Welcome to our weekly State of the Markets video where Seth Golden and Wayne Nelson discuss all aspects of the market, from the macro to the micro. Please click the link to review the video. (54 minutes in duration). For expedient reviews, feel free to skip segments of the SOTM by following the Outline below:

- Introduction and brief commentary on what is driving this market and why the market has expressed a near 5% pullback.

- Trade headlines are continuing to cue algos and the market responds positively or negatively depending on the sentiment in the headlines.

- White House Administration has trained market participants to feed into the headlines dating back to the Q4 2018 Fed missteps in messaging and rate hikes that negatively impacted financial conditions and markets.

- Intel (INTC) bought Mobileye in 2017 but nothing has come of the acquisition that is publicly recognizable or of benefit to INTC share price since the acquisition.

- Autonomous driving has been a dream in the making for several years and as various companies have been beta testing and gather data over the last 3-5 years.

- Tesla (TSLA) shares down below $230 as another Model 3 crash was reported today. Autopilot was engaged according to reports.

- Autonomous driving is seemingly a pipe-dream with practical beta testing that seems lost for full deployment into the marketplace.

- A shift to mass autonomous driving application would take a physical and mental, human habitual change. (0-15 minutes in)

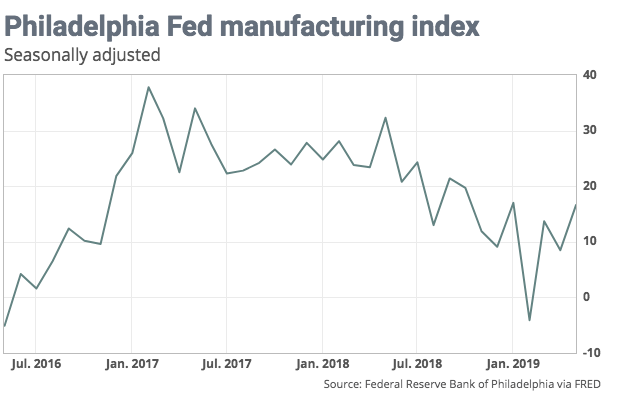

- The Philadelphia Fed manufacturing index in May rose to a four-month high of 16.6 after registering 8.5 in April. The employment index increased 4 points to 18.2, its highest reading in five months. The prices received index declined 3 points to a reading of 17.5, its lowest reading in 17 months.

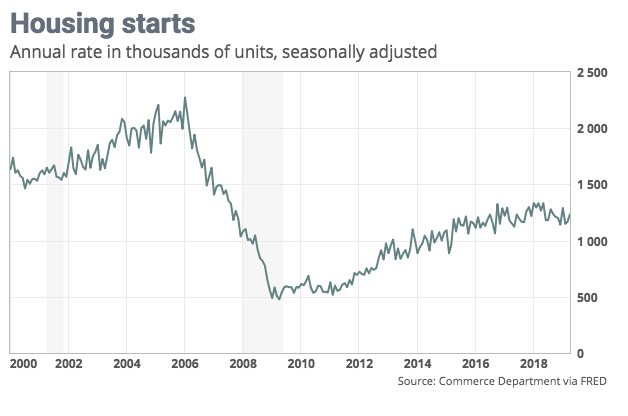

- Housing starts beat expectations and the previous reporting was revised higher as well.

- Jobless claims have fallen for 3 consecutive weeks and back below 215K on Initial Jobless Claims.

- JOLTS survey jumped to over 7.5mm per last week’s report.

- NAHB sentiment index jumped again to 66. Buyer traffic continues to rise. (15-25 minutes)

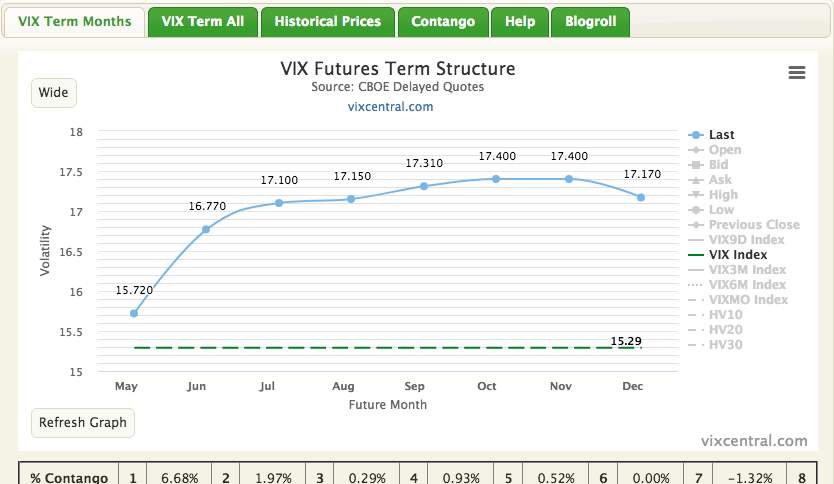

- Market volatility has spike recently alongside the market drawdown.

- Current VOL complex exposure is heavily slanted to long volatility positioning that has been heavily underwater. When VIX has spiked, long positions are being vanquished.

- Discussing Finom Group trade alerts in the VIX-ETPs (TVIX/UVXY/VXX) (25-34 minutes in)

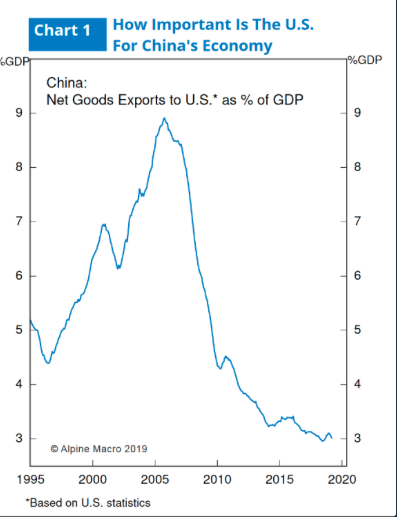

- Debunking charts from various Twitter tweets. Latest is with regard to net exports to U.S. as a % of GDP

- In depth discussion from first-hand experience. That chart could only be made from a fundamental shift in the Chinese economic operation.

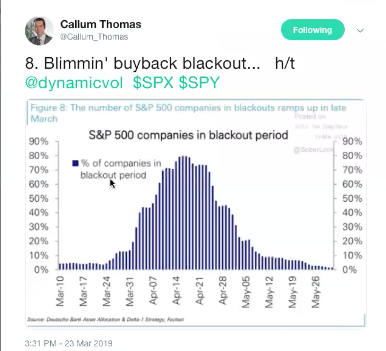

- Formerly issued DB chart of corporate buybacks proposed to peak during mid-April, leaving S&P 500 prone to downturn. S&P 500 only traded higher through this period and Bank of America reported a peak in their buyback operation only 2 weeks ago in early May. (34-51 minutes in)

- Look at intraday market activity.

- Fed’s Brainard discusses inflation in speech today. “In today’s new normal, it is important to achieve inflation and inflation expectations around our 2% target on a sustained basis while guarding against financial imbalances through active use of countercyclical tools. (34-54 minutes in)