There’s some good and bad residing within every trading day. Yesterday’s good news was the performance or rotation out of large and midcap stocks and back into small cap stocks as the Russell 2000 Index outperformed its larger peer indices. Rotation is a sign of a healthy market as it points to active market participation and the propensity for future favorable advance/decline line readings in the broader indices. Additionally, through this rotation we also witnessed a healthy increase in volatility that identifies the activity and relatively healthier level of fear in the market. Having said that, the relative bad in the market yesterday was the declines in the S&P 500, Dow and Nasdaq, all falling on the day, led by the Dow with a greater than .5% decline. Finom Group has pared the declines in the major averages with the continued declines in the Yuan, for now.

In a recent CNBC interview, President Donald Trump discussed the yuan’s nosedive in recent months that has seemingly gone unabated by the PBOC. Trump directly cited the yuan in his CNBC interview on Thursday, which has been aired on Friday morning.

“China’s currency is dropping like a rock,” he told Kernen, adding that “Our currency is going up, and I have to tell you it puts us at a disadvantage.”

The PBOC has no interests in stemming the decline in its currency as the U.S. threatens its exports with tariffs. In fact, the weaker yuan serves to soften the blow on China from the trade conflict. Overnight on Friday, the PBoC weakened the fixing of the yuan by the most since June 2016, in a clear sign that the PBoC is more than fine with letting the market push the currency lower. As the PBOC sits back and watches its currency devaluation in continuum, because its currency is managed, doing “nothing” is akin to doing “something”.

The future of the yuan, despite the recent declines, is not in question due to capital flight fears. More than likely and akin to the decline in the yuan experienced in 2015,t he PBOC will step in shortly to stem the decline. The known “unknown” is likely why Chinese equity markets were sharply higher overnight.

While the aforementioned are mostly negatives in terms of sentiment for market investors in the U.S., some of the positives were also very apparent/clear in yesterday’s market performance. Initial jobless claims continued to shine and express a strong labor market that supports continued economic expansion. Yesterday’s reading for initial claims made a new low for this economic expansion (207k). The key takeaway from the data is that Initial Claims are still trending lower, a net positive for the equity markets.

The following chart identifies the correlation of the S&P 500 with initial jobless claims.

Although the market dropped yesterday, the economic data that continues to come in with strong readings, suggesting that yesterday’s market rotation was healthy on the whole and when expressed in sector rotation. The following chart identifies the S&P possibly retesting its recent breakout from 2,800. From the chart below, ideally the bulls would appreciate the S&P 500 holding and closing above the 2,800 level to finish the week again. A 2nd consecutive weekly close above 2,800 is only one of the bullish statistics working against the bears right now.

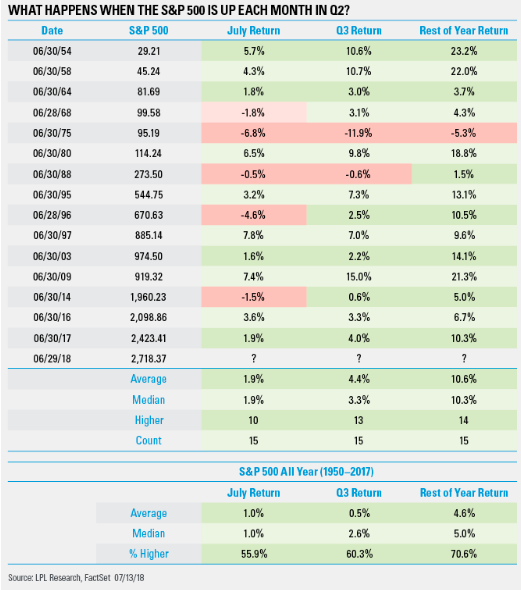

LPL Financial recently studied the history of Q2 annual market performances. What they found was relatively promising for bulls and likely another thorn in the side for bears. The following notes come directly from the firm’s recent publication.

“The S&P 500 Index is on a three-month winning streak, and more gains may be in store for bulls. As shown in our LPL Chart of the Day, in the last 15 instances when the S&P 500 has closed higher in April, May, and June (like 2018 just did), all but one of those years saw unusually strong returns in the second half. In fact, in those 15 years, the S&P 500 returned 10.6% on average from July to December. The chart also illustrates that weakness in July following a strong second quarter doesn’t necessarily portend the remainder of the year; and, with the index up roughly 3% on the month so far, note that third quarter and full-year returns were positive in every instance where July finished in the green.”

From the broader market moves we turn our focus to what ultimately will be the driving force behind equity market moves, corporate earnings. This is not to say that other variables won’t shake equity markets from time to time. Geopolitics and other macro factors should be understood by active traders and investors. The summer months are often low-volume market months and may not signal true market direction despite what charts are signaling. Additionally, when we look to history to guide market forecasts, the reality there is no historic precedence for today’s market and economy that is underscored by extended QE periods that have finally led to QT and coupled with fiscal tax stimulus. And when you throw into the mix a midterm election cycle…well again there is simply no precedence to review.

Moreover and speaking of corporate earnings, Microsoft (MSFT) reported a beat on both the top and bottom line after the closing bell yesterday. Here’s how the company did:

- Earnings: $1.13 per share, excluding certain items, vs. 1.08 cents per share as expected by analysts, according to Thomson Reuters.

- Revenue: $30.09 billion, vs. $29.21 billion as expected by analysts, according to Thomson Reuters.

- Microsoft chief financial officer Amy Hood told analysts on Thursday’s earnings call that the company expects $27.35-28.05 billion in revenue. According to Thomson Reuters, analysts had expected Microsoft to forecast $27.38 billion in revenue, below the midpoint of the guidance.

On the heels of Microsoft’s better than expected results and guidance, the tech-heavy Nasdaq is looking to open higher on Friday while it’s peer indices are still signaling a negative open on Wall Street. The highlight of Friday and possible market guidance will be taken from a pre-taped interview on CNBC between President Donald Trump and Joe Kernan. The post airing of the interview suggests investors are more concerned about the potential for President Trump to go through with all the pre-announced tariffs on China. It has been previously reported that President Trump is unhappy with the status of trade talks between the U.S. and China. Investors can review the full interview here.

While the equity futures are steadily worsening ahead of the open on Wall Street, Finom Group will look for a trading opportunity offered by the sentiment swings. Our most recent trade came from shares of Apple Inc. AAPL and displayed below.

Regardless of the market landscape, Finom Group continues to seek out and deliver trading opportunities for subscription members. At present, we expect the bulls to defend the SPX 2,800 level on Friday. How successful they will be in doing so remains to be seen.