Monday proved to be a rather tumultuous day for global equities, as we largely expected. Over the weekend, Finom Group discussed the flight to safety plays at hand in the market last week, which may prove to foreshadow a turbulent time in the market for the present week. In our weekly research report to subscribers titled Did You Notice The Flight To Safety Last Week?, we offered the following:

“Ok, so we’re going to get off our soapbox for a minute here and before we look at earnings expectations for the Q2 2018 period. Keep in mind come early July, earnings season kicks-off once again. But with regards to last week’s trading activity, the coming week could make or break the market ahead of earnings. We’ve heard of no ongoing negotiations between the U.S. and allies or the U.S. and China recently. Without any beneficial news on trade this coming week, the market may begin to price in worse, not the worst but worse, case scenarios. Again, the market has been incredibly resilient to date so there is also the possibility that it does not. As such, suggesting the worst-case scenario doesn’t seem fitting, but a worse case does. The expected move in the S&P 500 for the coming week is nearly $36 after an expected move of only $31 in the previous week. That’s a pretty big bump in the expectation, signaling the potential for greater volatility in the week ahead.

Given the uncertainty and with last week’s seeming flight-to-safety having taken place, it would probably be best for investors to remain risk neutral with larger amounts of cash on-hand. Should markets take a dip, it may be prudent to put this capital to work in laddered moves. Keeping in mind that, technically markets still look healthy and the overall economic picture is on sound footing, a market hiccup could prove favorable for investors with a long-term horizon.”

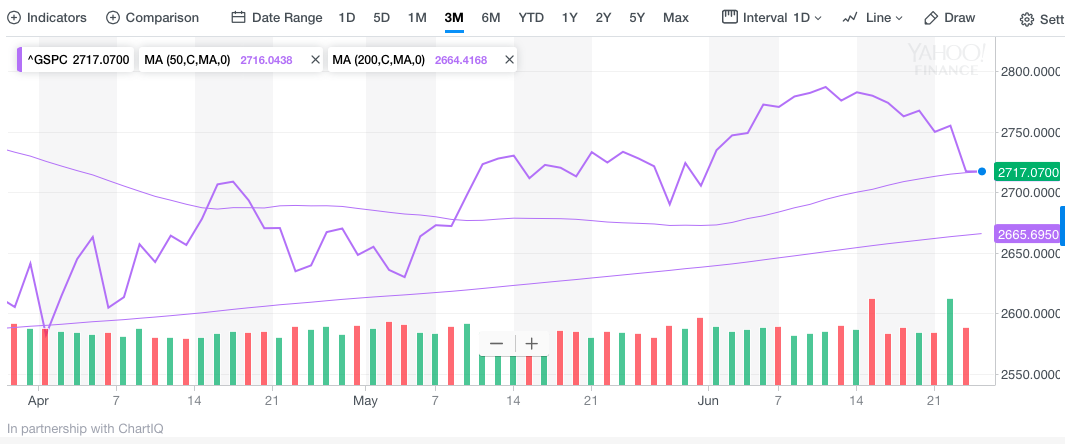

And on the first trading day of the week, the markets did find increased volatility and the pricing in of a worse case scenario with regards to global trade. The Dow Jones Industrial Average dropped 328.09 points to close at 24,252.80, with Boeing and Intel among the biggest decliners in the index. The 30-stock index also closed below its 200-day moving average for the first time since June 2016. The Dow rebounded slightly in the final hour of trading after Peter Navarro, a top trade adviser to President Donald Trump, said on CNBC that investment restrictions against China and other countries are not immediately forthcoming and that the market was overreacting.

The S&P 500 fell 1.4% to 2,717.07, its worst day since April 6, when it fell 2.19 percent. Five of the 11 S&P 500 sectors also closed in correction territory. The Nasdaq composite pulled back 2.1% to close at 7,532.01. The S&P 500 did dip below 2,700 and its 50-DMA briefly in yesterday’s trade before closing slightly above this key level. The Dow closing below it’s 200-DMA has found the index with technical damage that could last a bit longer and as the index also suffered another 10% correction. The last time the Dow 200-day moving average was broken on the downside was in early February.

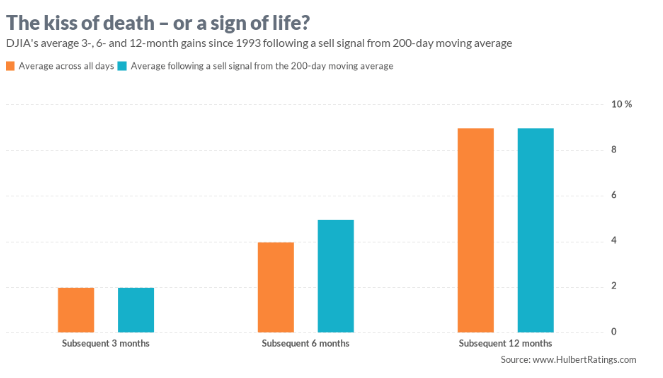

While many assume that breaching the 200-DMA creates a broad-based sell signal, history suggests something quite different. Take a look at the graphic below from Mark Hulbert that indicates the performance of the Dow, over the last 25 years, when it breaches the 200-DMA.

Buying the break of the 200-DMA in the Dow would have actually been the action to take over the last 25 years. Of course history may not deliver duplication of past performance, but not all breaches are created equally or are deserving of knee-jerk reactions from investors.

So what was the cause of Monday’s dramatic decline in the markets? Well it was the very trade concerns that have been looming over the market for months. Those hovering trade clouds became more concerning for investors on Sunday and with the report from the Wall Street Journal. The Wall Street Journal reported Sunday that Trump plans to bar several Chinese companies from making investments in U.S. tech. The newspaper also reported that the administration wants to block additional technology exports to China. Both measures are expected to be announced by the end of the week.

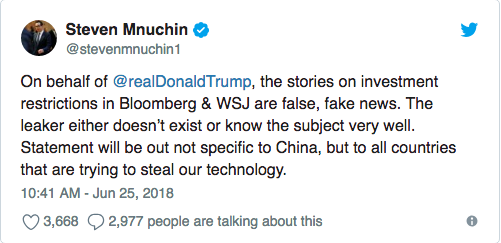

China stocks tumbled overnight on the report and European equity markets followed suit, which forced U.S. investors into a risk-off trade Monday. Later Monday morning, however, Treasury Secretary Steven Mnuchin added a little more color to the Wall Street Journal story with a tweet. Mnuchin called the Journal’s story “fake news” in a tweet. He also said, however, that the measure will impact not just China, but all countries.

There is a difference, believe it or not, between fake news, getting the story wrong and being untruthful. (Nicer way of characterizing a lie) And we’ll get to that in a bit.

With U.S. equities near their lows of the trading session around the 3:00 p.m. hour on Monday, Peter Navarro, one of President Donald Trump’s top trade advisors, said the market was overreacting to fears the administration would restrict foreign investment as part of its trade actions against China and other countries.

Navarro told CNBC that the administration currently does not have any specific countries targeted. His comments came after news reports that had Wall Street reeling over the prospect that the U.S. could prevent companies that had at least 25 percent Chinese ownership from buying businesses that possessed “industrially significant technology.”

“There’s no plans to impose investment restrictions on any countries that are interfering in any way with our country. This is not the plan,” he said.

What are investors to think? What are trading partners and China to think about the ever-changing message and contradictory statements from White House officials on the subject of trade? When you get 3 different stories from which the story originated with the President of the United States and ends with a top advisor to the President, at some point investors and trading partners have to consider somewhere along this chain there exists an untruth in the story or statements. It’s almost comical that we can literally follow the path of U.S. equity markets yesterday and see how, as the markets worsened, there were new statements on trade from the White House. It seemed as if Mnuchin’s tweets/comments were thought to spread fairness of trade tariffs and restrictions beyond just China and that would quell markets anxiety. When that didn’t work and U.S. equity markets faltered further, Navarro attempted the same measure, but with different language/statements that contradicted Mnuchin. Again, what are investors and trading partners to think? Additionally, that is why the concerns over trade are likely to persist until something more concrete develops, for better or for worse.

As it stands, a catalyst for buying equities is not readily recognizable for which it can overcome the trade situation that is littered with uncertainty. Of course the outlook for earnings remains robust and should ultimately lead to higher valuations and higher levels for the major averages, but until investor focus shifts back to earnings strength, a cloud resides over the market. That cloud could loom larger with the S&P 500 narrowly above its 50-DMA.

Although Asian markets stabilized overnight and European equity markets are rebounding somewhat in early trade, it remains to be seen how U.S. equities will perform after Monday’s steep declines. At present, equity futures are pointing to a negative open once again.

Although Asian markets stabilized overnight and European equity markets are rebounding somewhat in early trade, it remains to be seen how U.S. equities will perform after Monday’s steep declines. At present, equity futures are pointing to a negative open once again.