%, with only 31% opposed.”

Regardless of which side of the argument will be found right, equities around the globe are pricing in risk, assuming a negative outcome, even prior to any insights coming from the European Central Bank leaders. The underlying issue regarding the political uncertainty in Italy is the desire for the opposing political parties to….spend, spend, spend. The antiestablishment 5 Star Movement and far-right League disagree on many issues, but both are calling for expansionary spending that would ignore the European Union’s deficit rules. These measures are setting up a confrontation with Brussels and its eurozone partners. The desired spending from both sides of the Italian political spending is what has Italian bonds soaring in the last week, which has carried over into today’s trading with the Italian 10-yr bond up nearly .43 basis points to over 3.10 percent.

While a layer of panic is setting into European equity markets presently, creeping into U.S. equities to a lesser degree, this geopolitical concern of the day is likely to pass relatively quickly. Here’s why: ECB’s Outright Monetary Transactions program. The OMT program was assembled after Draghi’s famous 2012 pledge to do “whatever it takes” to preserve the euro. Never used, OMT allows the ECB to make purchases of government bonds issued by eurozone countries in the secondary market once a government requests assistance. Draghi’s pledge and the promise of the OMT program were credited six years ago with pulling Italian yields down from crisis levels that had seen the yield on two-year government paper spike above a fiscally unsustainable 7.5 percent.

There are actually a host of reasons as to why the current political issues resounding in Italy are unlikely to find global equities under pressure for a sustainable period. The ECB’s other bond-buying program has dragged down government and corporate yields across the eurozone. This means Italy’s debt-service costs should minimally increase even as yields rise. That’s because the average yields are still far lower than the average outstanding coupon. Because of the ECBs bond buying activity and dominance in the space, only 32% of Italian government bonds are still held by foreign investors and only a third of those are held outside the eurozone. That compares with more than 40% before the sovereign debt crisis. Additionally, the ECB’s deposit rate stands at negative 0.4%, while its key lending rate stands at 0 percent. Rates aren’t expected to rise in the near-term and that’s curbing the rise of short-term bond yields. It also means Italy will be able to issue new bonds with low coupons, which should anchor long-end yields. Italy’s Treasury has enough cover to shift its issuance back toward shorter-dated maturities if deemed necessary.

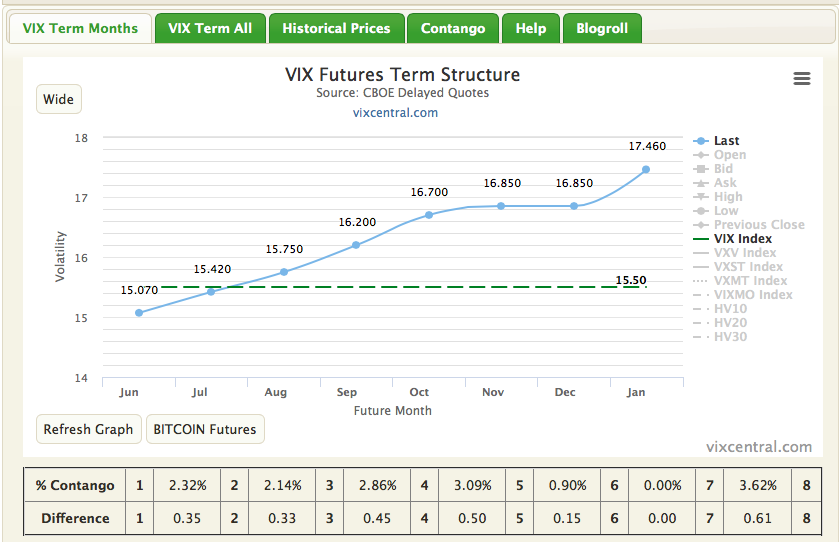

It’s a risk-off day thus far around the globe, which is finding gold, U.S. treasury yields and oil following equity prices lower. The risk-off event is coming with a decent amount of volatility as the VIX is presently up above 15.50 or roughly 17% in the 7:00 a.m. hour.

VIX Futures are still representing contango across the term structure although much of contango has been reined in with volatility surging. Given the geopolitical circumstances largely will show minimal if any impact on the U.S. economy, Finom Group would expect volatility sellers to take advantage of this spike in volatility near term.

U.S. investors will likely monitor the European markets right up until their closing later today, taking their lead from the Union. Later this week, investors will refocus on economic data releases coming in the form of ADP private payrolls and Nonfarm Payroll data to wrap up what is already proving to be an excitable week of trading.