With Asian equity markets finishing nicely in the green overnight, European markets aren’t following suit as of yet. Nonetheless, U.S. equity futures are largely higher, but anything can happen between now and 9:30 a.m. EST when Wall Street opens for trading. That has been the trend, the unpredictability of the market, which has been on a roller coaster ride through February 2018.

After rising post the release of the latest Fed minutes this past Wednesday to 2.95%, the 10-year U.S. treasury yield has retreated somewhat. The yield is lower this morning and broken below 2.90% once again. Given market jitters that are correlating to rising rates and bond yields, investors might expect increased volatility in equity markets to persist until an equilibrium between inflation/reflationary fears justify market multiples and/or equity valuations. The debate will seem to carry on with regards to whether or not the bull market is in dire jeopardy of subsiding and yielding to…rising yields or the potential for an inverted yield curve. What we would recommend to investors at Finom Group, is to simply maintain an active participation in managing one’s portfolio and dedicating oneself to managing risk as the debate surrounding the bull market carry forward.

Speaking of inflation/reflation and as it pertains to the outlier that may have been the sharp increase in wages reported in the January Nonfarm Payroll report, U.S. Treasury Secretary Steven Mnuchin recently spoke on the topic.

“There are a lot of ways to have the economy grow … You can have wage inflation and not necessarily have inflation concerns in general,” Mnuchin said Thursday in an interview with Bloomberg. “One of the reasons why the president won the election is because most middle-class Americans had very little wage growth,” he said in the interview.

Konstantinos Anthis, head of research at ADS Securities, expressed doubts about Mnuchin’s thesis.

“Whether his assessment will prove to be true or not remains to be seen, even though it sounds more like wishful thinking than an actual estimate of inflation growth in the U.S,” he said in a note.

As usual, opinions will vary amongst analysts and economists alike. In terms of the consumer confidence and consumer spending, which is the largest portion of the U.S. economy, the data continues to come in favorably.

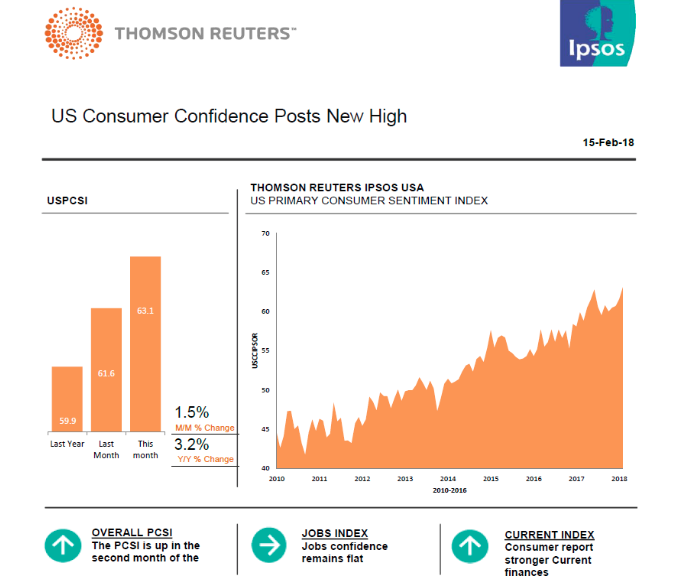

“American consumer confidence as measured by the Thomson Reuters/Ipsos Primary Consumer Sentiment goes into February 2018 continuing its forward progress to stand at 63.1. This is up a point and a half from last month and marks a new post-recession high. Jharonne Martis, Director of Consumer Research at Thomson Reuters, said, “Consumer confidence has a big impact on spending. The recent improvement is also reflected in The Thomson Reuters Retail and Restaurant earnings index, which has experienced a significant upward revision. The index is expected to grow 7.6% for the current quarter, up from 5.4% last month.”

In other news, the Securities and Exchange Commission may be rolling back Obama-era standards that would require mutual funds to tell shareholders about large holdings of hard-to-sell assets. The SEC had planned to propose rolling back the disclosures on Wednesday. Regulators postponed the action because commissioners have disagreed over the scope of the rollback as reported. The SEC said, in a notice posted Thursday, that it anticipates holding a vote in the future with regards to the subject matter.

In 2018, equity markets will likely continue to grind out another annual gain, but how they achieve the gains might greatly determine a portfolio’s performance. Active portfolio managers tend to do better in periods of increased volatility that coincide with corporate earnings growth. But when throwing higher rates into the “market mix”, uncharted territory may be ahead. As I noted coming into 2018, markets and market volatility will not mirror that of 2017. I foresee greater implied volatility persisting for months to come, but from the level of today and compared to the mean VIX of 11 in 2017, that still leaves room for volatility to subside somewhat from here/today, and yet still be elevated year-over-year.

Many have blamed volatility sellers for recent market woes in favor of appreciating stretched market valuations and the general fears from rising rates that are actually manifested…in volatility. For every action there is a reaction and where we experience the affects we look for low-lying causation and that is where many media pundits have found the short-VOL crowd with culpability. Right or wrong remains to be determined, but it could easily be offered that no one variable caused the market to correct. Nonetheless, equity markets have not yet stabilized and volatility sellers are still coming under fire. What I often find comical is that general asset managers and long-only fund managers that perpetuate rational risk/reward management of assets don’t find fault with the existence of the VIX, just how it has developed into a complex of derivative instruments. I guess we are supposed to believe that is not how the commodity complex has developed?

More importantly for the short-VOL crowd and the volatility complex will always be the manner of participation consistent with generating annual returns. Volatility has rhyme and reason-ing despite those who claim to the contrary: It will always rise and always fall thereafter as a correlation to SPX options existence. Volatility is ever-changing or morphing from one year to the next. And it is for these reasons that participation in the volatility complex should also be ever adaptive to such changing. Up to and through 2017, UVXY was my VIX-ETP of choice or preference. But coming from such low realized volatility levels in 2017 and from a risk management perspective in 2018, I chose/choosing to limit exposure to UVXY and TVIX. These double-leveraged VIX-Exchange Traded Products (ETP) carry greater risk in an environment with higher implied volatility and along the lines of liquidity. Naturally, they also carry with them a higher reward as volatility relaxes in time. On the other hand, VXX carries with it a lesser risk during periods of higher implied volatility given its lesser leverage than the former offered ETPs. There is a host of VIX-ETPs to choose from and the following list offers those that have the greatest liquidity and there corresponding leverage.

- 2x Long (Leveraged) – Short-Term VIX Futures

- UVXY = ProShares Ultra VIX Short-Term Futures ETF

- TVIX = VelocityShares Daily 2x VIX Short-Term ETN

- 2x Long (Leveraged) – Medium-Term VIX Futures

- TVIZ = VelocityShares Daily 2x VIX Medium-Term ETN

- 1x Long (Unleveraged) – Short-Term VIX Futures

- VXX = iPath S&P 500 VIX Short-Term Futures ETN

- VIXY = ProShares VIX Short-Term Futures ETF

- VIIX = VelocityShares VIX Short-Term ETN

- VMAX = REX VolMAXX Long VIX Weekly Futures Strategy ETF

- 1x Long (Unleveraged) – Medium-Term VIX Futures

- VXZ = iPath S&P 500 VIX Mid-Term Futures ETN

- VIXM = ProShares VIX Mid-Term Futures ETF

- VIIZ = VelocityShares VIX Medium-Term ETN

- 1x Short – Inverse (Unleveraged) – Short-Term VIX Futures

- SVXY = ProShares Short VIX Short-Term Futures ETF

- VMIN = REX VolMAXX Short VIX Weekly Futures Strategy ETF

- XXV = iPath Inverse S&P 500 VIX Short-Term Futures ETN

- IVOP = iPath Inverse S&P 500 VIX Short-Term Futures ETN II

- XIV = VelocityShares Inverse VIX Short-Term ETN (expected to be liquidated on 21 February 2018)

- 1x Short – Inverse (Unleveraged) – Medium-Term VIX Futures

- ZIV = VelocityShares Inverse VIX Medium-Term ETN