U.S. equities are pointing to a lower open after the government reopened yesterday. All three major stock market indexes closed at record levels on Monday. After U.S. markets closed on Monday, Congress passed a three-week funding measure that brought a halt to the three-day shutdown, with the bill then signed by President Donald Trump. The agreement keeps the government running up to Feb. 8, 2018.

Shares of Netflix soared after hours yesterday and after the company handily beat the expectations for subscriber growth. Netflix beat revenue expectations by just under $10 million, logging earnings exactly where Wall Street predicted at 41 cents a share. But the company blew net subscription additions out of the water, logging 8.3 million new net subscribers, a 18% gain over the same period last year. Subscriber growth was well above the company’s forecast of 6.3 million. It also handily beat the analyst consensus forecast of 6.37 million. Netflix released expectations for top- and bottom-line growth well above what analysts polled by FactSet expect — issuing guidance for earnings of 63 cents a share on sales of $3.69 billion. Currently, analysts model earnings of 54 cents on sales of $3.49 billion. The company also expects to add 6.35 million net subscribers, or about 1 million more than Wall Street expects. Management expect to spend between $7.5 billion and $8 billion through 2018 on content costs.

More earnings will hit the tape today. Earnings are expected from four Dow components: Johnson & Johnson, Procter & Gamble Co., Travelers Cos. and Verizon Communications Inc. Reports are also expected from United Continental Holdings Inc., Kimberly-Clark Corp. and State Street Corporation.

U.S. equity markets remain complacent in the face of a rising 10-year yield, which tipped past 2.66% in yesterday’s trade, but has fallen back slightly and to 2.62% in early trading Tuesday. The U.S. green back is higher after falling over the last several trading sessions with volatility also lower over the last 2 trading sessions.

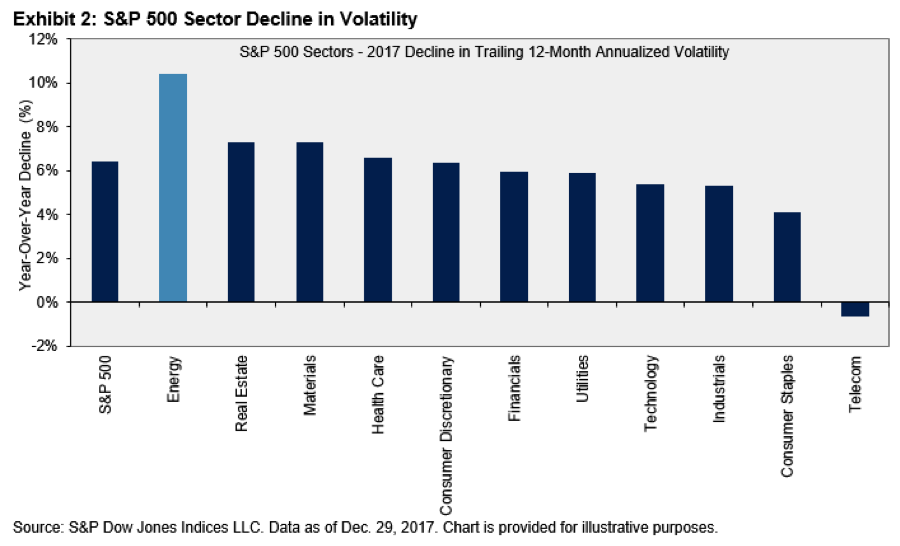

Dispersion and correlation among indexes created unusually low levels of volatility in the trailing twelve-month period. This also resulted in the VIX mean reading of 11.10 in 2017, nearly half of its historical mean reading. The chart below identifies decreases in volatility across the majority of sectors. The energy sector had the largest decrease in volatility in the trailing 12-month period.

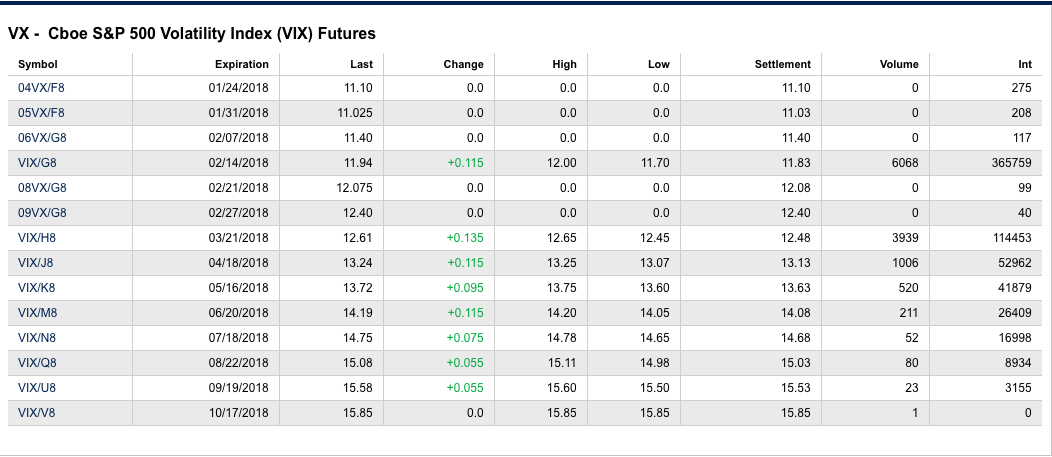

As for today, the VIX is relatively flat while VIX futures are notably higher ahead of the markets open. Contango is healthy at just over 5 percent.

In news from across the pond, Europe is painting a mixed picture with the CAC lower, FTSE and DAX higher. The DAX is likely getting a lift off some improved economic data. German economic sentiment rose in January and analysts remained optimistic about Germany’s near-term growth prospects despite the country’s struggle to form a governing coalition. The ZEW think tank said Tuesday that its measure of economic expectations rose by three points to 20.4 points, beating economists’ forecasts of 17.5 points.

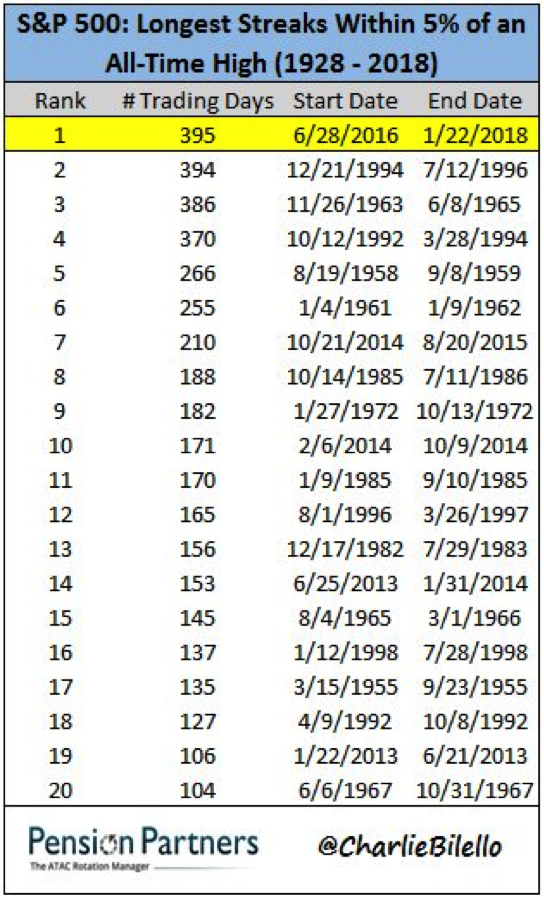

This has been a record setting bull market that has not gone unnoticed by investors.

As of today, the S&P 500 has set a record for longest streak without a 5% pullback as indicated in the table above by Pension Partners. It’s anybody’s guess as to when or to what extent the next pullback in the markets will be found. Warning signs are always abound in the market, indicating a potential market decline is on the horizon. One thing is for certain, a pullback will be found and investors with actively managed portfolios, and cash handy, will be advantaged and rewarded for their prudent planning.