After sideways action in the markets for the first two trading days of the week, the markets may have picked a direction on Wednesday, well at least for the Dow Jones Industrial Average. The Dow finished higher by .61% on Wednesday, but the Dow’s rally didn’t provide leadership as the S&P 500 rose a scant .13% and the Nasdaq fell by .08% on the trading session. It’s been quite clear over the summer months and into the fall that sector rotation has been moving markets up and down, but ultimately finding new all-time highs for the major averages. All but the Dow has yet to achieve a new record high.

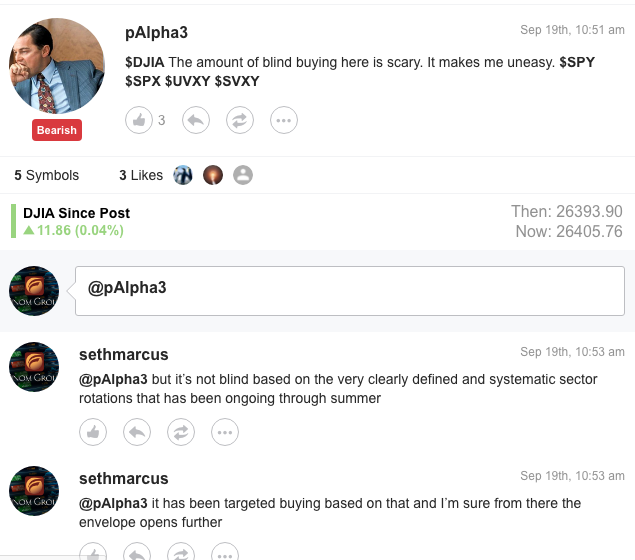

In a recent post on StockTwits, a participant stated that investors were blindly buying the market and it made the trader uneasy. Finom Group’s chief market strategist, Seth Golden, often participates in social media and on StockTwits and countered the commentary by stating the following:

“But it’s not blind based on the very clearly defined and systematic sector rotations that has been ongoing through summer.”(See screenshot below)

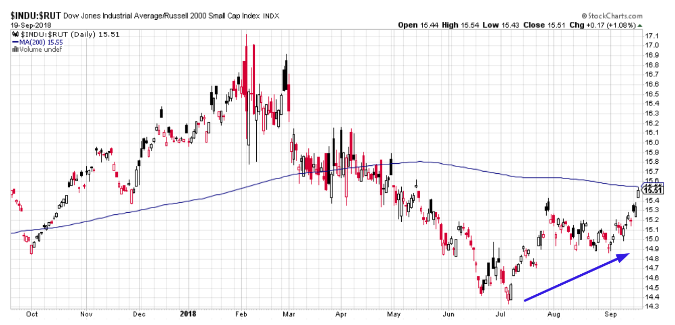

We don’t like to make assertions without offering evidence of such assertions. As such, a couple of charts identify the longstanding Dow, large cap (Industrials) underperformance with respect to small caps or the Russell 2000 small caps as follows. Again, this known as sector rotation from within tech, industrials, financials, consumer discretionary et. Cetera.

The above chart of the Dow:Russell ratio is on the verge of closing above its 200-day moving average for the first time in approximately 5 months. In other words, the Dow has underperformed the Russell for a long time, and this underperformance is coming to an end. That’s how sector rotations work and such market activity is yet another sign of a healthy bull market. The following chart may help traders, well, trade into the Dow’s strength and the probability that the Dow and/or the industrials hit a new high.

The above chart is of the 1-month Industrial Select Sector SPDR ETF (XLI)’s performance. As one can clearly see, the XLI has broken free of its slump and looks to be on the verge of recapturing its January highs. This may prove a good short-term trade for folks to participate with, although the strength in the XLI may brush up against rate hike angst next week.

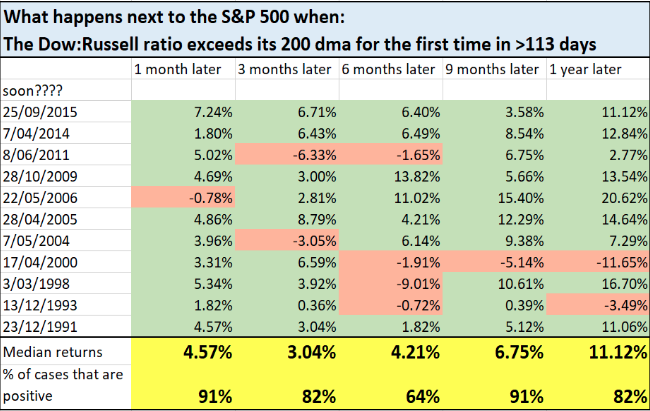

Bullmarket.com’s Troy Bombardia offers our last table. The table identifies what happens to the S&P 500 after the Dow:Russell ratio is on the verge of closing above its 200-day moving average for the first time in >113 trading days.

With respect to social media, be careful what you hear and see out there and always relate what is stated with how markets work. Markets follow earnings, not how long a bull market has lasted or how quickly it has risen or even sentiment from time to time. This is not to suggest markets can’t be roiled by fears surrounding the yield curve, reflation, geopolitical pressures and the like, but if the aforementioned don’t’ curtail the earnings outlook, the markets will eventually rebound to express over valuation. OVER VALUATION?? Who determines fair value is not always driven by historical fair values, so don’t get caught overly cautious simply because valuations get stretched beyond historic norms. That’s also how markets work. As the market trends higher it begets more highs…eventually!

Many investors become confused by market actions, especially when the cycle is elongated as the current bull market cycle has become. Richard Bernstein, who has spent decades on Wall Street, believes the late-cycle economic environment is creating too much confusion on Wall Street — pushing many investors to make ill-advised decisions.

“Late in the cycle makes it sound like the abyss is minutes away. That’s not really where we are,” Bernstein said Monday on CNBC’s “Trading Nation.” “The signs of what would really signal a true bear market are really nowhere to be seen.”

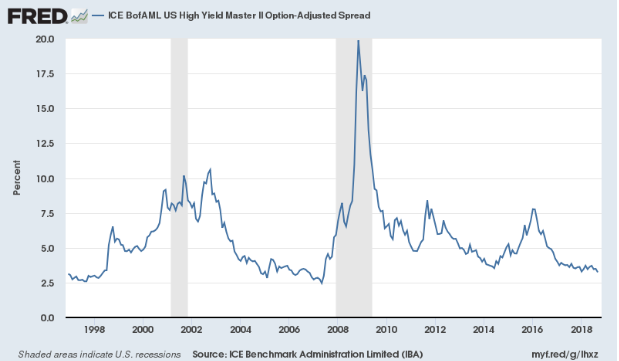

According to Bernstein, the U.S. economy is firing on all cylinders, and earnings should remain strong through next year. Bernstein has seen all types of markets in his many decades of following and participating in the equity and bond markets. He’s not just going off hunches and assumptions and letting duration of the economic cycle guide his sentiment. In fact, one of the leading indicators of a recession, credit spreads for high-yield bonds suggest the economy is on strong footing.

Bond buyers say the historically narrow gap between yields on below-investment-grade corporate debt and “risk-free” U.S. Treasurys, in other words, investors are demanding less of a premium to hold riskier debt. This essentially reflects the belief that the expansion has room to run.

A rapidly widening spread is viewed as a potential indicator of recession danger, while a narrowing spread indicates investors are upbeat about the outlook. Before each of the past 3 recessions, the high-yield credit spread started to widen, according to ClearBridge Investments.

“The naysayers of this economic expansion don’t seem to be reflected in the credit markets,” said Jim Sarni, managing principal at Payden & Rygel Investment Management.

The bullish growth outlook implied by muted credit spreads runs counter to the view held by perma bears that the economy’s second longest expansion since World War II will see its demise sped up by the Federal Reserve’s tightening cycle.

Third quarter earnings reporting season is just around the corner and investors are expecting another 20%-plus S&P 500 earnings growth quarter, on a YOY basis. Expectations are running high for investors, which would give cause for the market to pause if not also for fears of a near term yield curve inversion. Nonetheless, FactSet is anticipating Q3 2018 earnings to grow 19.9% YOY and Thomson Reuters is forecasting Q3 2018 earnings to grow 21.7% on a YOY basis. Year-to-date, earnings have beaten forecasts by 4.5 percent. If Q3 falls inline with the two previously reporting periods, the quarter could show another quarter of 25% YOY growth.