Now that the FOMC meeting is out of the way…but is it really? The event risk is clearly out of the way, but to be sure, the FOMC is more so a fundamental support mechanism of financial markets than ever before and will likely remain as such for the foreseeable future. Under this premise, investors should always be considering the implied market risk/reward with respect to FOMC/central bank financial market underpinnings. Getting off of our soap box…

The Fed’s statement released on Wednesday certainly found favor with investors as much of what investors have desired to see implemented came to fruition. Investors wanted the updated monetary policy outlook to be found even more accommodative and by the action of removing the word “patient”. The market got what it wanted! Below is the revised monetary policy statement from the FOMC.

Information received since the Federal Open Market Committee met in

MarchMay indicates that the labor market remains strong and that economic activityroseis rising at asolidmoderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low.GrowthAlthough growth of household spending and appears to have picked up from earlier in the year, indicators of business fixed investmentslowed in the first quarter.have been soft. On a 12-month basis, overall inflation and inflation for items other than food and energy have declined and are running below 2 percent.On balance, marketMarket-based measures of inflation compensation haveremained low in recent months,anddeclined; survey-based measures of longer-term inflation expectations are little changed. Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 2-1/4 to 2-1/2 percent. The Committee continues to view sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective as the most likely outcomes., but uncertainties about this outlook have increased. In light ofglobal economic and financial developmentsthese uncertainties and muted inflation pressures, the Committee willbe patient as it determines what future adjustments toclosely monitor thetarget rangeimplications of incoming information for thefederal funds rate may beeconomic outlook and will act as appropriate tosupport these outcomessustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.

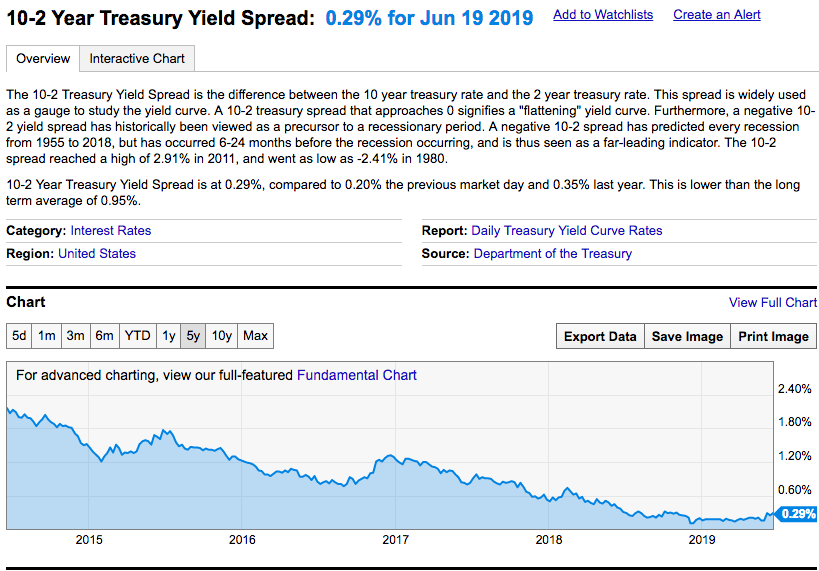

While investors achieved the outcome they most desired from the FOMC on Wednesday, equities had a somewhat modest move as bond yields found lower yields with the 10-yr. Treasury yield edging closer to the 2% threshold. Having said that, the threshold broke overnight to 1.98% and now rests just above 2% Thursday morning. Additionally, the increased probability of the Fed cutting rates, from voting members, has greatly increased, which has found a steepening of the yield curve at the long-end of the curve. The spread between the 2s/10s are now at their steepest level of 2019, some 29 bps.

The yield curve steepening is also a positive outcome from the FOMC meeting. Much of the yield curve movement is a reflection of the Fed more likely to lower short-term rates, identified by the revision to the Fed’s dot plot offered.

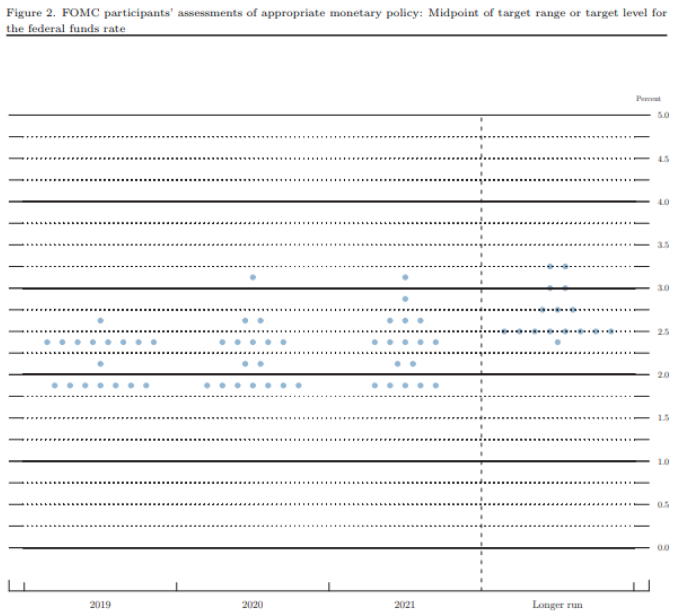

Fed officials themselves appear increasingly divided over the strength of the economy, the direction of inflation and what to do next. St Louis Federal Reserve President James Bullard, who’s warned about low inflation for months, dissented in a 9-1 vote. He favored a quarter-point interest-rate cut. The divisions run deeper judging from the Fed’s projections of future interest-rate moves known as the “dot plot.” Nine Fed officials predict no rate cuts this year while eight forecast one or two reductions. The Fed dot plot does now reflect a quarter-point cut in 2020 owing to a subtle shift in voting patterns, with rates rising again in 2021 to the current target of 2.4 percent.

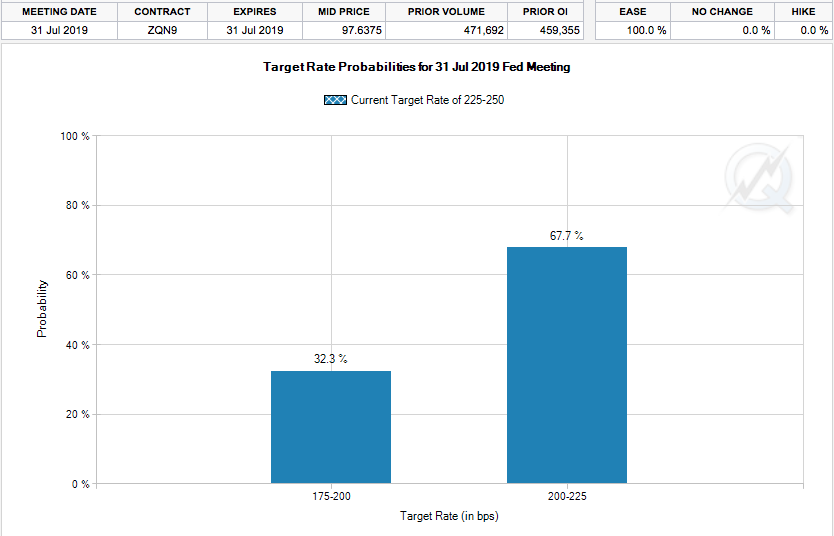

Based on the Fed’s more accommodative policy stance and removal of the word patient, investors have now priced in a 100% probability for at least a 25 bp cut in July. The probability for a 50 bp cut has also risen as of the latest update from the Fed.

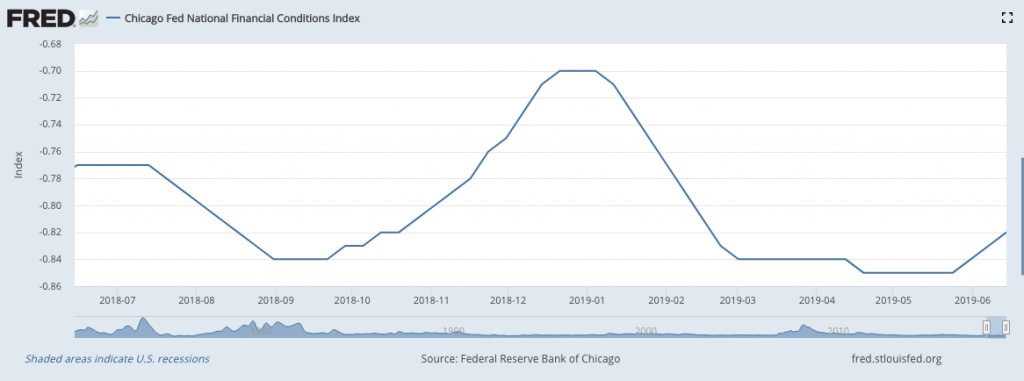

It remains to be seen if the highly followed inflation data continues to support a rate cut by the Fed’s next meeting, but until then market just got another liquidity boost. Even if the liquidity boost doesn’t necessarily read through to financial conditions it will likely resonate within financial market sentiment. We can view financial conditions and liquidity in the markets to understand the key role that they play in determining the trend of the market at any given time and why a dovish Fed which is not hiking rates and moving toward cutting rates tends to boost equity market sentiment through the Chicago Fed National Financial Conditions Index.

The Chicago Fed’s National Financial Conditions Index (NFCI) provides a comprehensive weekly update on U.S. financial conditions in money markets, debt and equity markets and the traditional and “shadow” banking systems. Positive values of the NFCI indicate financial conditions that are tighter than average, while negative values indicate financial conditions that are looser than average. The NFCI has been found with loose financial conditions, but it’s all relative to the cycle and taken on a quarter-to-quarter basis. We can see that with the Fed tightening in September and December in 2018, conditions were tightened greatly and adversely found equity markets in turmoil, falling some 20% from September through December.

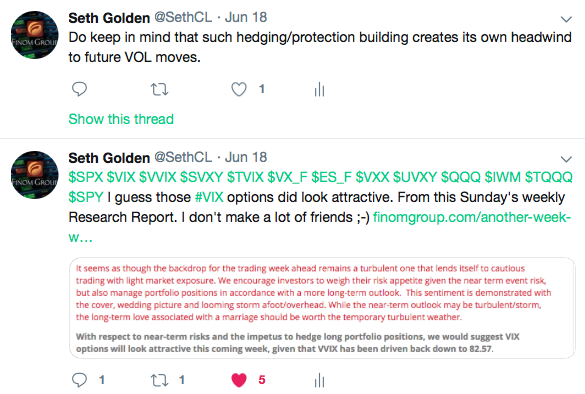

So if you’re just waking up to the equity markets Thursday morning, investors are eyeing a strong rally in equity futures alongside a VIX that has plunged below 14. On Tuesday, investors were found hedging against the binary market outcome imposed by the Fed’s rate announcement to come. The Volatility of Volatility Index (VVX) rose sharply on Tuesday as investors hedged against the potential market reaction to the Fed announcement on rates. Finom Group describes and/or characterizes such hedging activity as hedging “the known-unknown”. The known is the event, the Fed rate announcement. The unknown is the market reaction post the Fed rate announcement. The issue with performing this hedging activity is that it largely creates it’s own failure should volume centered on that same thinking lead to outsized hedging. Finom Group and Seth Golden typically warn against this type of hedging as it rarely works and usually proves to tax a portfolio more so than hedge downside risks. (See tweet below from Tuesday)

Now we fully understand why hedging ahead of “known-unknonw” risk occurs; the price of option premiums… but still!

Something to consider with an even more accommodative-leaning FOMC is the probability of suppressed volatility in 2019 and contrasting how investors viewed volatility coming into 2019. With this in mind we revisit something Finom Group offered to its subscribers in a Research Report issued back on March 17, 2019.

“Investors should not expect the market to continue to rally in a straight line or without a pullback of 3-5% during the calendar year. Even so, given our forecast for an H2 rise in economic activity/output, with stabilization of the Chinese economy Finom Group is forecasting improvements to both earnings and revenues that should find investors buying any such pullback of consequence.

Should this outlook come to pass, we would also anticipate a “VOL 2017-redux” scenario, that finds unusually suppressed market volatility and coincides with a “buy the dip” market mentality prevailing once again. This is also a potential offshoot of the light market positioning to-date that gives way in the H2 period and as fund managers once again play catch-up.”

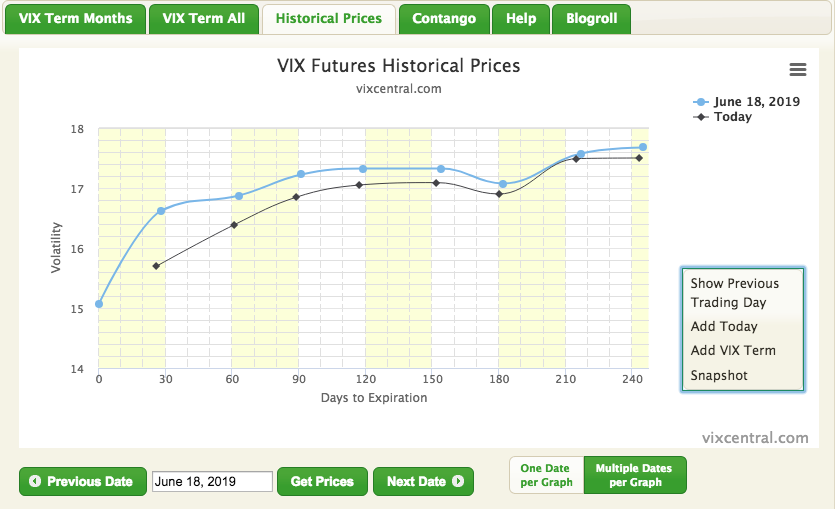

There is an increasing probability for the VOL 2017-redux thesis to be found validated. One way we can see the probability increase for a VOL 2017-redux scenario is by reviewing the VIX Futures Term Structure historical prices data.

As shown in the chart above, the day before the FOMC rate announcement and dovish lean toward a rate cut, the totality of the futures curve was elevated above the present level. Moreover, the front end of the curve, even after monthly VIX futures expiration, has already steepened. We’ll need to see further steepening to validate the duration of this futures cycle correlation to 2017, but we would continue to monitor the probabilities through term structure.

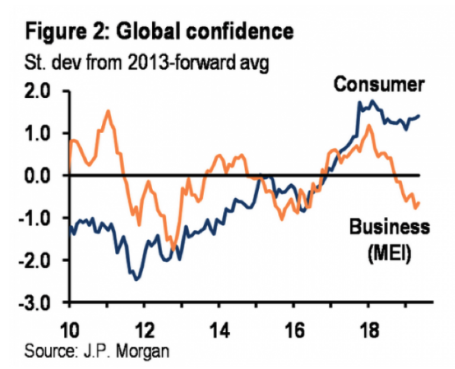

Beyond the Fed investors will now focus their attention on corporate earnings and the upcoming developments from the G-20 Summit meeting between President Trump and President Xi. To reiterate, what investors desire most is a trade truce absent further tariff threats and impositions. The status quo on trade relations would suffice investors and the business community and lead to greater economic certainty, which would likely breed confidence among the business community. One of the greatest impacts to the global economy since tariffs have been imposed in July 2018 has been capital expenditures. While consumers have proven impervious to the impacts from the ongoing trade disputes, the business sector… not so much! J.P. Morgan Chase offers the following sentiment regarding the divergence between households and the corporate sector:

“While the household sector is not immune to geopolitical concerns, fundamentals have held consumer confidence close to cyclical highs at the same time that corporate sector angst has intensified”.

And speaking of earnings, or rather reverting to earnings that continue to come in better than expected ahead of the true launch of earnings season, Oracle reported after the closing bell Wednesday. Shares of ORCL rallied on the beats on the top and bottom line analysts’ estimates. Here are the key numbers:

- Earnings: $1.16 per share, excluding certain items, vs. $1.07 per share as expected by analysts, according to Refinitiv.

- Revenue: $11.14 billion, vs. $10.93 billion as expected by analysts, according to Refinitiv.

The company’s revenue rose 1% year over year in the quarter, according to a statement. Oracle’s largest business segment, Cloud Services and License Support, delivered $6.80 billion in revenue, above the $6.76 billion consensus estimate among analysts polled by FactSet. The Cloud License and On-Premise License segment had $2.52 billion in revenue, over the $2.32 billion FactSet consensus estimate.

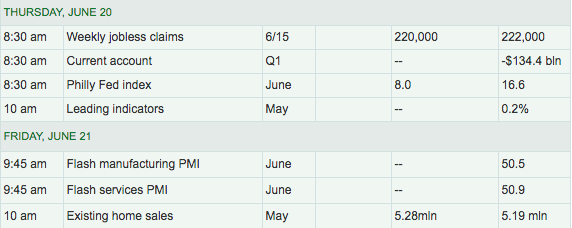

In the 6:00 a.m. EST hour, Dow Futures are pointing to a greater than 200 point rally once Wall Street opens. But that has the potential to find some mitigation if the economic data proves more unfavorable, especially when it comes to manufacturing data. The Philly Fed manufacturing index is due out at 8:30 a.m. and has the potential to mirror the declines in the recent ISM and Empire State Manufacturing data.

After a sharp rise in the Philly Fed last month and with respect to its peer indexes, economists do expect a sharp drop in the index from 16+ to just 8 for the month of May. Jobless Claims and Leading Economic Indicators (LEI) will accompany the Philly Fed data today. With manufacturing and equity prices reeling during the month of May, we don’t anticipate a strong reading from LEI when it is released after the opening of trading on Wednesday.

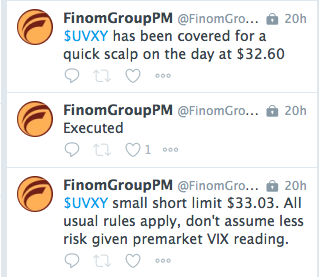

Whatever the day may have in store, Finom Group will continue to monitor market volatility for optimal trading opportunities that we can deliver to our Premium members. (See trade alert issued Tuesday, below)

Take the time today to test drive all that Finom Group has to offer by way of its weekly Research Reports, State of the Markets videos, daily/weekly trade alerts, long-term investing ideas and so much more by subscribing today!