The weekly expected move for the S&P 500 this week is $37/points. The S&P 500 has now fallen for 3 consecutive days and with media headlines blaming the decline on U.S./China negoitations and economic data (ISM Manufacturing). With the S&P 500 coming into the week at 3,147, just 9 points off its all-time record high levels, it has fallen sharply this week and already breached the weekly expected move to the downside. What lay in store for the S&P 500 next is anybody’s guess, but it may hinge upon those headlines… or not.

While the media will offer many different or even a more pressing reason for the market to draw lower, I’m of the opinion that overbought conditions combined with excessive optimism in a rather complacent market lent itself to any reason offering the market an excuse to selloff. Reasons are a dime a dozen, but excuses can often drive the action. Remember what we said in Tuesday’s Daily Market Dispatch, as follows:

“Sometimes, yes sometimes there’s no real reason for a market to drawdown, but rather excuses. The aforementioned reasonable means for the market’s reaction may have simply provided the market a natural excuse to selloff. Keep in mind, the market has been in overbought, frothy territory for the last several weeks.”

With Tuesday’s commentary and analysis in mind, now watch the latest on-air video of Canaccord Genuity’s chief equity market strategist Tony Dwyer, with CNBC here…

During the interview, Dwyer mirrors the commentary and analysis of Finom Group by stating that headlines and data were nothing more than EXCUSES for the market pullback. Sometimes, it’s nice to hear another analyst draw the same conclusions on market action that you’ve previously outlined. Nonetheless, with the S&P 500 closing below 3,100 on Tuesday, investors have managed to work off some of the froth that developed over the last couple of months.

During the latest drawdown in the S&P 500, the market has already filled one gap to the downside at 3,111, on Monday. The next gap doesn’t come into the picture until 3,046 only to be followed by further downside to the 50-DMA at 3,033.

In terms of falling down to an “accomplishment” during Tuesday’s trading session, the bulls managed to make a stand at another key level. According to Nomura’s equity strategist Charlie McElligott, the key gamma level came into play on Tuesday as the market selloff continued from Monday, but with greater volatility.

“‘sell’ levels looking at SPX options, we see the Dealer $ Gamma position nearing the potential ‘flip’ level to ‘SHORT GAMMA’ ~ 3073 (spot 3083 last), which would of course beget more selling [to] hedge the lower futures travel” – Nomura’s Charlie McElligott

The S&P 500 did breach the 3,073 level briefly, but made a stand and rallied in the afternoon to finish near the highs of the trading session. One might say that in both of down trading days this week, the bulls actually managed to claim victories. In further speaking of victories or at least a healthy distribution period, the market has also worked off a good deal of extreme sentiment.

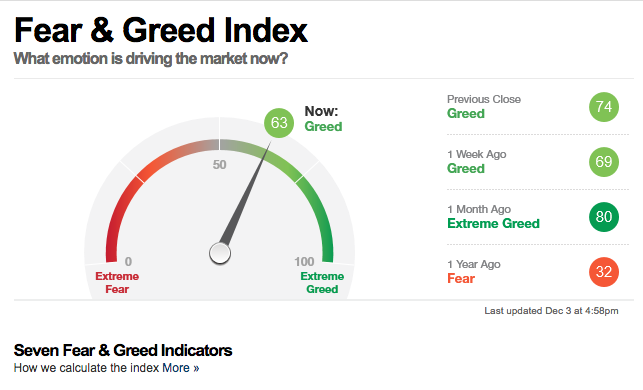

For several weeks, the CNN Fear & Greed Index has resided in extreme greed territory. The index read 75 coming into the Tuesday trading session, but finished the day at 63, where it will begin the trading day on Wednesday.

U.S. equity futures had been pointing lower overnight and heading into the Wednesday trading session. President Trump’s suggestion that a trade deal may not be inked until after the 2020 Presidential election offered the market a an excuse to selloff and reconsider the probability surrounding the December 15 tariff imposition.

“In some ways, I think it’s better to wait until after the election, you want to know the truth,” Mr. Trump said after meeting with NATO Secretary General Jens Stoltenberg in London before U.S. markets opened on Tuesday.

To be clear, Finom Group remains of the opinion that should the U.S. White House Administration go forward and implement the December tariffs, it would prove the undoing of the markets in December. We would be of the opinion a good 10% market correction would ensue before the White House Administration altered the tenor of trade talks and trade relations with China. But here’s the problem, should the tariffs become realized, the market retrenches some 10% and then the White House Administration decides to rethink their trade relationship with China and the implemented tariffs:

- You can only push investors so far, when they’ve been on the edge and found net sellers of equities for the whole of 2019.

- The final trance of tariffs on December 15th would directly impact consumer goods.

- There’s no win or way for the market to sidestep the last tranche of tariffs. If the tariffs are imposed, corporations will either absorb the cost of the tariffs that will curtail profits or they will pass along the price increase, which may prove to curtail demand… which would also cut into profits. Either way, the market would likely adjust lower to account for the EPS drag.

- It’s the final straw for corporations when it comes to trusting the White House Administration, which has already been at low levels if one considers CEO confidence surveys and general CAPEX levels.

- Imposing the December 15th tariffs combined with a market selloff would likely be felt on “main street”, cutting off holiday spending at a critical point in the retail holiday season.

- A second annual market selloff during the holiday season would not be short-lived by the consumer, consumer sentiment and consumer spending going forward. Fool the consumer once, shame on you. Fool the consumer twice during the holiday period and the retribution will be longstanding in the economy.

- These tariffs and the direct hit to the consumer, the largest contributor to the U.S. economy, would not be found with a rebound for upwards of 6 months without a swift removal of said tariffs.

- Considering the calculus of the ongoing trade negotiations, the last tranche of tariffs would likely, also, eliminate any positive sentiment that remains between the U.S. and China and with regards to a trade deal of sorts. China’s desire for a rollback of certain tariffs that would be met with additional tariffs would likely prove the last straw for Chinese officials. The U.S. would have played its “final hand” in this calculus, leaving them with little ammunition to repeal former actions as China would solidify hopelessness in the negotiations with the White House Administration and trade counter party.

In short, if the U.S. was to impose the December 15th tariffs it would likely create finality on many fronts including trade negotiations, equity market sentiment and the bullish trend, consumer spending growth and/or the current Fed rate cut pause. Yes, the Fed would likely be forced to recommence rate cuts. At this point in the calendar year, all that matters to the market is will the December 15th tariffs be implemented. Here is what State Street Global Advisors Michael Arone offers on the subject matter of tariffs:

“In order for the market to break through to new highs, we need resolution on trade, especially U.S.-China trade. I think you can see that each time the market makes new all-time highs, trade tensions escalate and markets become more volatile and sell off. That happened in May, and August, and now in the last couple of days. It’s become a vicious cycle.

I do think much of December’s action is going to hinge on the trade decision and the headlines and certainly the 15th is the date that is going to overhang the market until there’s some sort of definitive news.”

In addition to Arone’s comments, if we take the December 15th tariffs a step forward and are found without the probability of a trade deal/truce, here is what Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets had to offer in this regard:

“Taken at face value though they indicate that the trade war would be a “semi-permanent” facet of global commerce throughout next year.

And it’s also not difficult to imagine a “no-deal”-based Trump re-election campaign despite conventional wisdom to the contrary. In that scenario, Trump would campaign as the only candidate capable of pushing forward his trade agenda.

The market implications of ‘no deal’ are ostensibly straightforward; trade-war-inspired global uncertainties will limit the upside for risk assets and put a ceiling on how far Treasury yields can increase in any bearish episode. This is complicated by the fact that by kicking the proverbial can beyond Nov. 3 (next year), Trump may be eliminating the ‘risk-on’ potential from even the watered-down/phase-one compromise.”

Fortunately, ahead of the opening bell on Wall Street for Wednesday, a new and more optimistic trade headline has surfaced from Bloomberg.

“The U.S. and China are moving closer to agreeing on the amount of tariffs that would be rolled back in a phase-one trade deal despite tensions over Hong Kong and Xinjiang, people familiar with the talks said.

The people, who asked not to be identified, said that U.S. President Donald Trump’s comments Tuesday downplaying the urgency of a deal shouldn’t be understood to mean the talks were stalling, as he was speaking off the cuff.“

The comments and reporting from Bloomberg seem believable. After all, the President’s comments in London on Tuesday were nothing new. We’ve heard such rhetoric/comments from the President in the past. This is one of the reasons we offered that the selloff was simply using the negative headlines as an excuse to do what it desired to do anyway, selloff from lofty levels. But while the reporting from Bloomberg seems candid and inline with the path of headlines toward a phase one trade deal, it also doesn’t lend itself to a trade deal culminating timeline.

If we press the rewind button, one thing we all have come to know is that the President gauges his performance and likability through the lens of equity market performance. We’ve called this the “Trump Put”, and the Trump Put has been in place since the December 2018 market debacle. When things get a little mess in the equity markets, all of a sudden, we see a positive trade headline. I noted this very commonplace routine of market declines met with positive trade headlines in a tweet on Tuesday:

Equity futures are now sharply higher on Wednesday in the 6:00 a.m. EST hour, but I’m not of the opinion the early read on the market will prove lasting. The routine of market declines suddenly met with positive trade headlines, coupled with a looming tariff deadline still may not offset the desire of the market to move lower… but we’ll see what comes to pass as the market also looks forward to economic data.

Probably the biggest economic data point of the day will come from the ADP private sector payroll report. Economists will use the report to model for the potential of the big Nonfarm Payroll report set to be delivered Friday morning. Unless the data points on Wednesday meander far from consensus, we wouldn’t expect the market to have any serious reaction to the data. Positive data is largely priced into the market and be it the labor market or service sector sentiment, both have been the foundation of the bullish economy in 2019.

While the S&P 500 typically falls or rises by 1% or more once a week under normal market churn, there’s not been a 1% day in 7 weeks until… Presently and naturally, the market has weakened and we’ve finally seen 1% daily moves for the S&P 500, although the VIX has moderated back below 16 on Wednesday. A 16-level for the VIX represents a 1%+ intraday move for the S&P 500. The VIX briefly touched 18 during Tuesday’s market decline, and quickly dropped to finish the day just below 16. Finom Group had discussed the headwind for any VIX spike given the total VIX complex positioning, inclusive of long/short VIX-ETP VEGA positioning.

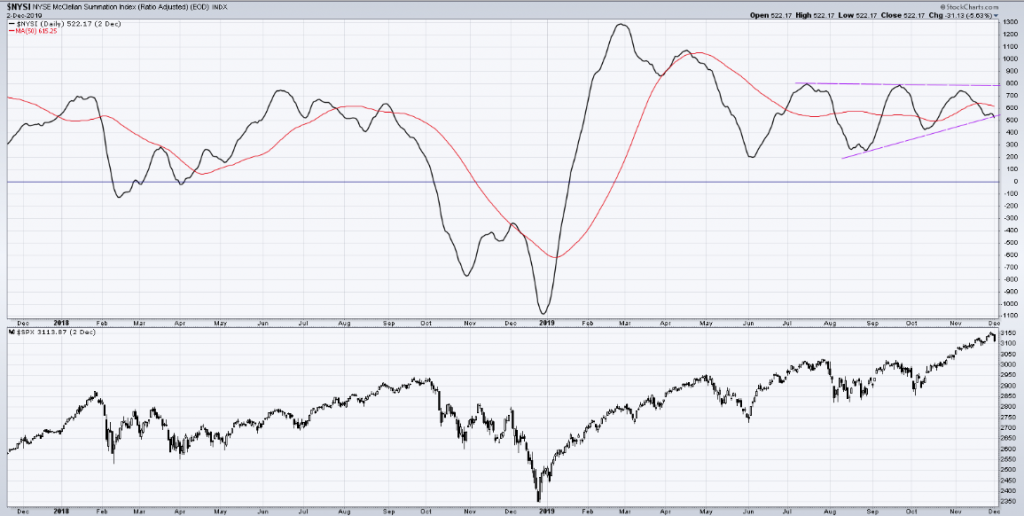

In addition to the rise in market volatility, realized or implied, the McClellan Oscillator moved back into negative territory on Tuesday.

I’m watching the McClellan Summation Index to see if we get a breakdown on this market pullback, which presently looks to rebound Wednesday. Nonetheless, if a breakdown was to occur, that would suggest further market internal weakness near-term.

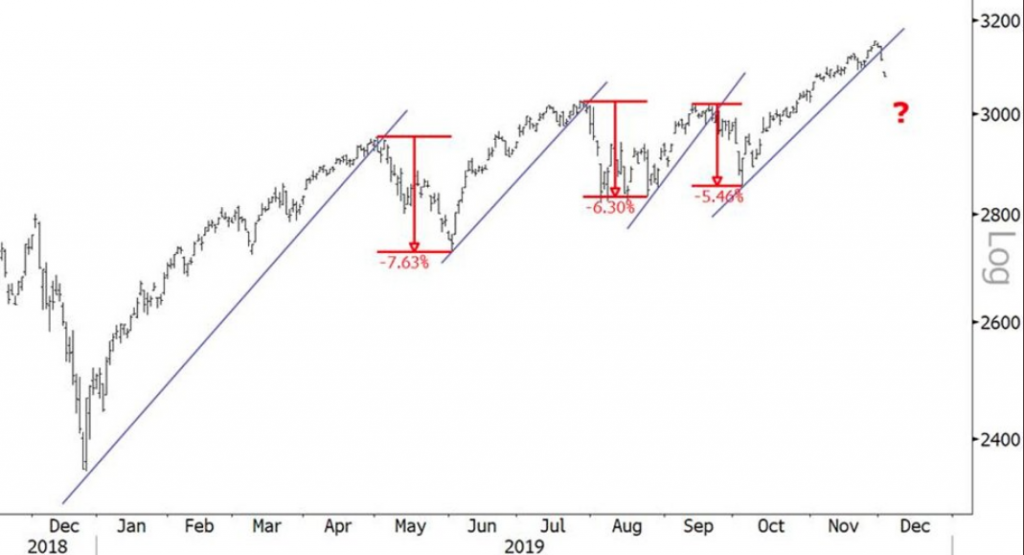

Market pullbacks are normal, natural and healthy. To this point of the calendar year, the market has expressed three intra-year market pullbacks. Carter Worth highlights that the 3 previous trend breaks resulted in selloffs of 7.63%, 6.30%, and 5.46% respectively. If the current break mirrors the previous three, a garden variety 5-8% selloff can be expected.

Given the time of year, which is usually a strong period for stocks, it’s unlikely that a 5-8% period will take place unless the December 15 tariffs or some unforeseen exogenous shock to the market unfolds, in mine and Finom Group’s opinion.

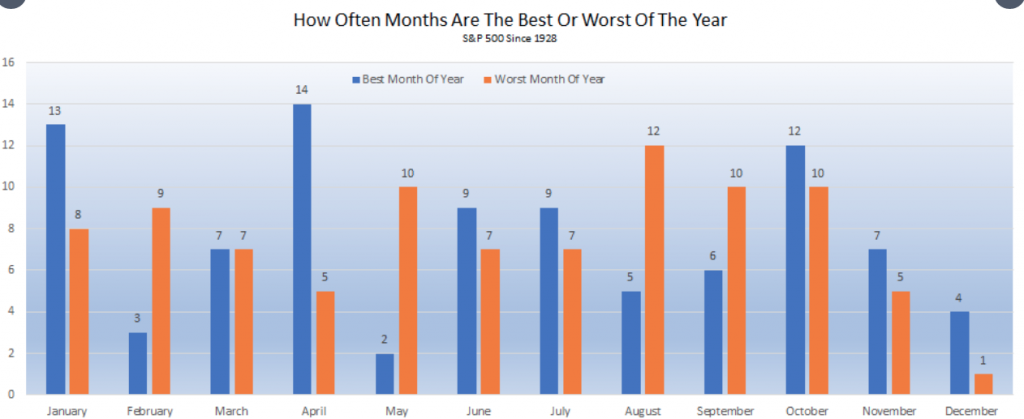

While December is typically a strong month for equities, it certainly hasn’t started off that way… for the last 2 years now. Since 1928, December has been the worst month of the year exactly once, 2018. April has been the best the most often, while August has been the worst the most.

As we look forward to another trading day, and with European markets and U.S. equity futures moving higher, the tone on Wall Street has improved as trade headlines have improved. Funny how that works huh? The December 15th tariffs loom large and as such we would expect a cautious market outlook leading up to the December tariff deadline. To reiterate, we are of the opinion, the calculus for implementing these tariffs is demonstrative on all fronts. As such, we don’t see implementing the December tariffs with advantage for the White House Administration. Consequences would be too steep and based on prudence alone, we wouldn’t be of the opinion the White House Administration goes forward by implementing these tariffs. Nonetheless, we can’t exonerate the possibility, and as such, we suggest investor cautiousness will play a key role in the markets’ direction leading up to December 15th.

Oddly enough, even some of the most standout equity market bears don’t believe the tariffs will be implemented on December 15, although there are likely some that do believe they will roll on.

Looking forward to 2020, analysts have been putting together their S&P 500 price targets under the guise of an improving economic backdrop and trade de-escalation. And while there are a range of views regarding the performance of U.S. equities in the year to come, the top strategists on Wall Street largely agree that 2020’s performance will come nowhere near that of 2019, with only one of those surveyed by MarketWatch predicting the S&P 500 to rise 10% next year from Monday’s close, while a few are predicting year-over-year declines in the large-cap index.

As usual, Morgan Stanley’s chief equity strategist Michael Wilson is the most bearish strategist surveyed, with a base case that the S&P 500 falls to 3,000 by the end of next year.

“Easier monetary policy and trade stabilization will help global growth accelerate, but only stabilize GDP growth in the US at 1.8%, leaving pressure on corporate margins from tight labor markets.

Central bank stimulus may keep stock prices elevated in the near term, “but by April, the liquidity tailwind will fade and the market will focus more on fundamentals, where uncertainty is higher than normal.”

Wilson believes that profit margin headwinds and sluggish U.S. economic growth will keep earnings gains nearly non-existent, as has been the case in 2019, while international trade and policy uncertainty will keep a lid on equity valuations.

And our last mention of the day folks, keep an eye on the price of oil as we edge closer to a key OPEC meeting. OPEC hosts its bi-annual meeting on Thursday in Vienna, Austria. It will be important, interesting and unusual on a number of key levels. Ultimately the only key level that matters to the energy sector and markets is the price of crude.