One of the more “confined/restrained” market performance days I’ve seen in recent history. The S&P 500 (SPX) fell slightly and alongside its peer indices on Monday, after futures were pointing much higher. Futures made a u-turn on headlines out of China that proved to confuse investors with regards to last Friday’s trade de-escalation and signaling of a “phase 1” trade agreement of sorts with the United States.

“While the negotiations do appear to have produced a fundamental understanding on the key issues and the broader benefits of friendly relations, the Champagne should probably be kept on ice, at least until the two presidents put pen to paper,” wrote China Daily, the official Chinese state-owned English newspaper.”

It was from that somewhat harmless commentary, which should have been expected, that U.S. futures retreated and stocks were found without true direction during the trading day. Criticisms and caution were always going to play out in the media, both in China and stateside, at least. I wouldn’t be of the opinion that the comments from China are a form of retraction or overtly concerning. With several weeks of ongoing talks and drafting of an agreement to go, it’s only natural for the bait and click machines to do what they are best at doing, creating a hyperbolic narrative of increasing interest.

Having said that, the key takeaway and potential certification of good will and de-escalation between the two trading foes can be assessed more appropriately with the meeting between Chinese Vice Premier Liu He in the Oval Office. Such a meeting carries a heavy weighting, assumes a breakthrough and confirms a bi-lateral path forward.

U.S. President Donald Trump said the first phase of the trade deal will be drafted over the next three weeks. As part of phase one, China will purchase between $40 billion and $50 billion in U.S. agricultural products.

“Phase two will start almost immediately” after the first phase is signed, Trump said in the Oval Office alongside Chinese Vice Premier Liu He.“

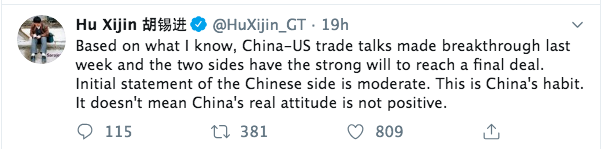

In aiming to confirm a more conclusive sentiment for a breakthrough and determine some of what was issued in the Chinese media as being sensationalistic, we turn to the Global Times of China chief editor:

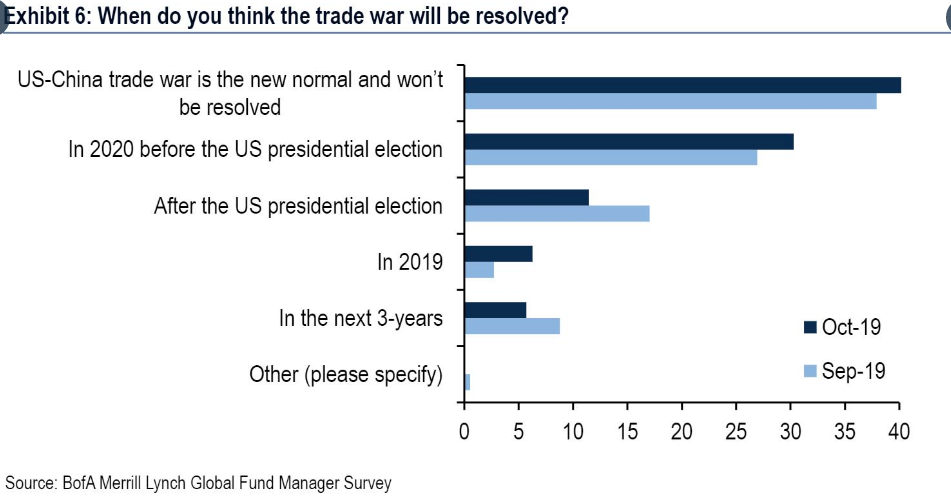

The trade war seems as if it has been ongoing for a decade, even though the reality is far less. Scorn and distrust of headlines on trade has developed alongside woeful sentiment, even when the tide may have turned. According to the latest Bank of America Merrill Lynch fund manager survey (FMS), when asked when fund managers foresee an end to the trade war, the results were less than optimistic.

And while all the “Doubting Thomasinas” value headlines and trade war duration over the actual breakthrough moving forward, it seems as though there’s additional confirmation of increased agricultural purchases from China. The following was reported by CNBC’s Eunice Yoon:

“China will accelerate the purchase of US agricultural products,” says Foreign Ministry when asked about US saying China has started buying. Spox says in 2019 Chinese firms have bought 20mln tons soybeans, 700k tons pork, 700k tons sorghum, 230k tons wheat, 320k tons cotton.“

It’s not hard to find those whom doubt the announced de-escalation and phase 1 trade developments. This is especially the case since the trade war is considered to have the greatest tail risk to the economy according to the FMS.

Even more important is the potential positive affects from these developments on the global and domestic economies. Morgan Stanley’s team of analysts suggest the de-escalation simply isn’t enough to re-energize the U.S. economy and/or consumption.

Morgan Stanley says those who are banking on this trade deal wrapping up are getting ahead of themselves and that the deal with China is an “uncertain” arrangement at best, according to a note from strategists Michael Zezas and Meredith Pickett.

“There is not yet a viable path to existing tariffs declining, and tariff escalation remains a meaningful risk. Thus, we do not yet expect a meaningful rebound in corporate behavior that would drive global growth expectations higher.”

What might be concerning for investors is the latest forward looking technical analysis from Morgan Stanely, as they all-but throw a cold, wet blanket on the trade de-escalation announced.

“Friday’s price action was strikingly similar to what we experienced the last time we had a trade truce on December 1, 2018, at the G-20 meeting .. We expect Friday to mark the near-term highs and the next few weeks/month to resemble what we saw last December ..”

And then there still remains the issue of the December tariffs. Phase 1 coming to a concluding and signed agreement is seen as a “must” in order to avoid future tariff imposition on China, according to Treasury Secretary Steve Mnuchin.

“I have every expectation if there’s not a deal those tariffs would go in place, but I expect we’ll have a deal.”

Goldman Sachs sees a 60% chance that the announced 15% tariffs will take effect, but expects a delay until early 2020 as opposed to the current deadline of Dec. 15. Evercore ISI said it expects a delay and no additional tariff hikes in 2020.

And the ever-popular, permabear and critic of all things economically and politically sensitive to the U.S. markets, Sven Henrich, offered his sentiment on the announced Friday phase 1 initiation in a tweet and Oped via his latest publication at Zerohedge:

“Let me tell you what it doesn’t mean: No company is suddenly going to increase their capex or business investments because in 5 weeks, maybe, something will get signed to buy more soybeans and pork as part of phase 1. They didn’t solve anything, it’s a face saving exercise and gives the Chinese time. Time for what? Time to see how the political situation unfolds in the US.“

Fun fact regarding Zerohedge: The editor of Zerohedge was barred from the securities industry, yet millions of people follow and read it like it’s gospel. Always nice to see that Sven is keeping himself with good company 😉 !

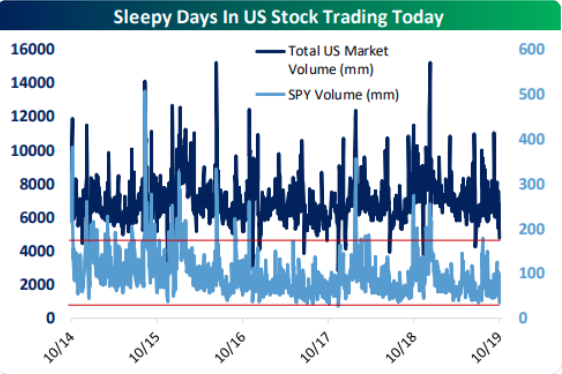

So clearly, market and pseudo-political pundits are not finding their trade feud sentiment shifting with a phase 1 announcement. That being the case, let’s return to our discussion on the market itself, which proved lackluster at best on Monday. The day proved to be the lowest volume, full trading day since December of 2017, and the lowest SPY volume day since November 2017. With the bond market closed and Wall Street pros seemingly held over from a Columbus Day extended weekend, the market held in a very, very tight trading range all the live-long day.

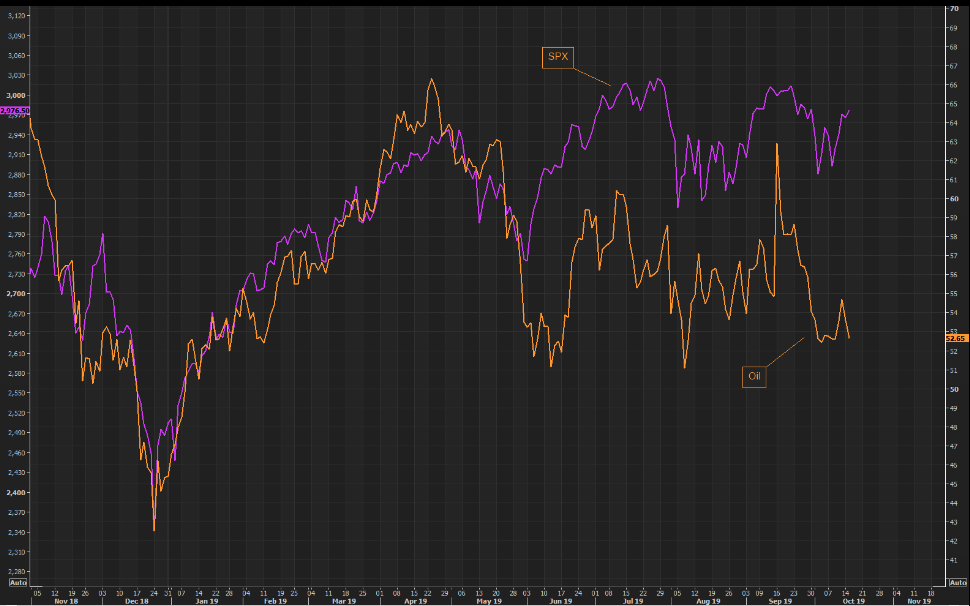

While volume was virtually absent on Monday, investors will awaken to a more favorable indication from Tuesday’s equity futures, which have resumed a sharp uptick. Some of the key issues coming into the trading week will remain front of mind with investors. Earnings season is now officially in high gear and economic data will be more pressing than the prior week’s light data calendar. And all of this as crude oil prices continue to express global demand concerns. The following chart is somewhat concerning, as we usually see a tighter correlation between the S&P 500 and crude oil prices.

As investors, there’s nothing we can do about the look of the chart. but we should respect it for what it may point to going forward. Waning crude prices negatively affects the energy sector earnings performance, and as such, weighs negatively on the S&P 500 EPS outlook. The following outlook and update for the energy sector earnings reporting seasons comes by way of FactSet Data:

- The Energy sector has recorded the largest decrease in expected earnings growth since the start of the quarter (to -31.8% from -13.9%). This sector has also witnessed the largest decrease in price of all eleven sectors since June 30 at -10.6%. Overall, 25 of the 28 companies (89%) in the Energy sector have seen a decrease in their mean EPS estimate during this time. Of these 25 companies, 17 have recorded a decrease in their mean EPS estimate of more than 10%, led by Noble Energy (to -$0.08 from $0.01), Hess Corporation (to -$0.20 from -$0.04), and Apache Corporation (to -$0.12 from $0.20). However, Exxon Mobil (to $0.79 from $1.15), Chevron (to $1.78 from $2.10), and Occidental Petroleum (to $0.55 from $1.00) have been the largest contributors to the decline in expected earnings for this sector since the start of the quarter. The stock prices of all three companies have decreased since June 30.

For the remainder of the trading week, investors will become bombarded by a litany of big bank and financial sector earnings. The docket is extremely heavy Tuesday morning, as depicted in the graphic below:

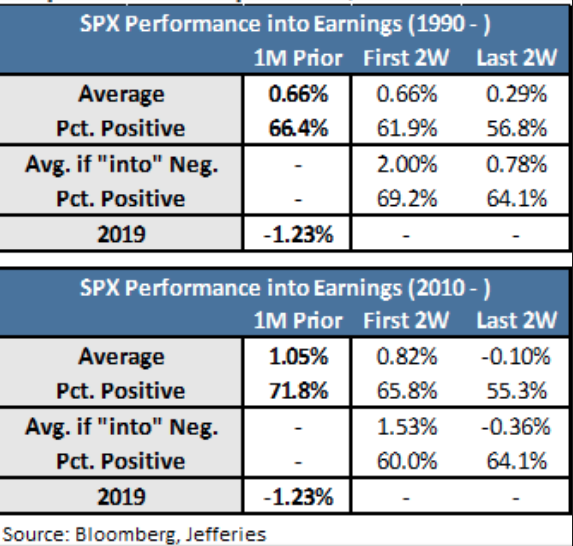

Earnings season is likely to directionally guide markets going forward as markets follow earnings over time. During earnings season, however, trends are also prevalent and apparent.

As shown in the chart above from Jefferies, the S&P 500 typically rises roughly 1% and is higher by some 71% during the lead up to earnings season. Over the first 2 weeks of earnings season, beginning in earnest with the financial sector reporting period, the S&P 500 has risen roughly .8% and has been positive nearly 66% of the time since 2010. It’s not until the tail end of the reporting season that the S&P 500’s performance wanes. This would be expected as overbought conditions from the early reporting season is repealed and profits are taken.

While the big banks will hold court before investors this week, certain Dow Transports (DJT) will also be reporting alongside that pesky tech-media stock, Netflix Inc. (NFLX). Investors definitively desire a better performance out of the tech sector as breadth for the tech-heavy Nasdaq index ETF (QQQ) is struggling and found with concerning breadth. (Chart and comment from Sentiment Trader)

“Last fall, breath momentum for the largest tech stocks diverged from price and then collapsed. This year, it’s arguably similar but worse. It’s now *trying* to curl up. It better keep going.“

Nobody desires to see a repeat of Q4 2018 market performance. While we await earnings results Tuesday and throughout the week, the economic data will lend itself to the macro-outlook. Manufacturing, housing and consumer data will all be revealed this trading week. Due up first will be the latest Empire State Manufacturing Index. The index took a tumble, as expected, in the month of August. Investors will be looking for some type of rebound from the Empire State reading in September.

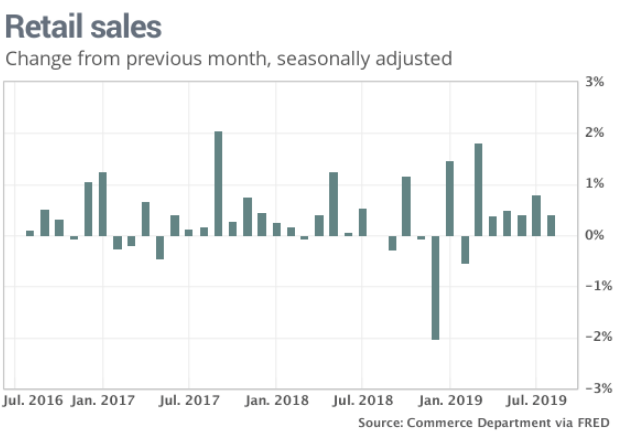

Probably a bigger economic data point being contemplated by investors will be delivered on Wednesday via the monthly retail sales data from the Census Bureau. Retail sales have been resilient and even strong throughout 2019, despite the slowdown and recent contraction in the manufacturing sector.

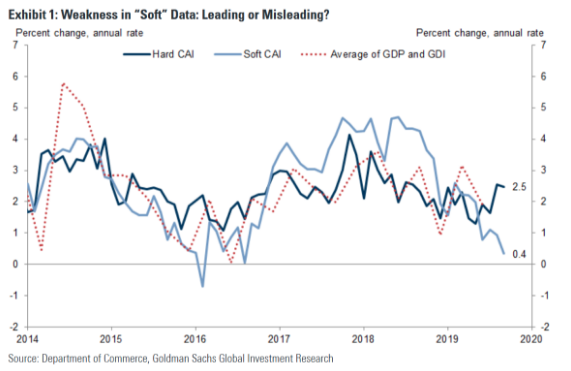

Retail sales data is considered hard economic data, actual sales. Manufacturing data from the likes of ISM or Markit PMI is considered soft economic data, surveys. In recent months, the hard U.S. economic data has diverged from the soft economic data. Many economists are of the opinion it is just a matter of time before the hard data catches down to the soft data. Everyone is just so darn optimistic, aren’t they?

Sentiment or soft data continues to also show divergence. The recent CEO survey suggests CEOs have extreme uncertainty and fear about the strength of the economy going forward. And this, while the latest University of Michigan Consumer Sentiment survey rose to a 3-month high.

“I’m not sure if we’ve seen this disparity between positive consumer sentiment and negative business confidence at this level,” Michael Arone chief market strategist at State Street Global Advisors, told MarketWatch. “From my perspective, something has to give. Either businesses have to be more confident, or you’re likely to see more rollover on the consumer data.”

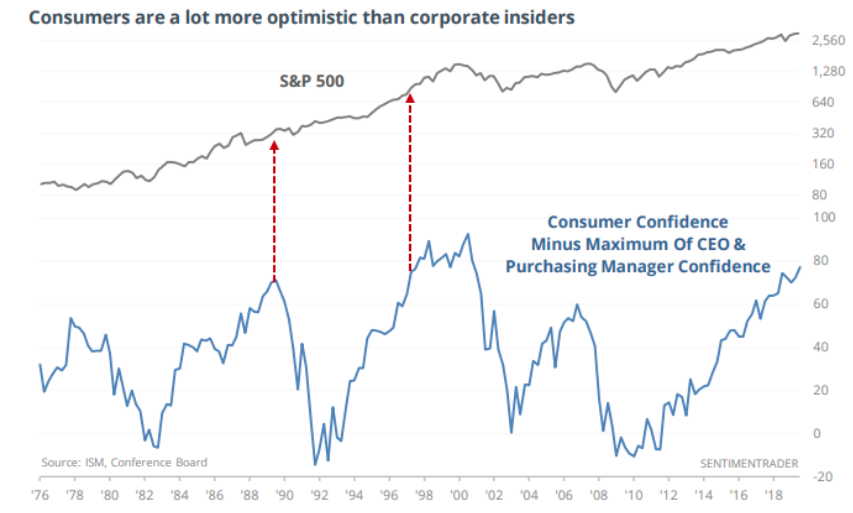

Investors might think that CEOs have a better understanding of the trajectory of the U.S. economy than the consumer, but historically that’s not always the case. Previous instances of high consumer confidence and low executive confidence have actually turned out well for stocks. In fact, the narrative that “dumb money” consumers are optimistic while “smart money” insiders are prepping for a recession sounds really good and bearish. It’s also useless, as determined by the Sentiment Trader chart below:

JJ Kinahan, chief market strategist at TD Ameritrade said that in the near term, it’s unlikely that American shoppers will slow their spending. “People are employed and when they are employed they spend money. Heading into the holiday season, I see no reason why the consumer would slow barring some disaster.”

In terms of seasonality, Finom Group wouldn’t be suprised to see the upcoming release of monthly retail sales indicate some cooling. September is typically a throw-away month as it represents a seasonal gap between the former back-to-school shopping season and the Halloween-Black Friday shopping season. Consumers are typically in saving mode during September and ahead of the holiday shopping season, whereby seasonal product doesn’t typically hit shelves until the tail end of the month. In terms of the strength of the consumer, here is a recent note from Morgan Stanley:

- MS research: “The strength of the US consumer has been the bedrock of the current economic expansion. Just a few weeks ago, in a CNBC interview, Fed Vice Chair Clarida said that “I cannot think of a time where in the aggregate the consumer has been in better shape.” While the US consumer’s balance sheet is in fine shape overall, mainly because levels of debt and debt-servicing costs remain low, there’s a segment whose income statements are under stress – rental households with lower income and lower credit scores. How big are they? Not small, at least on one metric: borrowers with FICO scores below 650 account for about 28% of the population. If the direction of gains in employment reverses, look for the cracks highlighted by our US economics, cross-asset and equity strategy teams to widen. These cracks tend to lead an overall downturn in household creditworthiness, so we’re keeping a careful watch to see if they spread to other segments of consumer debt and eventually creep up the income chain”

There’s a lot of moving parts to the economy and a lot that will take place through the back half of October. Investors would be wise to anticipate the likelihood of continued geopolitical headlines. U.S./China trade relations are moving forward and while a good deal of pessimism surrounds the de-escalation, some are a touch more optimistic.

Andy Laperriere of Cornerstone Macro thinks Friday’s trade truce is likely to hold with the potential for a written agreement to be inked at the APEC meeting in November. A “Phase 2” deal is unlikely to happen before the 2020 elections or at all.

Alright folks, let’s get trading! It’s that time of year for seasonal trends to play a bigger role with investors. J.P. Morgan announced a beat of earnings estimates this morning, so did Blackrock, so did Johnson & Johnson… you get the picture. Additionally, the usual October seasonal dip may be behind us and the seasonality going forward looks strong for the S&P 500, based on the last 30-year period at least.

And trade with us at finomgroup.com. Check out our latest trade alert completed in the below screenshot. Subscribe today and take advantage of our Live and interactive daily Trading Room as well as guided approach to market analysis.