It was a topsy-turvy trading session yesterday with the Dow giving up more than 120 points during the trading session before finishing nearly flat. The Dow ended 14.25 points, or less than 0.1%, lower at 24,448.69, closing with losses for a fourth straight session. The S&P 500 index closed virtually unchanged at 2,670.29. The Nasdaq Composite Index shed 17.52 points, or 0.3%, to 7,128.60.

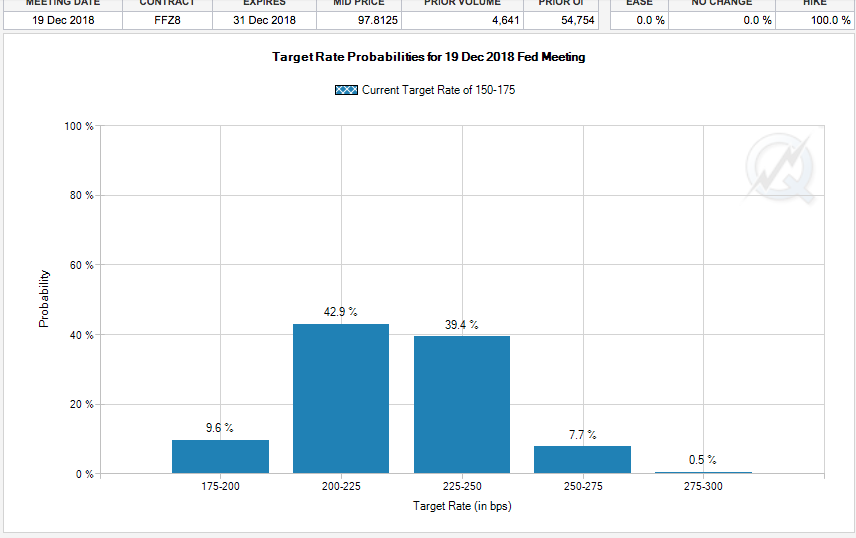

Yesterday’s market action and swings from positive territory to negative territory to largely flat territory came as a reaction to the 10-year Treasury yield traveling higher. The 10-year Treasury note yield hovered around 2.9729% yesterday, the highest level since January 2014, but had moved above 2.995% at one point. Rising yields and rising Fed funds rates have given rise for investors concerned over risk/reward and the potential for a yield curve to invert. We discussed this in our most recent article titled “4th Rate Hike Coming? Tech Titan Earnings Week Ahead!” In the article, Finom Group discusses the probability of a 4th rate hike being priced into the market via the Fed Fund Futures December contract. To end the previous week, investors were pricing in a 38.6% probability of a 4th rate hike, one more than the FOMC has previously indicated via their rate path/dot plot. Since then, the probability has increased by nearly 1% and as many feel the Fed may find itself behind the curve. (See Fed Fund Futures December FFZ8 contract below)

Finom Group’s Chief Market Strategist has outlined the relevance of a 3%, 10-year Treasury as “nothing more than a water mark number” that is still extremely low historically.

“It’s higher than we’ve seen in recent years, but investors shouldn’t be fearful of the yield number, they should expect it given the Fed’s decision to unwind its balance sheet and inflation mandate. The list can literally go on and on as to why investors should expect a 3% number at this stage of the economic cycle”.

Moreover, when juxtaposed with the rate of corporate earnings growth and an economy that is seemingly humming along, the Fed normalizing rates should be seen as a positive. Ben Rogoff of Polar Capital Partners echoes much of Golden’s sentiment in his recent interview with CNBC. He told CNBC Monday that the real concern would be when the interest rate on that bond neared 3.5%, and even higher.

“I think somewhere between there (around 4 percent) and where we are today, there’s trouble ahead and I think that really does explain the change in volatility that we are seeing in markets.”

“Rogoff believes that at 4 percent for the U.S 10-year, pension funds around the world start to immunize their portfolios. He added that the relative attraction of bonds over equities changes at 4 percent. He added that at 3.5 percent, equity markets struggle to expand their PE (price-to-earnings) ratios — which is an important metric used by traders to gauge the value of a company’s stock.

One of the main concerns for investors when it comes to higher yields is the higher borrowing costs associated with such periods of reflating yields. Many companies have taken advantage of low interest rates/borrowing costs since 2009 and as the FOMC set itself and the economy on a path of low rates and increased liquidity. Finom Group does believe that borrowing costs, alongside rising rates, does portend to become a headwind for the equity markets over time. This will likely reveal itself in the curtailment of multiple expansion. As such, while corporate earnings are growing at a cycle-high rate, multiple expansion may be limited and equities may simply appreciate as earnings growth proliferates according to what may prove a cyclical peak.

We are now in the heart of earnings season with the majority of S&P 500 companies reporting this week. Google’s parent company Alphabet reported after the closing bell yesterday and managed to handily beat analysts’ estimates. The search giant beat estimates, but concerns about rising costs muted any positive sentiment for shares in the after hours trading session. Alphabet reported earnings of $9.93 a share, while first-quarter revenue of $31.15 billion topped estimates of $30.29 billion. Net profit soared 73% to $9.4 billion. For the second quarter in a row, TAC equaled 24% of Google’s ad revenue vs. 22% a year earlier. Eric Jhonsa of The Street.com offers 10 key takeaways from Alphabet’s reported quarter as follows:

- Google emphatically put to rest any concerns that its mobile search and YouTube ad momentum was about to meaningfully slow. Paid ad clicks on Google’s own sites and apps (they include video ad views that technically aren’t “clicks”) rose 59% annually, outpacing Q4’s 48% growth. This more than offset a 19% drop in cost per click (slightly worse than Q4’s 16% drop), the result of mobile search and YouTube ad prices being lower on average than PC search ad prices.

- CFO Ruth Porat noted mobile search was once more the largest driver behind Google’s ad growth, and both Porat and CEO Sundar Pichai sounded upbeat about search ad trends. Though there have been worries about Amazon.com’s impact on Google Search, both due to the growth of Amazon’s ad business and the tendency of Amazon shoppers to go straight to its site/apps, Google Search remains a one-of-a-kind online marketing vehicle — including for many businesses that are either competing against Amazon or operate in an industry that Amazon isn’t involved in. And like Amazon, Facebook and others, Google is benefiting from the steady shift of advertising dollars towards online channels.

- TAC — the ad revenue-sharing payments Google makes to the likes of phone OEMs, carriers and publishers — remains a real headwind. For the second quarter in a row, it equaled 24% of Google’s ad revenue versus 22% a year earlier. Moreover, Porat forecast TAC’s share of ad revenue on Google’s own sites and apps (13% in Q1) will continue rising, albeit at a slower pace starting in Q2. A revamped search ad revenue-sharing deal with Apple is believed to be contributing to TAC growth in recent quarters.

- Elevated hardware/service costs also raised eyebrows. Alphabet’s “other cost of revenue,” which excludes TAC, rose 39% annually to $7.2 billion. That’s higher than Q4’s 34% growth, even though Q4 is a seasonally big one for hardware sales. Porat blamed rising depreciation expenses (the result of heavy capex), YouTube content spend and rising hardware-related expenses.

- Capex soared in Q1: Google’s “purchases of property and equipment” jumped to $7.3 billion from a year-ago level of $2.5 billion. Porat noted this figure includes the $2.4 billion purchase of Google’s Chelsea Market Manhattan facility, and that overall about half of Q1 capex was related to spending on facilities rather than “compute capacity.” But with a portion of year-ago capex also involving facilities, this suggests compute investments still rose sharply. While chip suppliers such as Intel, Nvidia and Broadcom can’t complain, all this spending will lift Google’s depreciation expenses in future reports.

- Earnings benefited from the fact that Google had just an 11% Q1 tax rate, down from 20% a year earlier. Tax reform played a role, and the aforementioned accounting changes had a 5-percentage-point impact. EPS also got a small boost from $2.17 billion worth of stock buybacks; that’s up from $1.13 billion a year ago.

- The Google Other reporting segment, which covers non-advertising businesses such as hardware sales, Google Play transactions, the G Suite (formerly Google Apps) and the Google Cloud Platform (GCP), had another strong quarter: Revenue rose 36% to $4.35 billion. On the call, Pichai noted the G Suite saw accelerating revenue growth in Q1, and that GCP is seeing stronger large-deal activity.

- The Q1 report was the first one for which the Nest smart home hardware unit was placed within the Google Other segment, rather than the “Other Bets” segment. Google also restated its 2017 results to reflect the change. Based on the restatement, Nest had 2017 revenue of $725 million, but also posted a $621 million operating loss. On the bright side, Pichai said that Nest, which was just merged with Google’s core hardware team, sold more devices in 2017 than in the prior two years combined.

- Two slower-growing parts of Google’s ad empire — PC search and ad sales on non-Google properties — did well in Q1. Porat mentioned Google saw “solid growth” in desktop (PC) search in Q1, and Pichai suggested the large investments Google is making to enhance its mobile search experience “translates to desktop search as well.” Ad sales on “Google Network Members” properties grew 16% to $4.64 billion ($1.25 billion excluding TAC); ad impressions were flat, but Google’s average cost per impression rose 18%.

- Pichai didn’t sound worried about the pending arrival of new EU online privacy regulations (GDPR), which among other things require companies to get users to explicitly opt in to any collection of their data for ad-targeting purposes. He mentioned Google was been working for over 18 months on GDPR compliance, and suggested that — since it relies heavily on the keywords a user inputs — its search ad business won’t be significantly affected by it.

Earnings results will continue to roll in today and will be carefully considered by investors. Such results are expected Tuesday from 3M Co., Caterpillar Inc., Coca-Cola Co., Verizon Communications Inc., United Technologies Corp., Travelers Cos., Eli Lilly & Co., Harley-Davidson Inc., Biogen Inc., Texas Instruments Inc. and Lockheed Martin.

With U.S. equity futures higher this morning and the 10-year Treasury stabilizing, investors will also consider the light economic data calendar for April 24th. The Case-Shiller home price index for February is due at 9 a.m. Eastern Time, followed by the April consumer confidence index and new home sales data for March at 10 a.m. Eastern.

Finom Group believes equity prices are heading higher and rationalizes their beliefs through fundamental analysis on the economy and corporate earnings. In the firm’s most recent report, Seth Golden highlights that earnings growth expectations continue to rise for the Q1 2018 period. From one week to the next, Thomson Reuters ratcheted up their Q1 2018 earnings growth expectations from 18.6% to 20%, as of April 21st. Even as earnings growth expectations and forecasts rise without a more meaningful boost to the benchmark S&P 500, there remain trading opportunities with ample confidence to execute due to the fundamental outlook for corporate earnings. The longer-term forecast is that eventually the S&P 500 will be found appreciating by year’s end and finish higher than in the previous year.

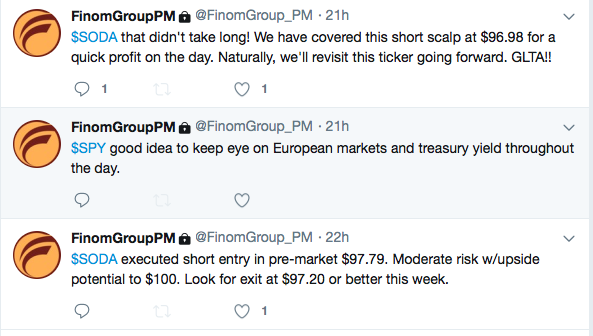

Moreover, yesterday Finom Group delivered 2 such trading opportunities to subscribers and via it’s private twitter feed. (subscription needed) During the pre-market trading hours, Seth Golden shorted shares of SODA at what would prove to be a high intraday trading price of $97.79. Once the market opened, the share price retreated to the desired profit target of $97.15. The trade dissemination/alert to finomgroup.com subscribers is depicted below.

As the trading session carried forward, Golden was eyeing a trade in the short-VOL strategy and VIX complex, for which he is best known.

As depicted in the screenshot above, Golden entered a short VXX position at $42.11, as the VIX began to elevate from intraday lows. This morning and with the VIX decaying as equity futures rise, this trade has been covered in the premarket at $40.85 and for a healthy profit. (Golden Capital Portfolio maintains a core, short holding in shares of VXX) Finomgroup.com welcomes new subscribers!

It remains to be seen how long investors can avoid the lure of rising earnings in favor of rising yields and rate-centric fears. With that being said, trade what is in front of you and with respect to the fundamental underpinnings of the market.