By: SARAH TOY: MarketWatch

Netflix Inc. will get the chance this week to prove its disappointing second-quarter results were just a one-off rather than a recurring problem.

The company NFLX, announces third-quarter earnings results Tuesday after the closing bell. For the second quarter, the streaming giant reported 5.15 million new subscribers, down from 7.41 million the previous quarter and well below the 6.2 million guidance the company gave in April.

Investor confidence took a hit at the time, sending Netflix shares—which were at an all-time high of $419 a share in early July—into a nosedive, falling to $316.78 in mid-August. The stock has since partially recovered and is now sitting at $329 a share.

This earnings season, all eyes will once again be on subscriber growth as investors decide whether the streaming giant’s miss last quarter was really just a blip — or an indication of a more prolonged slowdown.

In the company’s July earnings interview, Netflix’s Chief Executive Reed Hastings didn’t seem worried, chalking the second-quarter shortfall up to simply “some lumpiness in the business.”

“We’ve seen this movie of Q2 shortfall before, about two years ago in 2016,” Hastings said at the time. In 2016’s second quarter, Netflix fell below subscriber growth expectations, but the company has mostly beat guidance since then.

Netflix’s second-quarter miss and subsequent stock plunge also didn’t bug analysts, most of whom stood firmly by their golden child. Piper Jaffray analysts, led by Michael Olson, wrote in July that “the long-term potential is too great for us to suggest anything other than buying Netflix on today’s weakness.

And analysts are generally optimistic about this third quarter. Netflix still leads in the living room, according to a Cowen & Co. survey of 2,500 U.S. consumers published last Wednesday. When asked which platforms users used most often to view video content on TV, 27% of respondents said they used Netflix, followed by basic cable with 20%, broadcast with 18% and YouTube with 12%.

“We view Netflix as a pioneer in online streaming, with further expected growth in subs in the U.S. and expectation for long-term sub growth internationally in existing and new markets,” wrote Cowen analysts, led by John Blackledge.

Netflix churned out a record 676 hours of original programming in the third quarter, well above the 452 hours of the second quarter, according to a Cowen analysis, also published Wednesday. “Netflix’s subscriber forecast is achievable in our view,” thanks to its increasingly robust content slate, continued international strength driven by local originals and set-top box integrations as well as increased marketing around originals, wrote Blackledge.

Imperial Capital analyst David Miller is also upbeat about Netflix’s third-quarter subscriber growth, saying in a note last week that the reports of Netflix testing ways to bypass Apple’s app store overseas are a sign that international subscriber growth is strong this quarter. And in early October, Evercore ISI raised the company’s target price to $350 from $320, citing SensorTower data that showed international downloads of the Netflix app numbered more than 40 million in the third quarter alone.

Citi upgraded its Netflix rating to buy from neutral on Friday, saying the recent sell-off is an “opportunity to own a high-quality, recurring revenue franchise with attractive upside potential.” And although Raymond James and Goldman Sachs recently cut their target prices for Netflix to account for investors’ skittishness over rising interest rates and trade tensions, both firms said long-term prospects for the company remained bright.

But Buckingham Research Group analyst Matthew Harrigan slapped an underperform rating on Netflix with a target price of $305, an 8% downside to the company’s current stock price of $329. The company’s sizable negative free cash flow, which the company estimates will be negative $3 billion to negative $4 billion by the end of 2018, makes it “especially vulnerable to recent interest rate increases,” Harrigan wrote in a note to investors last Monday. The company‘s aggressive use of debt to finance its free cash flow deficits has been a long-time concern among some investors.

Harrigan is also skeptical about Netflix’s prospects in India, which Hastings said in February would be the source of the streaming giant’s next 100 million subscribers. Former Indian finance minister Jayant Sinha has said there are only about 50 million people in India who would qualify as part of the “global middle class,” which poses a challenge for Netflix, wrote Harrigan. The true market for Netflix’s pricing in India could be as low as 25 million, he wrote, and likely not any higher than 50 million.

Netflix’s third-quarter slate included new seasons of “Orange is the New Black,” “Bojack Horseman” and “Marvel’s Iron Fist.” There was also psychological thriller “Maniac,” directed by Cary Fukunaga and staring Emma Stone and Jonah Hill, and the controversial drama “Insatiable.” The streaming company also tied with HBO for total wins at the 2018 Emmys.

Here’s what to expect from Netflix in the third quarter:

Subscriber growth: Analysts polled by FactSet are expecting 5.32 million net additions to the Netflix subscriber base, similar to the 5.3 million figure Netlfix reported for the third quarter of 2017. That’s higher than Netflix’s own forecast of 5.0 million, with 0.65 million from the U.S. and 4.35 million internationally.

Earnings: Analysts polled by FactSet expect Netflix to post earnings of 68 cents a share, a 134% increase from the third quarter of 2017.

Estimize, which crowd sources estimates from buy-side and sell-side analysts, fund managers, academics and others, is expecting EPS of 71 cents.

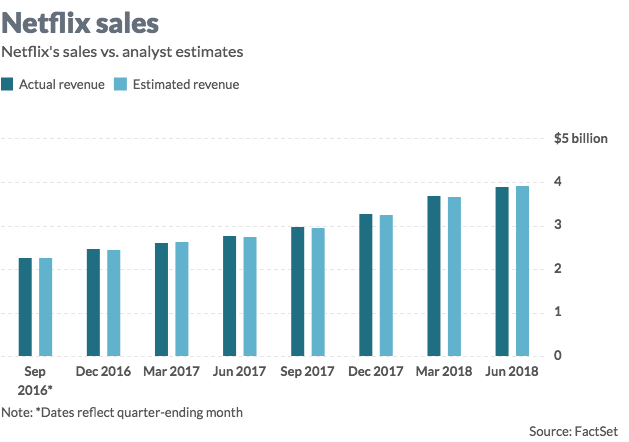

Revenue: Analysts polled by FactSet expect revenue of $3.9 billion, with $1.94 billion in domestic streaming revenues and $1.97 billion in international streaming revenues. Domestic DVD-by-mail revenue is expected to be $88 million. Netflix reported revenue of $2.98 billion in the third quarter of 2017. Estimize pegs revenue at $4.0 billion.

Stock movement: Netflix shares were trading just above $322 Thursday afternoon, a drop from its mid-summer high of nearly $419, but 68% above where it ended 2017. The S&P 500 SPX, has gained 2.8% year to date.

Of the 44 analysts on FactSet who cover Netflix, 27 rate the stock a buy or overweight, 13 are neutral and four are at underweight or sell. The average target price is $382.66, which is about 19% above current levels.

Looking ahead: Investors should keep an eye on Netflix’s fourth-quarter plans, any specifics on their plans for growth in India, and, as usual, any commentary on future content spending. Netflix’s fourth-quarter originals roster includes the final season of “House of Cards” and the debut of “Chilling Adventures of Sabrina,” based on Sabrina the Teenage Witch.

The FactSet consensus for fourth-quarter net subscriber additions is 8.35 million.