It was a huge day of VIX trading on Monday with VIX options and futures volume soaring. The bottom line is that hedging programs were deployed on scale given the relative low level/inexpensive hedges that could be afforded and with the S&P 500 achieving the 2,800 level intraday. Most of the hedging activity and upside protection spreads were bought within the April time frame as offered by the CBOE.

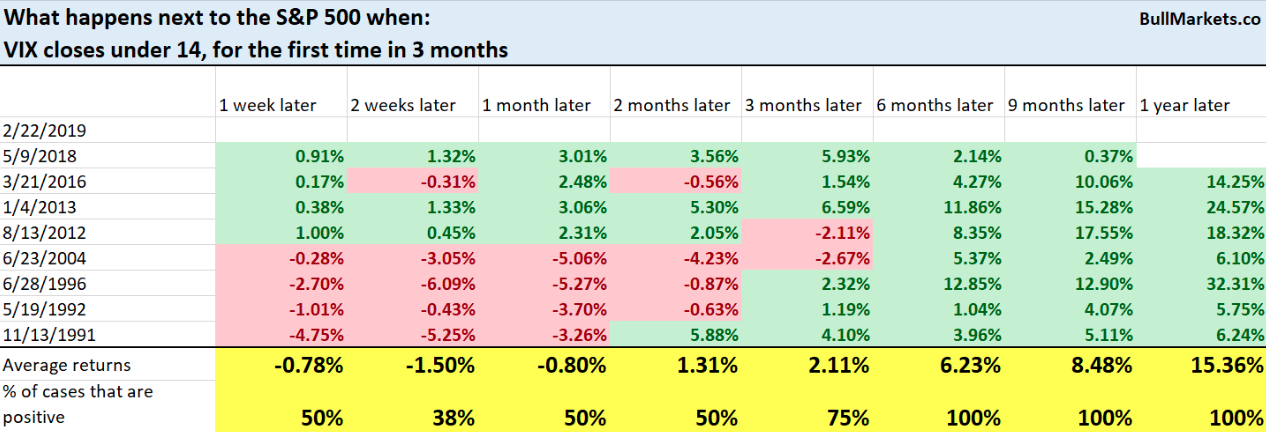

The VIX finished the previous week below 14 and had been lower for 9 consecutive weeks, a feat never accomplished in the index’s history. It was the first time the VIX had closed under 14 since October of 2018. Since the losing streak is a first of its kind for the index, historical statistical probabilities aren’t available without modifying the criterion and in effort to forecast the probabilities for the VIX going forward. With that in mind, here’s what happens next to the S&P 500 when the VIX closes under 14 for the first time in 3 months. (Tables from Troy Bombardia)

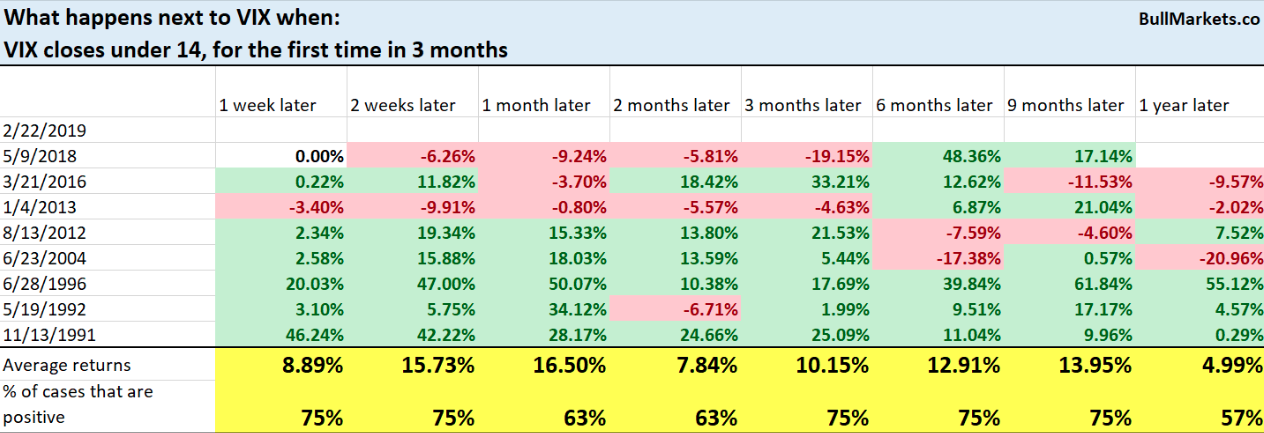

Additionally, here is how the VIX tends to perform using the same criterion mentioned above.

As one can see from the table above, the VIX doesn’t have a tendency to remain below 14 for any significant duration of time. Reverting to the prior table, however, the VIX also doesn’t express such complacent levels in a bear market. Something “for the bulls” you might say.

With the S&P 500 finishing the day below 2,800 and finding selling pressure going into the closing bell, there’s a high probability to see some additional selling pressure going into the Tuesday trading session. Just as buying begets buying, selling begets more selling.

The market is likely going to take a breather in the coming days and weeks as it digests a rather unprecedented 9-week rally whereby the S&P 500 rallied some 18 percent off of the December 24, 2018 lows. The timing for a potential pullback aligns almost perfectly with the timing of what was a 2-week, oversold period that occurred in December 2018. The S&P 500 has spent roughly 2 weeks now in overbought territory. All major indexes and index ETFs are in overbought territory as described in the table from Bespoke Investment Group.

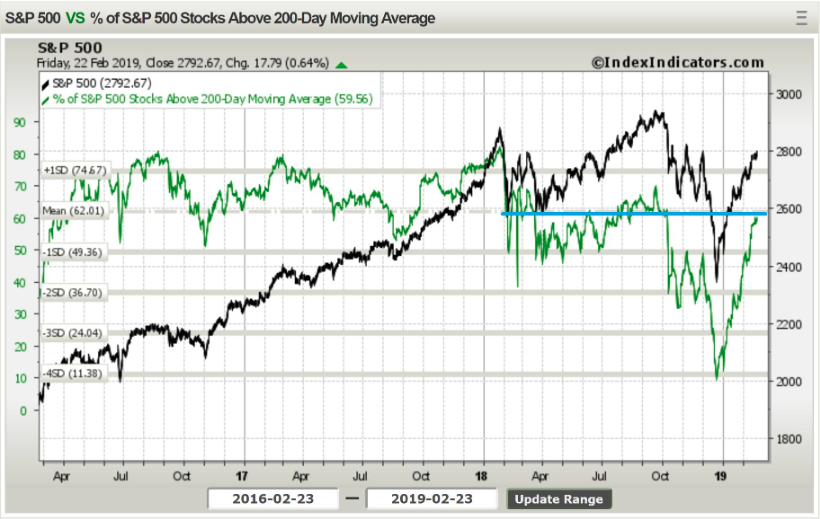

To further this point, the following chart identifies a key resistance level for the S&P 500 and market breadth as defined by the percent of S&P 500 stocks trading above their respective 200-DMA.

So what do markets have to contend with during what proposes to be a consolidation period? On Tuesday, a host of media headlines will pervade the airwaves and social media sites as President Donald Trump and N. Korean Chairman begin their 2nd Summit. Washington has demanded that Pyongyang abandon all its nuclear and missile programs, while North Korea wants crippling sanctions to be removed as part of denuclearization negotiations.

“So far, North Korea seems only willing to take measures that limit its nuclear and missile capabilities, it has no indications that it wants to roll back or undercut its existing nuclear arsenal or missile arsenal,” Tong Zhao, a fellow at the Carnegie-Tsinghua Center for Global Policy, told CNBC on Tuesday.”

However, the meeting will be timely for the two sides to negotiate some meaningful progress so that Pyongyang is held back from taking “risky and destabilizing nuclear postures,” said Zhao.

While President Trump is abroad, on the domestic front his former attorney will be testifying before congress and the Fed heads to Capital Hill. We would expect significant headlines to proliferate from the hearings that are slated to carry on throughout the week. While the headlines may be politically damaging for the White House, they will have little to no impact on the economy and as such would only serve to stoke volatility in the markets and little else.

Fed Chairman’s testimony before a congressional panel will likely be met with a warm welcome as the Fed’s shift from hiking rates to pausing rate hikes finds more favorable economic and market conditions.

“Sal Guatierei, senior economist at BMO Capital Markets, agreed: “Pastor Powell will deliver a sermon from the Book of Patience before Congress, the one message both parties actually agree on.”

“Joseph Song, senior U.S. economist at BofA Merrill Lynch Global Research, said he was interested in seeing if Powell says anything about what could lead the Fed to resume raising interest rates again.”

Also on our geopolitical radar remains the Brexit debacle, debate and disaster that seems endless and without cohesion amongst the political parties within the U.K. and the European Union. The latest movement in this ongoing saga is the likelihood of delaying Brexit altogether.

British Prime Minister Theresa May will today bow to pressure and give U.K. politicians an opportunity to delay Brexit if she hasn’t secured backing for her proposed withdrawal agreement by mid-March. The move marks a substantial shift in strategy for May, who has until now insisted that the country will leave the European Union on March 29, with or without a deal.

Her new proposal, which would allow for a short extension to the Brexit process, is an attempt to keep the government together as they muddle through the process that continues to search for consensus.

Shy of all the geopolitical issues and Fed testimony taking place this trading week, retail-reporting season will be intense. With Wal-Mart (WMT), Amazon (AMZN) and Wayfair (W) earnings already proving to surpass analysts’ estimates, some of the more worrisome earnings releases will be released this week.

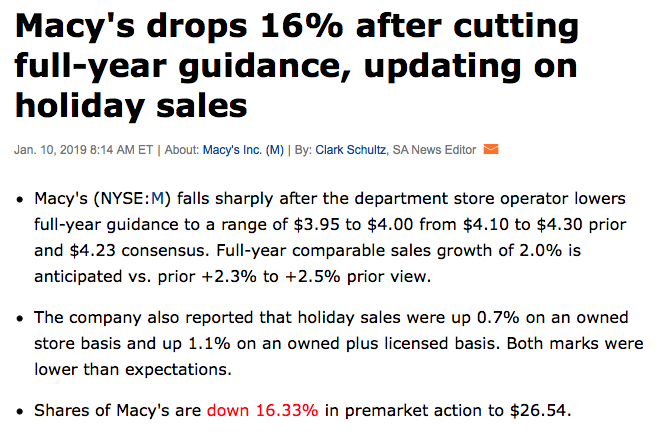

Ahead of the opening bell on Tuesday we’ll see quarterly results from the likes of Home Depot (HD) and Macy’s (M). Both stocks have seen there fare share of depreciation over the last 90 days and even with a modest rebound of late. With the housing sector in a cyclical decline, it remains to be seen if the do-it-yourself retailer can buck the overall retail trend. Macy’s, has it’s work cut out for itself after preannouncing a disappointing holiday season whereby the department store retailer lower its Q4 2018 guidance, siting a slowdown in the month of December. Analysts have cut their ratings and price target for share of M shortly after the January 10, 2019 press release.

While Macy’s undergoes the ongoing battle of navigating through a difficult transition from traditional brick and mortar sales to online sales, management is doing everything you’d want to see a management team doing. The problem remains, however, exercising the many initiatives put forth by the retailer on-scale and without impacting operating profits. The stock is reasonably inexpensive and the executive team has an opportunity to bide time for shares to rebound in price with an upbeat guidance. Nonetheless, we’d be of the opinion that the long-term trajectory for the business and share price is downward and investors might use the opportunity to reduce exposure at higher valuations, if presented.

While the retail sector has seen a rebound with the overall market in 2019, not everybody is convinced that the sector or the sector ETFs are a buy at present levels. In fact, some are of the opinion a sharp fall is in store for the biggest retail ETF, the XRT.

“Retail is a big old mess,” Cornerstone Macro technician Carter Worth said Friday on CNBC’s “Options Action. ” “We know that in so many different ways, but most, of course, is just the poor performance.”

“What you see is a well-defined downtrend,” Worth said of the XRT’s performance over the past year. “It has failed here repeatedly — over and over and over — and what’s to say that it’s going to bust through? Well, some would make that bet, but I’m not going to make that bet. I’m going to make the bet that it’s going to fail yet again.”

“As it’s ascending over the past month, and backing and filling, you’re almost making new 52-week relative lows [against the S&P 500]. So, money committed here is underperforming other things one could have done with one’s money — the definition of no alpha.”

We now have Q4 results from 445 S&P 500 members or 89% of the index’s total membership. With another 39 index members slated to report results this week, we will have seen Q4 results from almost 97% of all companies. Total earnings for these index members that have reported already are up +12.7% from the same period last year on +7.2% higher revenues, with 67.4% beating EPS estimates and 61.8% beating revenue estimates. The table below shows the current scorecard.

There’s room for the market to fall near-term, digest some of its 9-week gains and possibly find a market multiple that reflects a decline in earnings for the Q1 2019 period. At present and with earnings season coming to a close, FactSet estimates that Q1 2019 earnings will decline by 2.7% with revenue growth of 5.2 percent.

As we look ahead to the market’s open, U.S. equity futures are modestly lower. Economic data will center on the housing sector and consumer confidence. The market environment is such that having cash on-hand will likely prove beneficial during a market pullback and while investors jostle with headlines that have little to do with corporate earnings and outside of earnings season.

Finom Group suggests for those who do have plenty of cash on-hand to whether any near-term turbulence in the markets, to take a “light touch” approach; trading small positions, but positions in stocks or with strategies familiar and fundamentally sound.

Please review our daily, Technical Market Recap with Wayne Nelson for additional insights and considerations for the major indexes and futures by clicking the link.