The first week of September 2018 will likely leave much to be desired as it’s shaping up to be a rocky week for equities. The S&P 500 finished lower for a 3rd straight day on Thursday and is looking for a bit of a relief rally after rising to as much as 2,916 just a week ago. The S&P 500 has pulled back roughly 1.4% since, as investors await the next catalyst in the marketplace. Apparently, insiders aren’t waiting to buy equities, but rather selling them at an alarming rate.

According to data from TrimTabs Investment Research, insiders dumped some $10bn in stock ownership during the month of August. This was the most insider selling since last November.

“They’ve dedicated record amounts of shareholder money to buybacks but aren’t doing the same with their own which suggests that companies aren’t buying stocks because they’re cheap.”

On the surface, the data from TrimTabs looks alarming, seeing how we expect corporate insiders to be knowledgeable about the prospects for their companies and therefore a good gauge at valuing their own stock. This is not always the case and the truth is that these types of headlines have occurred throughout the current bull market cycle as indicated in the following graphic:

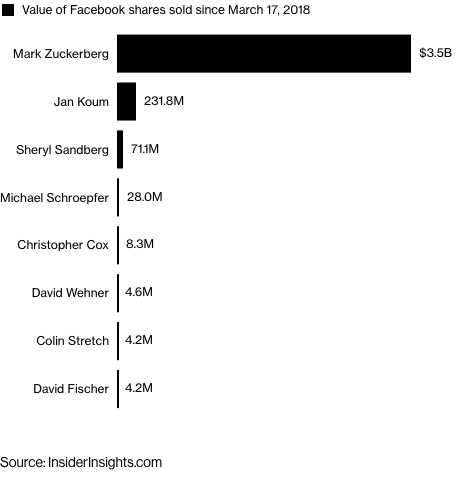

Some of the largest corporate insider selling has come from Facebook in 2018. Just since the Cambridge Analytica scandal, Facebook insiders have sold some $3.9bn in stock. Chief Executive Officer Mark Zuckerberg accounted for about 90 percent of the total, according to data from InsiderInsights.com, which analyzes such transactions. Most of Zuckerberg’s sales are part of a plan announced last September to sell as much as 18 percent of his Facebook stock. Zuckerberg and wife Priscilla Chan pledged in December 2015 to sell most of their shares over time to invest in philanthropic causes.

The tech sectors have been under heavy selling pressure in the early parts of September and finished lower by nearly 1% on Thursday.

“This is very much a tech-centric reversion. It is long overdue, given how much the Nasdaq has been outperforming the rest of the market,” said Peter Kenny, market strategist at Kenny & Co. “This is bigger than FAANG, but the scale of that move is the primary driver of what we’re seeing today and what we saw yesterday. I think there’s still some downside ahead, and that this won’t be a short-term correction, but something that will take a long time to work through.”

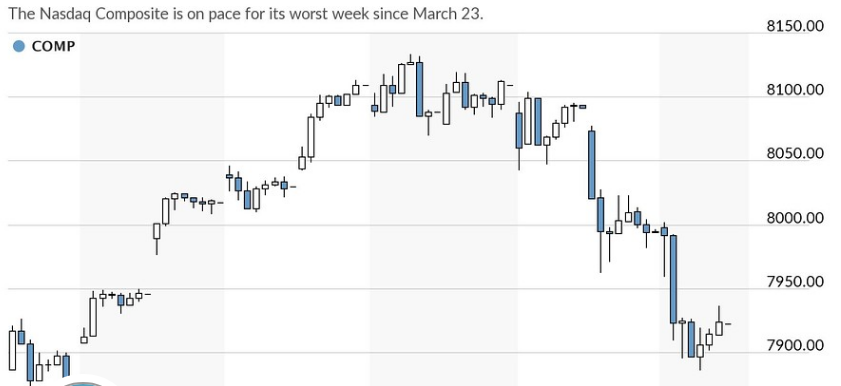

The tech-heavy Nasdaq is set to decline 2.5% for the Labor Day trading week, which would represent its steepest weekly drop since March 23 when the index plunged 6.5 percent. An index of the largest companies by market value, the Nasdaq-100 Index is set to suffer its worst weekly slide, down 2.9%, since late March.

One factor driving the weakness in the tech sector has been concerns surrounding social media platforms. Executives from Facebook and Twitter attempted to defend their efforts to prevent outside manipulation of their social-media platforms by Russian and other foreign actors in recent Capital Hill testimonies, which have fueled concerns over the ability for these social media sites to secure user interests and engagement. The concerns over social media security, regulation and general sales trends have found both stocks under heavy selling pressure in recent weeks. Coupling the social media giants’ broad operating issues with news out of KLA-Tencore yesterday and the tech sector has seemingly been caught in between a rock and a hard place. The chief financial officer of KLA-Tencor Corp. offered a weaker-than-expected outlook for chip shipments at the Citi Global Technology Conference, which helped to send the broader sector spinning lower.

While Peter Kenny is of the opinion the tech wreck will take more time to bottom and then recover, Art Hogan shared a different opinion on the subject yesterday.

“I don’t think the uptrend is broken whatsoever,” said Art Hogan, chief market strategist at B. Riley FBR Inc. “But I do think that it is a healthy reminder that momentum runs both ways. Additionally, the U.S.-China trade spat might be fueling some of the sell-off right now.”

The fundamentals of certain tech companies may remain in question until the next earnings cycle, but the technical view of the Nasdaq remains bullish. Neither the Nasdaq Composite nor the Nasdaq-100 have broken through their short-term moving averages, which market technicians tend to use as evidence of an assets bullish or bearish trend. The Nasdaq is holding about 1.5% above its 50-day moving average at 7,817.84, while the Nasdaq-100 is about 1.3% above its short-term trend line. (See chart below)

If indeed some of the latest selling pressure in the tech sector is due to the U.S.-China trade spat, it may be warranted. The Trump administration is considering tariffs on another $200 billion in Chinese goods, after a comment period expired at midnight on Thursday. China, of course, has its own list of tariffs on $60 billion in U.S. goods as a retaliatory measure.

Analysts have stated that it’s unclear how much of the tech sector selling is related to trade worries, but it may have some connection. Micron, Qualcomm and Intel are among companies with the most revenue exposure to China, according to Strategas. According to the Peterson Institute for International Economics, the initial list of possible targets from the U.S. trade representative on the $200 billion in goods, includes tariffs on more than $15 billion in computer parts and $8 billion in computers, in addition to the top product, $24 billion in telecommunications equipment. The tariffs would be in addition to tariffs on a previous $50 billion in Chinese imports and on steel and aluminum.

“Forty-seven percent of the U.S. import tariffs are on intermediate goods, and most likely the tariffs will raise their costs and make U.S. technology companies less competitive,” said Lucy Lu, research analyst at Peterson. “The U.S. companies will either absorb these increasing costs or pass the costs to consumers.”

Be it the U.S.-China trade spat, weakened chip demand or social media platform security and regulation concerns, the overall weakness of late is concerning to many investors. However, in a recent OpEd from Mark Hulbert the famed market watcher offered the following sentiment:

“Whatever else we can say about recent tech sector weakness — and there is no shortage of commentary on the subject — I doubt it’s signaling an imminent bear market.”

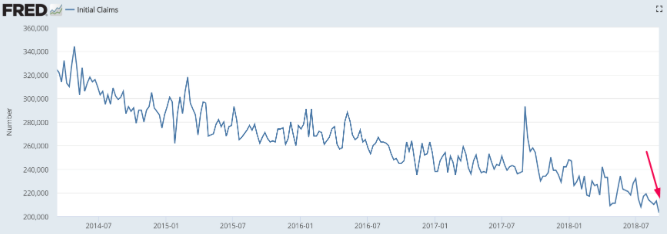

As Thursday’s trade gives weigh to Friday’s trade, investors will be eyeing a key piece of economic data. In the latest readings on the labor market issued Thursday, the U.S. created 163,000 private-sector jobs in August, according to payrolls processor ADP. This was below the 182,000 that had been expected, as well as down from July’s 217,000 reading. Separately, jobless claims fell to their lowest level since 1969. Yesterday’s reading for Initial Claims made a new low for this economic expansion, falling from 213k to 203k. Initial Claims are still trending lower presently and indicating a very strong labor market.

When the Nonfarm Payroll report is released, economists expect for the economy to express that 191,000 nonfarm payrolls were added in August, following 157,000 in July, according to Thomson Reuters. The unemployment rate should dip to 3.8% form 3.9%, and wages are expected to rise 0.2 percent.

Mark Zandi, chief economist at Moody’s Analytics, says he sees just 170,000 jobs and he also blames August.

“It should be a little on the soft side, but for technical reasons. The August first print comes in soft. It’s generally, I think related to the fact that there are fewer respondents in August,” he said. Zandi said the August payrolls are often revised higher, by 25,000 or 30,000 jobs as more data is collected.

Even as the economic data remains relevant, speculation as to when and not if President Trump and the OSTR announce further trade tariffs on Chinese imports may be of greater importance in September. UBS’ recent thoughts of the impact to the market in the event of implementing the $200bn in tariffs on Chinese goods suggests U.S. equities would take a hit. Their base case scenario would be a 10% tariff on $200bn worth of Chinese goods, but should the Trump administration opt for a 25% tariff…

“In our view, recent talks with the EU and Mexico help mitigate the downside scenario of the US fighting a trade war on two fronts, at least near-term, [but] the prospect of 25% tariffs on the $200bn of China imports is not fully priced”, UBS warns, before going on to predict that earnings would likely suffer a ~3% hit under the base case scenario with U.S. stocks falling some 2%.

“A 25% tariff rate could be construed as an escalation and would have a greater earnings impact and markets would need to price the potential for continuing escalation, thus, 25% tariffs could lead to a 5%+ type pullback.”

UBS doesn’t view the escalation of trade tariff implementation as the end all and be all of the bull market, but it is warning investors that the market could take a short-term hit. Investors have been preparing for such an event based on outsized protection buying activity and with volatility already rising ahead of the probable tariff implementation by month’s end.