Welcome to this week’s State of the Markets with Wayne Nelson and Seth Golden. Please click the following link to review the SOTM video. The potential beginnings of a market pullback are afoot with the S&P 500 falling roughly 1% this week. We all know that when valuations stretch too far beyond their historic average, unkind things tend to take place in the market. Nonetheless, we view any pullback during an economic expansion with relatively low rates, a strong labor market, free-flowing credit and an accommodative monetary policy as an opportunity to buy good company names and to increase exposure to the equity market strategically. We encourage viewership of the weekly SOTM to include reading the notes that accompany the weekly video, below. We suggest the bull market will carry forward, but not higher in a straight line and not without a near-term correction.

- For the “right here and now” aspect of market commentary from Tony Dwyer, he is of the opinion that investors should take offensive positioning off the field. His main reason…

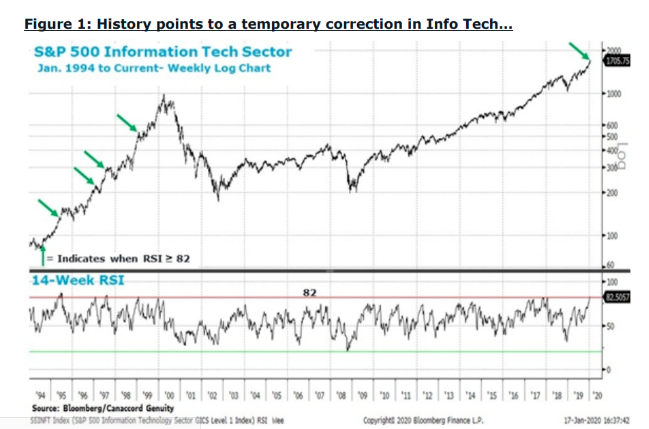

- The market, and the information technology sector in particular, “have reached a point that warrants a change in view.” The S&P 500 Information Technology sector has reached what he calls a “historically extreme level” for only the fifth time since 1990. (Chart above)

- JC O’Hara of MKM Partners, said in a note to clients to “swim at your own risk” at these elevated prices. A pullback could be around the corner.

“I think it is safe to say this market has risen further, faster than most think.

The S&P 500 hasn’t had a daily move of more than 1% in either direction since October, O’Hara said, creating an abnormally calm market.“

- From Tony Dwyer’s perspective, one of his key indicators for intense market rallies that is signaling a potential warning for investors comes out of the tech sector.

“History has shown that either a long-duration consolidation period or a nasty pullback can help relieve market excesses, and we have evidence the move higher in Tech has created the type of environment that generated temporary corrections in the pre-dotcom era.”

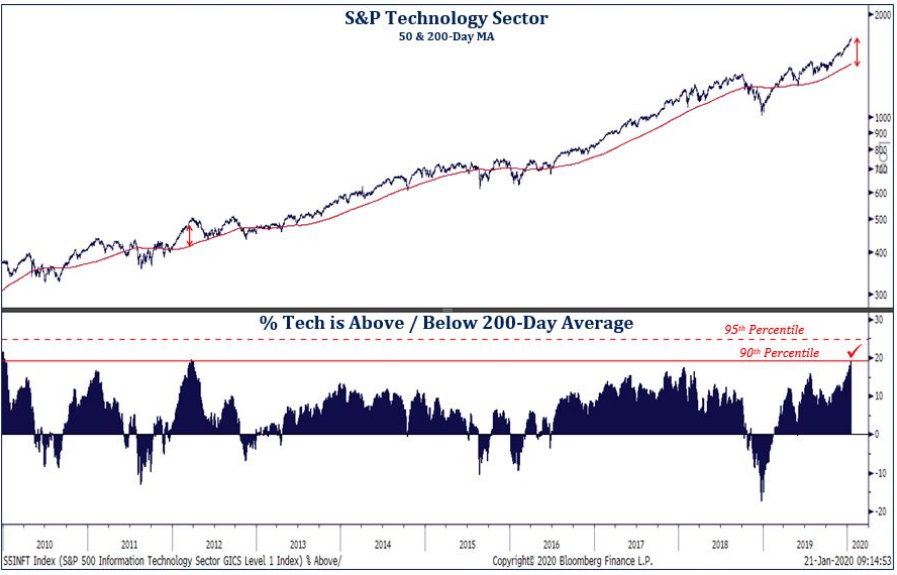

- Strategas: “Great trend, but tactically Tech is stretched here. At nearly 20% above its 200-day average,that’s enough to qualify as a statistical extreme in our work.“

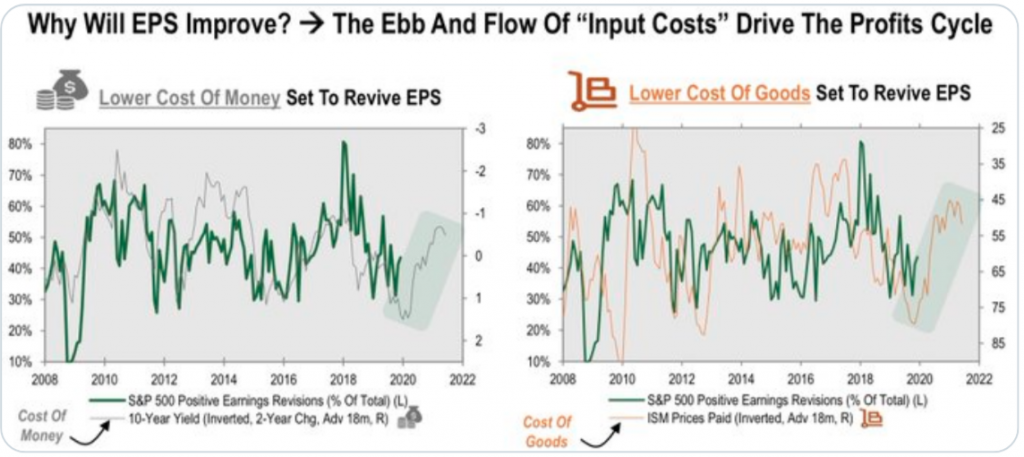

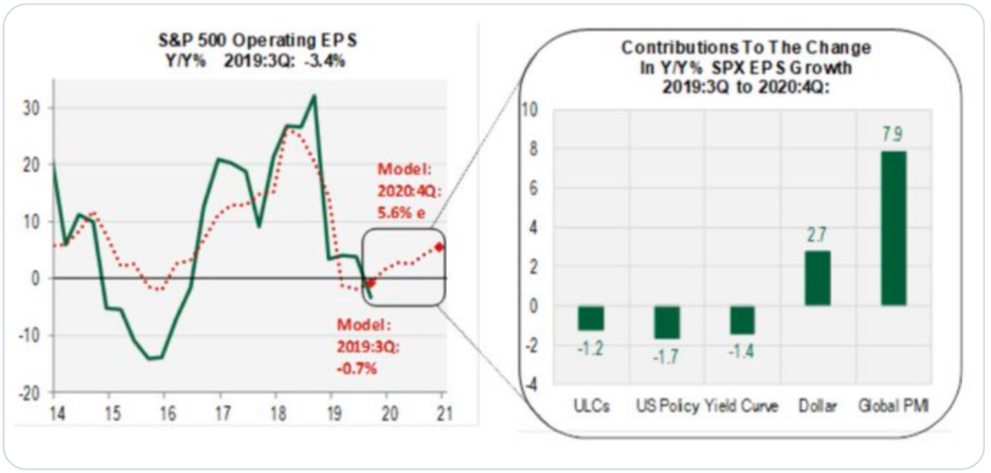

- Starting in Q1, we expect positive earnings revisions as lower input costs work their way through the global economy.

- This should keep credit spreads tight and P/Es expensive. Gains likely to be limited by a mild earnings recovery and already-easy financial conditions.

- We think the dollar and the global PMI will drive the upswing, and stocks with highest exposure will benefit the most

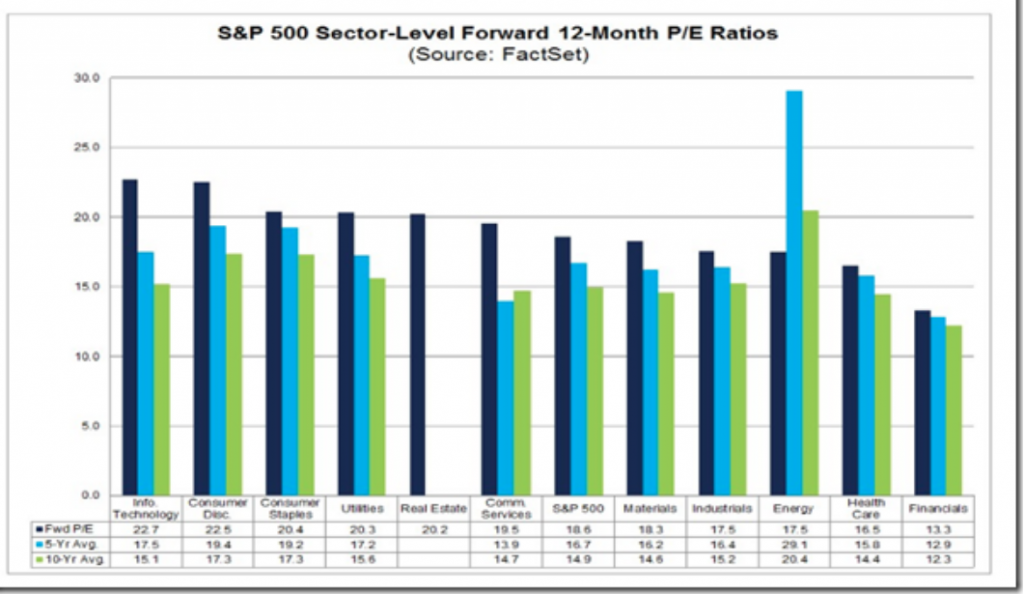

- Energy, Industrials, Materials, Financials, and Health Care are showing 12-month forward price/earnings ratios of between 13.3 and 18.3, below the S&P 500 multiple of 18.6, which is the highest level of this economic expansion.

- For reference, the forward P/E of the technology sector currently sis at 22.7.

- Valuations, on their own, do not overcome the laws of supply and demand for sector constituents, but, as price moves higher, demand would be expected to wane relative to supply and prices would then be forced to a new equilibrium in order to balance the two forces, once again.

- CREDIT SUISSE: “We are raising our 2020 S&P 500 target to 3600 from 3425,” .. These estimates imply EPS growth of 6.2% in 2020, a substantial improvement from 2019’s 1.1%. We project forward multiples to expand to 19.6x by year-end 2020 from 18.9x currently.”

- Citi’s “normalized earnings yield gap analysis” showed a near 90% chance of market gains in the next 12 months, according to the bank’s chief U.S. equity strategist, Tobias Levkovich. He contended the widely watched S&P 500 price-to-forward-earnings ratio could be skewed by low rates due to global central banks’ quantitative easing measures.

- “We do not see the makings of a bear market based on our indicators,” Levkovich said in a note Wednesday. “We do not see the pent-up demand that would generate a new S&P 500 or Nasdaq bubble either. Given global QE, there is a legitimate argument to be made that a distortion in yields may be sending the wrong signal for valuing stocks.

- Low bond yields are cited as providing a reduced discount rate such that much higher multiples can be appropriate.”

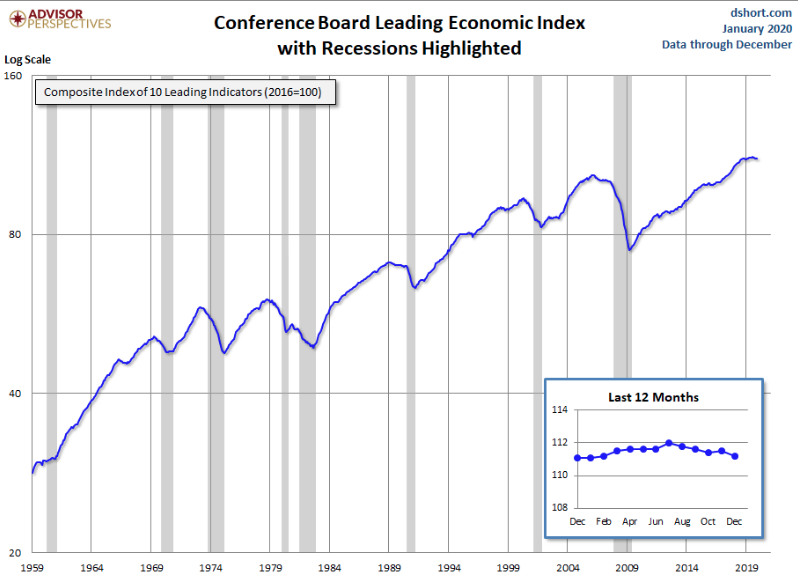

- The leading economic index fell 0.3% in December to mark the fourth decline in the past five months, the Conference Board said.

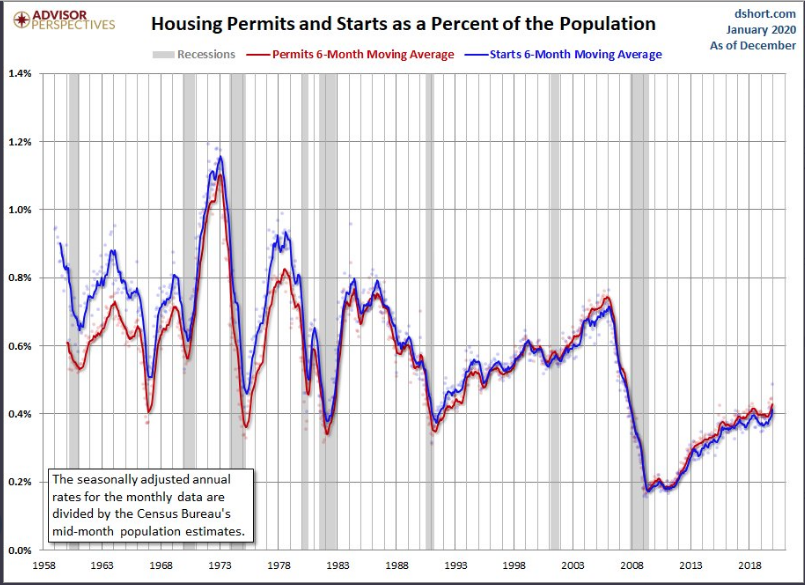

- The drop in the index largely stemmed from an increase in jobless claims and a decline in building permits for new houses, but claims have fallen since then and the weakness in permits is seen as temporary.

- Building permits were also weak in December, but construction on new homes actually hit a 13-year high. Permits are trending well above year-ago levels, and with mortgage rates falling again, are likely to rebound in January.

- Typically you don’t have a recession in the same calendar year that housing starts hit a cycle high.

- Also, yields are low, and the demographic patch is stable. Most importantly, a very soft expansion in production.

- The LEI’s “six-month growth rate turned slightly more negative in the final quarter of 2019, with the manufacturing indicators pointing to continued weakness in the sector,” said Ataman Ozyildirim, economist at the board. “ However, financial conditions and consumers’ outlook for the economy remain positive, which should support growth of about 2 percent through early 2020.”

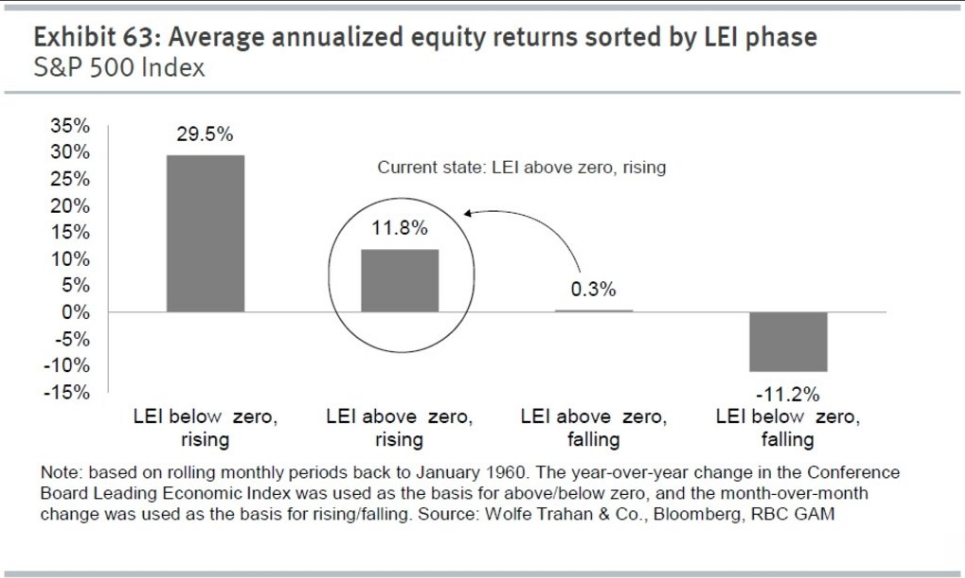

- Averge annualized returns for SPY when the LEI is below zero and falling are -11.2%.

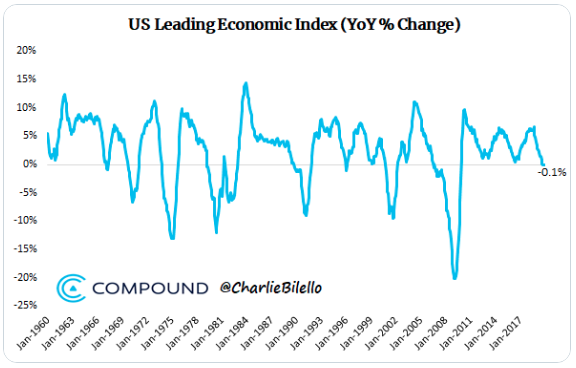

- US Leading Economic Index: -0.1% over past yr, first negative since 2009.

- Last 5 times LEI went from + to – YoY: Aug 2006 (recession Dec ’07) -Nov 2000 (recession Mar ’01) -Jan 1996 (only 1 month neg, no recession) -Oct 1989 (recession Jul ’90) -Jul 1981 (recession Jul ’81)

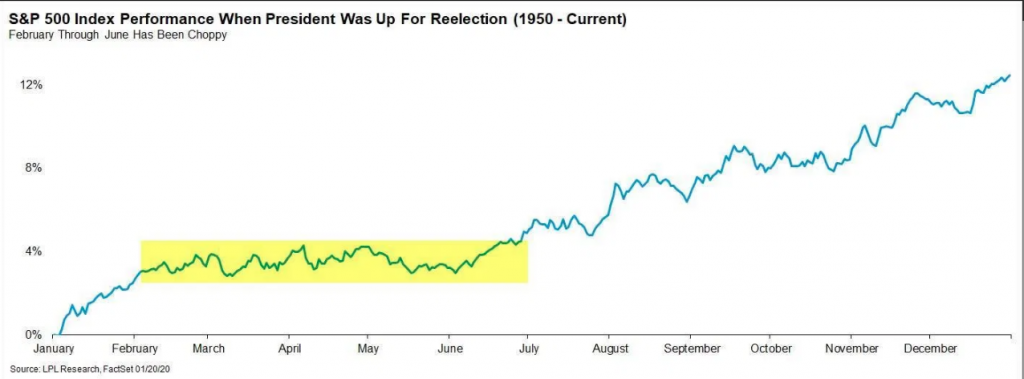

- The S&P 500’s track record for reelection years has been impressive, but its average path during these years has been quite interesting.

- In 10 reelection years since 1950, the S&P 500 on average has barely budged from February through June, before breaking out in the second half of the year.

- “Stocks actually have traded in a tight range from February through June during election years, with the big rally taking place during the second half of the year,” explained LPL Financial Senior Market Strategist Ryan Detrick.

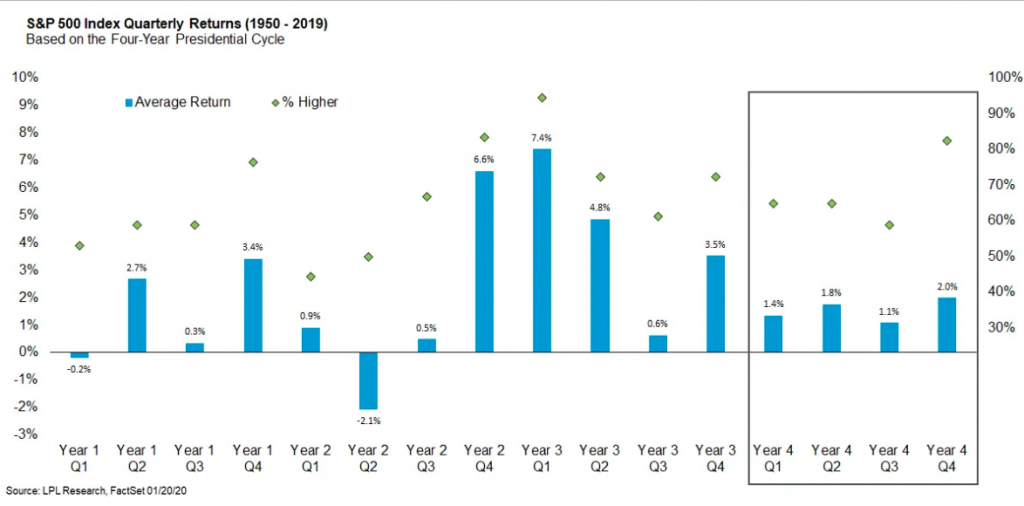

- From a quarterly view, the S&P 500 has historically posted modest returns in the four quarters of an election year, but the benchmark has been higher an impressive 82% of the time in the fourth quarter of all election years.

- That’s one of the best track records of any quarter in the four-year presidential cycle.

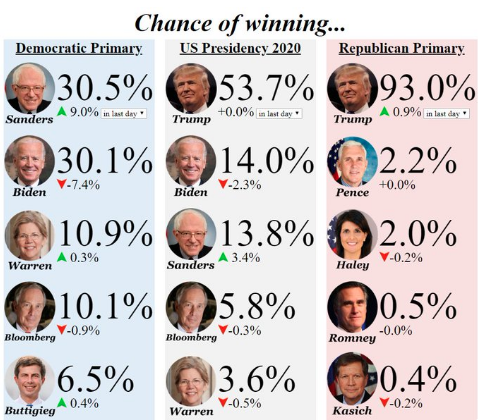

- As you can see from the graphic above, Sanders has recently surged ahead in the odds market as he has a 30.5% chance of winning the primary and Biden has a 30.1% chance.

- To be clear, just because the betting market shows this doesn’t mean the bond and stock markets expect him to win.

- The Iowa caucus is on February 3rd. The latest 2 polls have Biden ahead by 6 points. He averages a 3.7 point lead in the recent polls. Sanders has a 1.3 point lead over Biden in New Hampshire which has its primary on February 11th.

- In the latest 3 national polls, Biden is up by 5 and 7 points over Sanders and Sanders is up on Biden by 3 points. The CNN poll with Sanders ahead swung the odds on Wednesday. The average of recent polls has Biden only up by 6.1%.

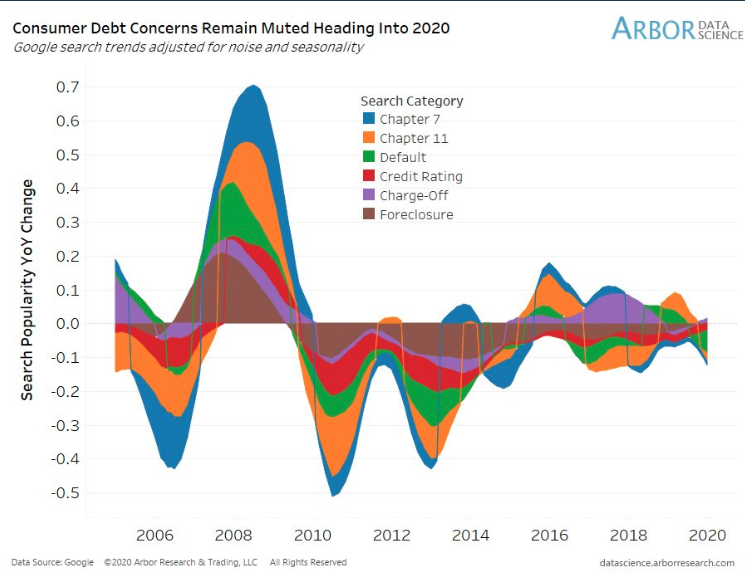

- U.S. consumer debt concerns not brewing according to Google search activity; burst of searches for bankruptcy, charge-offs or foreclosures preceding financial crisis not present in early 2020.

- With the employment rate at record level lows and job growth still forecasted in 2020, we continue to anticipate a healthy period of consumption in 2020.

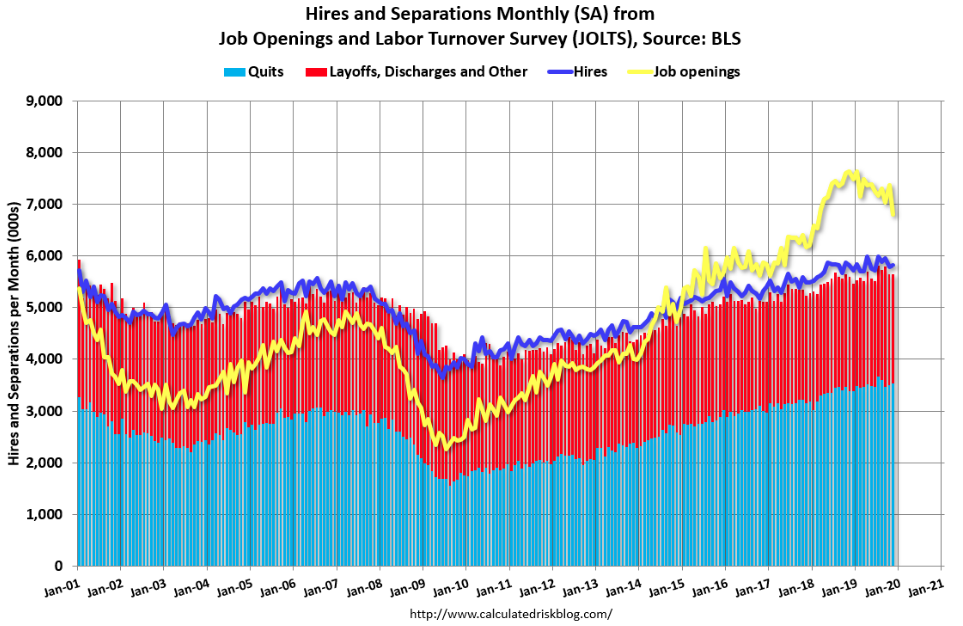

- U.S. job openings fell the most in over 4 years by 561,000 to 6.8 million in November, marking the lowest level since February 2018. That’s according to the latest Job Openings and Labor Turnover Survey (JOLTS).

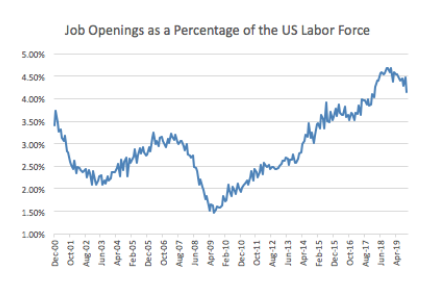

Job Openings as a percentage of the labor force fell to 4.14% in November 2019 compared to the record high of 4.68% in November 2018. The rate of job openings as a percentage of the labor force still exceeds levels reached in the last two economic cycles, but has been rolling over since 2018.

- In the last cycle, the number of job openings as a percentage of the labor force oscillated around the 3.0% threshold until the US stock market’s peak in October 2007 before falling to a low of 1.47% in July 2009.

- In the current cycle, this percentage continues to run closer to the 4% threshold, a red flag if breached. November’s large fall in job openings got it much closer, which gives us some concern given that it is an early indicator of trouble in the labor market since employers typically withdraw job listings before they start laying off workers.

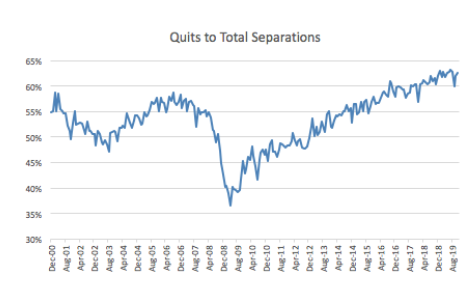

- Quits to total separations, rose to 62.6% in November compared to the record high of 63.1% in July 2019.

- This was due to an increase in quits and a fall in layoffs and discharges, an ideal combination.

- U.S. workers remain confident and employers are hiring, but the unusually large decline in job openings shows the US labor market may be slowing.

- Even with such a big move in job openings to the downside, they have outnumbered unemployed workers for 21 straight months.

- Prior to the beginning of 2018, unemployed workers always exceeded job openings since the start of the series in December 2000.

- As of November, job openings still outnumbered unemployed workers by nearly 1 million.

- This disparity highlights employers’ ongoing difficulty of finding qualified workers. Perhaps they have started to give up.

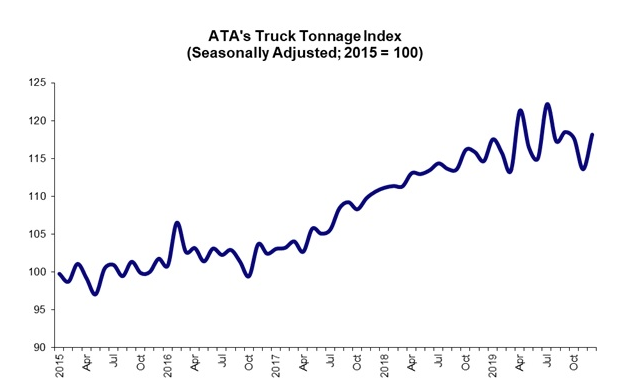

- ATA Truck Tonnage Index Increased 3.3% in 2019

- Monthly Index Rose 4% from November

- Trucking serves as a barometer of the U.S. economy, representing 70.2% of tonnage carried by all modes of domestic freight transportation, including manufactured and retail goods.

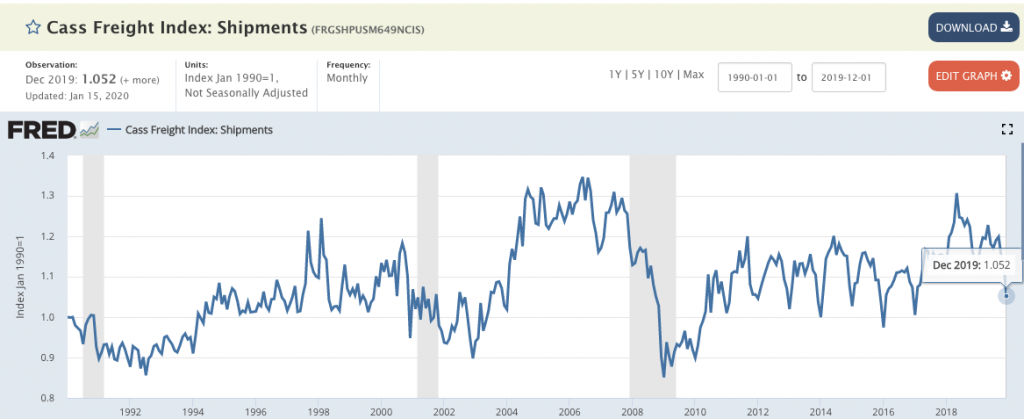

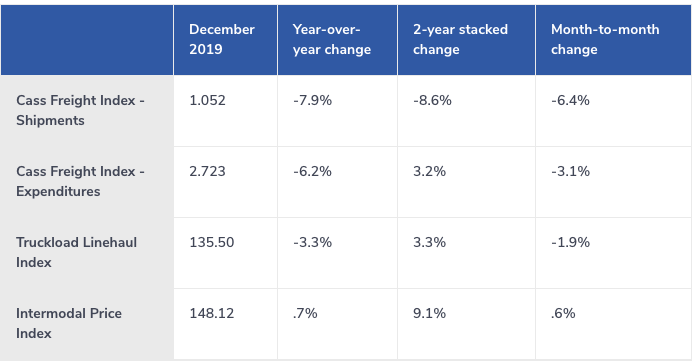

- Shipment volumes dropped 7.9% vs December 2018 levels, as the index posted its lowest reading since January 2018.

- It was also the steepest y/y decline since the Great Recession of 2008-2009.

- Although there were the same number of working days in December 2019 and December 2018, some industry participants we’ve spoken with about the sluggish end to the year cited Christmas and New Year’s Day both falling on a Wednesday as the reason for soft volume and low productivity the last week or so.

- “There is lots of hope in the stock market and the freight market for a better 2020, but the trends have yet to turn. Maybe with the January index readings? Doubtful, as the index (both shipments and expenditures) normally falls off sequentially from December to January, which would imply another negative y/y comp ahead. Our view is that the second quarter of 2020 has the best chance of seeing actual y/y growth in shipments and freight costs, if traditional seasonal freight patterns hold, as the second quarter of 2019 did not see the typical seasonal surge in activity.”

- “While we expect comps to ease and volumes to flatten out, we are not forecasting much growth in terms of freight volumes in 2020. The U.S. industrial economy – rebound or no rebound – will likely be the biggest swing factor. And the tariff relief from the Phase 1 deal seems to be just that – a relief for some, but not a stimulus.”

Below are three reasons we don’t see the deal contributing to much additional upside for U.S. stocks: Lisa Shalett, CIO Wealth Management Morgan Stanley

- China’s targets for U.S. imports seem ambitious. One reason investors have been excited about Phase 1 of the deal is that it calls for China to increase its imports of U.S. goods by $200 billion. However, when our analysts drill down into industry targets, we find that many of them seem unrealistic and enforcement mechanisms are limited.

- Existing China tariffs remain in place and U.S. policy makers could potentially seek more in Europe. The costs of tariffs are typically passed onto U.S. consumers, creating headwinds to economic growth. Remaining Chinese tariffs slow U.S. GDP growth by about half a percentage point, the Federal Reserve estimates. Our strategists believe an additional headwind from trade is possible this year coming from escalating trade tensions with Europe, now that U.S. policymakers seem to see tariffs as an effective tool.

- This phase of the China trade deal doesn’t resolve uncertainty around issues that may be inhibiting capital spending. The key issues with China that seem to most concern CEOs involve intellectual property and technology, and those discussions have been pushed off to the next phase of trade talks. That’s a big reason we remain skeptical that this will stimulate much additional capital investment.

- “The main impact of the trade deal, in my view, has been to put further escalation of trade tensions with China on hold for the next six-to-nine months. That, plus the stimulus added by global central banks, should support a global economic recovery, which is already underway.”

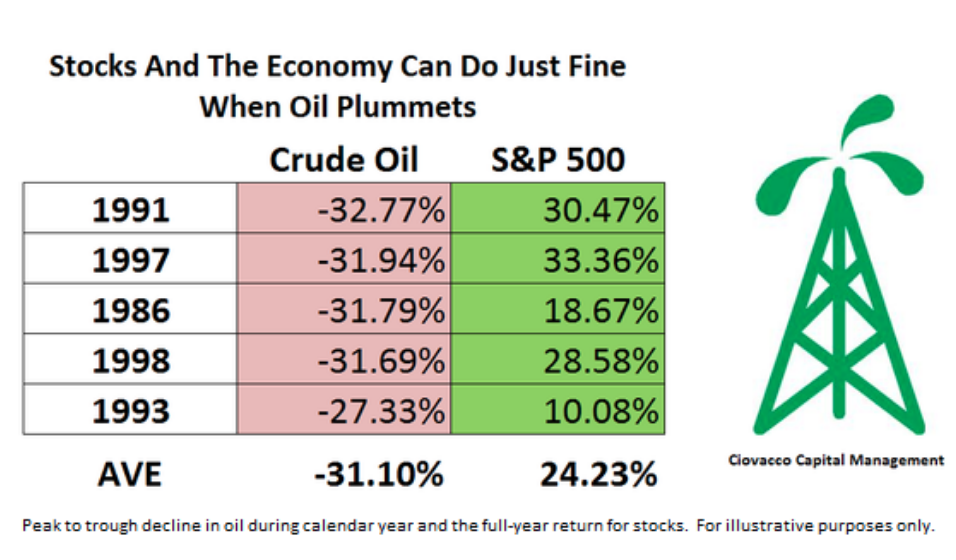

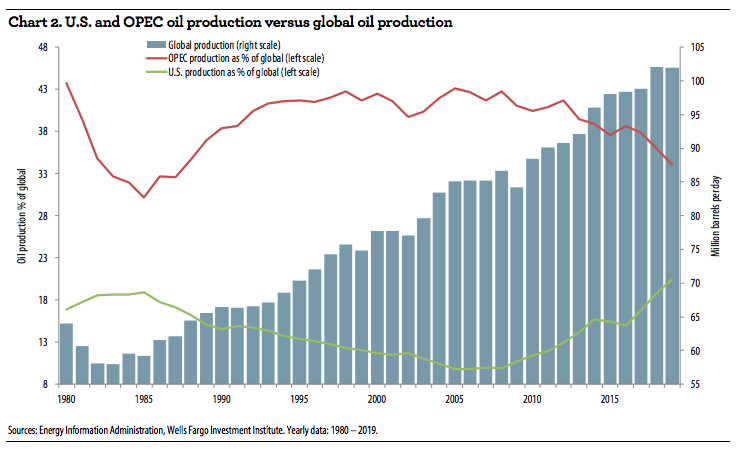

- Does weakness in oil mean the economy and markets are in trouble

- Some of the largest peak to trough declines in oil took place in 1986, 1991, 1993, 1997, and 1998 (average oil decline was over 30%).

- The average full year return for the stock market in those years was 24.23%